Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

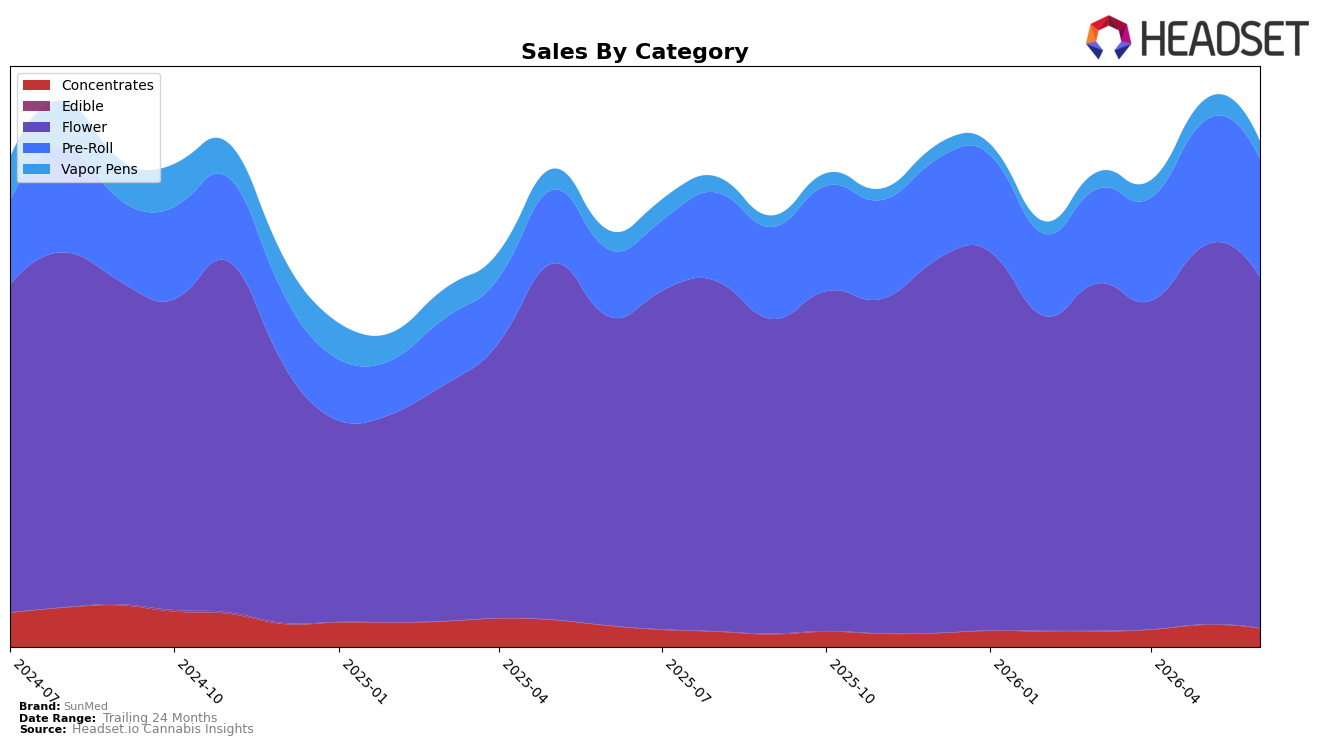

In June 2026, SunMed concentrated 69.43% of sales in Flower with year-over-year growth of 13.42% but a month-over-month decline of 7.43%, while Pre-Roll expanded to 23.41% share with 76.59% YoY growth and a 5.05% MoM dip. Smaller lines contracted simultaneously: Vapor Pens fell 5.23% YoY and 14.77% MoM to 3.53% share, and Concentrates slid 12.98% YoY and 16.12% MoM to 3.60% share. Edible remained a negligible 0.03% share despite 59.50% YoY growth and a 63.59% MoM drop. With overall brand sales up 21.43% YoY and average price down 12.15% YoY, the mix implies price-led unit velocity gains centered on Flower and Pre-Roll, while month-over-month pullbacks across all categories indicate short-term demand softening rather than a structural shift.

Holding the number 1 rank in Flower in Maryland alongside a 13.42% YoY lift and a 7.43% MoM dip positions SunMed as a category anchor that can absorb periodic troughs without ceding share. Pre-Roll’s 76.59% YoY rise and 5.05% MoM decline suggest an elastic, promotion-responsive second pillar that benefits from the 12.15% YoY price decrease brand-wide, whereas Vapor Pens’ 14.77% MoM and Concentrates’ 16.12% MoM drops indicate portfolio pruning or reduced promotional depth. The pattern points to a deliberate tilt toward high-throughput Flower and scalable Pre-Roll to defend rank and grow units, while deprioritizing low-share inhalables limits downside exposure but concentrates risk in two categories that are both showing short-term MoM cooling.

Competitive Landscape

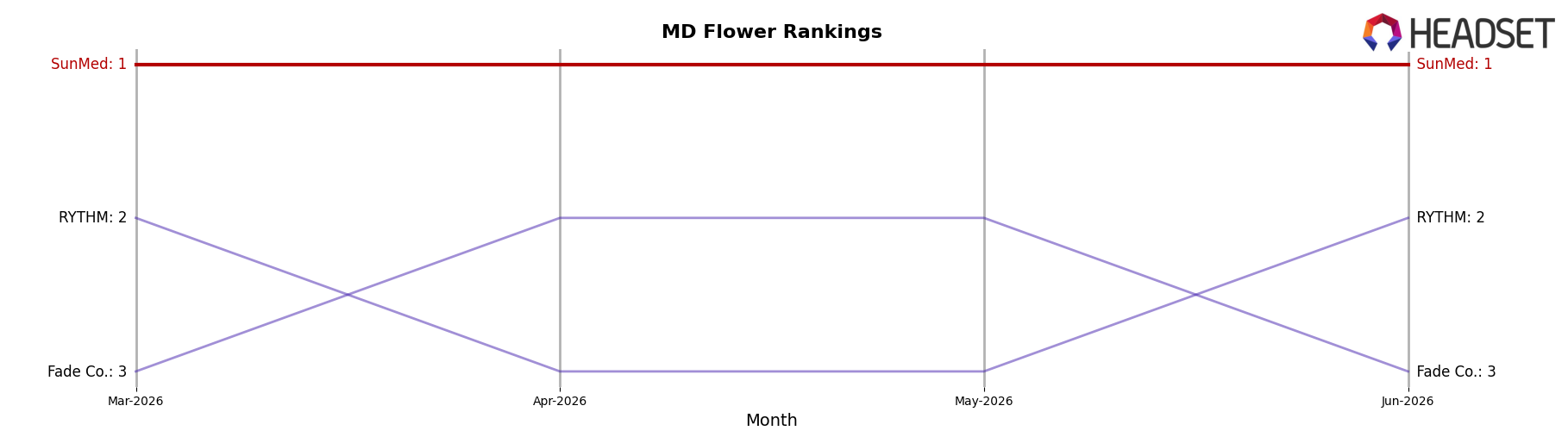

SunMed holds rank #1 in MD Flower in June 2026, unchanged from #1 a year earlier, while its 3-month position also stayed at #1, indicating a flat rank trajectory at the category peak reached in June 2026; in contrast, RYTHM sits at #2 after improving from #3 year over year alongside a 42.7% sales increase, and Strane climbed to #4 from #7 with a 58.8% YoY lift, outpacing Fade Co. which slipped to #3 from #2 despite 23.7% YoY growth; this mix of SunMed’s rank stability and upward pressure from faster-improving competitors implies the top position is defensible in the near term but increasingly contested if double-digit gains persist below it.

Notable Products

The steepest decline came from Sour Diesel (3.5g), which fell -17.2% month over month to rank 3, while Snoop Dogg (3.5g) slipped -9.2% at rank 4, signaling a pivot away from Flower despite their still-elevated positions. In contrast, Sour Diesel Pre-Roll 2-Pack (1g) gained +3.8% MoM to hold rank 1 and SDG OG Pre-Roll 2-Pack (1g) edged +0.4% at rank 2, and six of the top ten are Pre-Roll SKUs, indicating shopper preference is consolidating in ready-to-use formats. With four additional Pre-Roll entries between ranks 5 and 10 and no Pre-Roll declines steeper than -7.8%, the center of gravity is shifting toward multi-pack Pre-Rolls, reducing reliance on Flower volatility. This pattern implies SunMed’s commercial direction is tilting toward Pre-Roll-led velocity, where small MoM gains at the top ranks and broader SKU density can offset double-digit Flower contractions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.