Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

District Cannabis is stocked at 161 licensed dispensaries across Maryland and District of Columbia, 116 of them in Maryland, with the deepest coverage in Baltimore, Silver Spring, Annapolis, Columbia, and Hagerstown. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

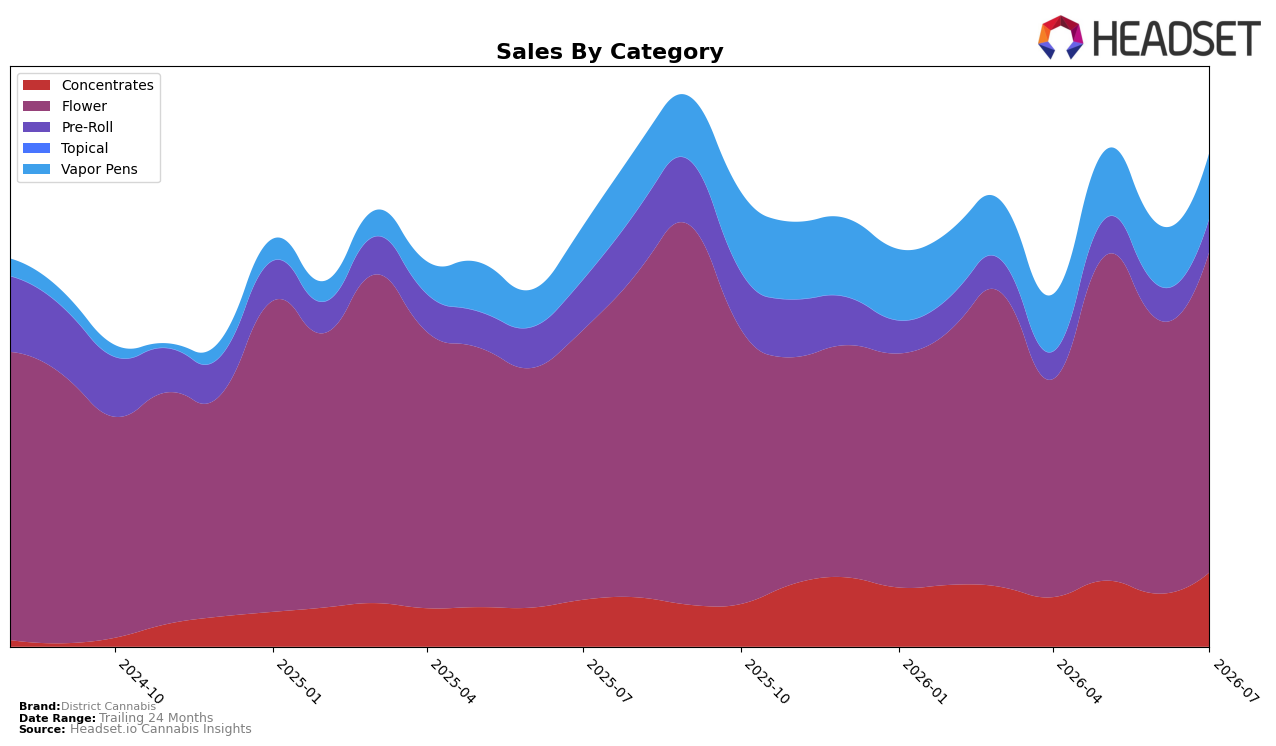

In July 2026, District Cannabis concentrated 65.08% of sales in Flower with year-over-year growth of 19.04% and month-over-month growth of 17.19%, while Vapor Pens held 13.26% share with 23.05% YoY and 7.78% MoM. Concentrates expanded to 15.03% share on 58.70% YoY and 40.36% MoM, whereas Pre-Roll contracted to 6.62% share with -34.67% YoY and -3.41% MoM. With Flower ranked 4 in Maryland and the average price up 16.66% YoY to $33.48, the mix shows a pivot toward higher-value inhalables, implying tighter focus on Flower and Concentrates as volume and price both move up.

The pattern implies District Cannabis is leaning into differentiated potency and premiumization: the 19.04% YoY and 17.19% MoM gains in Flower, combined with Concentrates’ 58.70% YoY and 40.36% MoM, offset the 34.67% YoY decline in Pre-Roll and the 3.41% MoM dip. With Vapor Pens growing 23.05% YoY but only 7.78% MoM, the near-term acceleration is concentrated where margins and price signaling are strongest, supporting a 4th-place Flower position in Maryland and suggesting continued share consolidation around core inhalables rather than breadth across lower-price Pre-Rolls.

Competitive Landscape

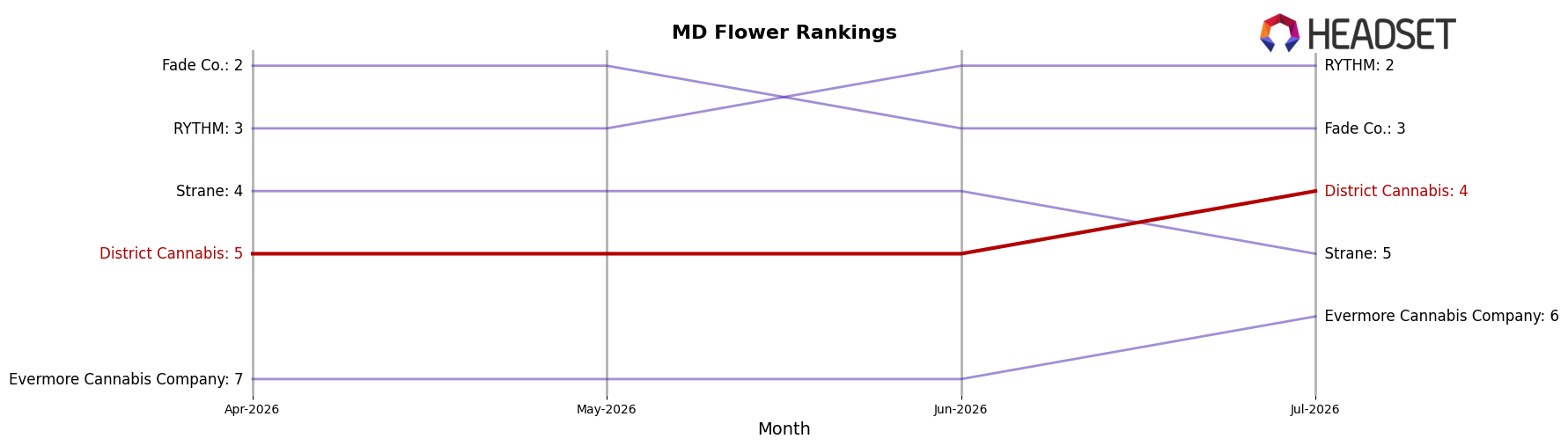

District Cannabis is ranked #4 in MD Flower in July 2026, improving 1 position from #5 year over year while holding flat versus April 2026 at #5 before the recent move; meanwhile, SunMed stayed fixed at #1 year over year as RYTHM advanced from #3 to #2 with a 47.9% YoY sales lift and Fade Co. slipped from #2 to #3 despite 12.7% YoY growth. Compared with Strane, which jumped from #8 to #5 alongside an 82.3% YoY sales increase, District Cannabis’s 1-rank YoY gain and current position below its #2 peak in September 2025 indicate that recent share defense is working but further step-change is needed to reclaim prior peak standing.

Notable Products

Florida Wedding (3.5g) posted the largest movement in July 2026 with a +111% month-over-month surge while climbing into rank 6, whereas Banana Acai Mints (3.5g) fell -37% and slid to rank 5; this divergence indicates shopper pivot toward a refreshed flavor profile over a fading legacy SKU. Pavé (3.5g) advanced +79% to rank 4, and Beach Cake (3.5g) gained +50% at rank 2 while Gelato Cake (3.5g) held rank 1 with +16%, with Flower occupying all top 10 slots to concentrate the portfolio in a single category. The 14g Beach Cake format entered at rank 10 alongside the 3.5g at rank 2, pointing to format laddering that captures both value and premium baskets with only one revenue figure of $258,868 signaling the scale of the 3.5g Beach Cake. The pattern implies District Cannabis is consolidating around Flower with momentum clustered in a few rising strains, suggesting near-term share will depend on sustaining the Florida Wedding and Beach Cake trajectory while pruning underperforming variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.