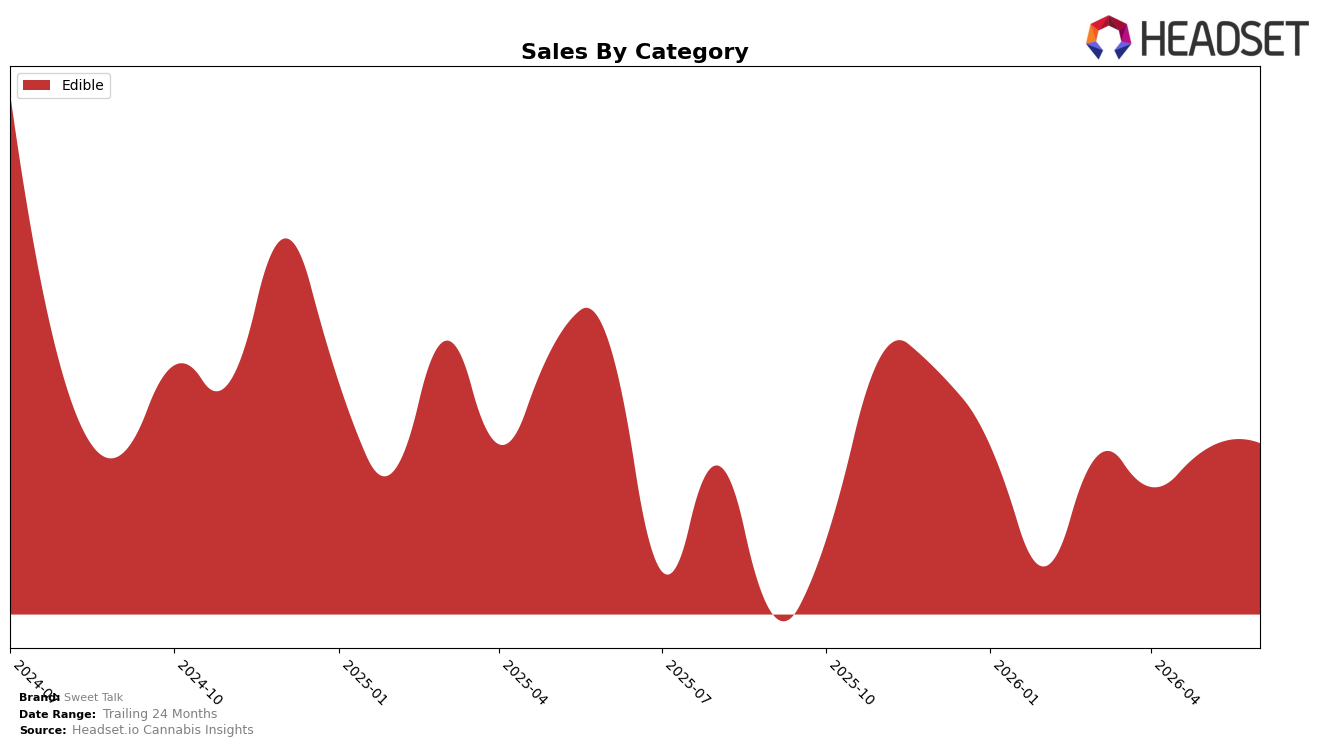

Market Insights Snapshot

Sweet Talk operated as a single-category brand in June 2026, with Edible at 100.0% of mix and a category-level year-over-year decline of 18.3% alongside a month-over-month increase of 1.5%. Average price fell 7.5% year over year while unit velocity expanded enough to produce the 1.5% month-over-month sales gain, and the brand held rank 25 within Edible in Maryland. The pattern implies a price-led volume response that stabilized monthly performance within Edible but left the year-over-year gap intact, suggesting the current single-category concentration limits recovery speed even as short-term momentum improves from a lower price point.

With 100.0% of sales in Edible and a rank of 25 in Maryland, Sweet Talk’s positioning is defined by depth over breadth, trading a 7.5% price reduction for volume that yielded a 1.5% month-over-month lift while still carrying an 18.3% year-over-year decline. This mix and rank setup implies that incremental gains will hinge on pushing up the Edible ladder from position 25 through targeted price-pack architecture rather than cross-category expansion, because the current configuration converts price elasticity into short-term volume without offsetting the wider 18.3% annual drag.

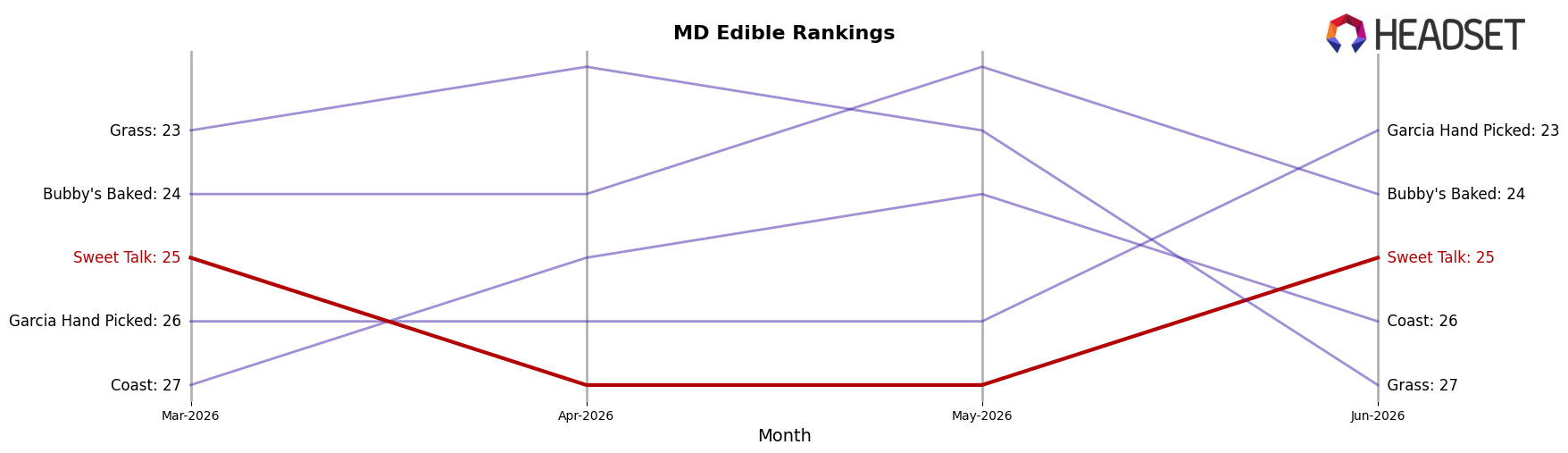

Competitive Landscape

Sweet Talk ranks #25 in MD Edible in June 2026, down 3 places year over year from #22, and flat versus March 2026 at #25; the brand’s peak at #18 in July 2024 is 7 spots higher than today, indicating a continued slide from prior bests. In directional contrast, Incredibles climbed from #3 to #1 with a 49.4% year-over-year sales increase, while Betty's Eddies moved down from #1 to #2 as sales fell 10.8%; concurrently, Jams rose from #9 to #5 on 57.0% growth. The combination of a 3-rank YoY drop and a 7-position gap from the July 2024 peak implies Sweet Talk is ceding relative shelf visibility to faster-rising competitors and needs mix or velocity gains to avoid further rank erosion.

Notable Products

Blue Raspberry Gummies 10-Pack (100mg) posted the largest month-over-month swing in June 2026 with a +78.6% jump to rank 4, while Guava Passionfruit Gummies 10-Pack (100mg) fell -17.9% yet still held rank 1. The top three ranks are concentrated in Edible gummies, with four of the top five also in that format, implying flavor rotation rather than format switching is driving volatility. Sativa Orange Peach Nano Gummies 10-Pack (100mg) rose +9.7% at rank 2 as Guava Passionfruit Gummies 20-Pack (100mg) slid -15.0% at rank 10, pointing to momentum favoring faster-acting or single-flavor 10-packs over larger packs this month. This pattern implies Sweet Talk’s near-term commercial direction will lean into high-velocity 10-pack flavors and nano-positioned SKUs while de-emphasizing larger counts where declines cluster.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.