Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sweetwater Farms is stocked at 109 licensed dispensaries across Washington, with the deepest coverage in Seattle, Spokane, Tacoma, Bellingham, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

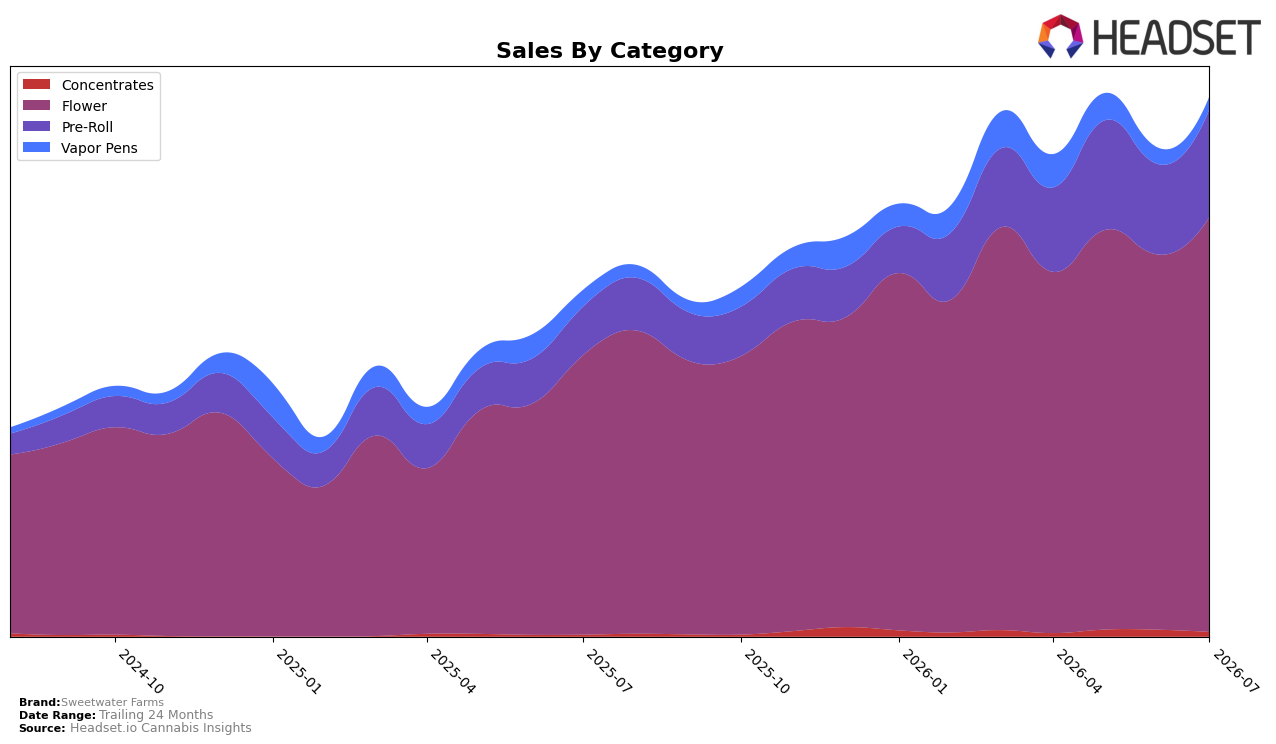

Sweetwater Farms concentrated 76.88% of July 2026 sales in Flower with year-over-year Flower growth of 48.49% and month-over-month growth of 10.61%, while Pre-Roll held 19.92% share with 122.48% YoY and 19.11% MoM growth. In contrast, Vapor Pens slipped to 2.35% share with -23.34% YoY and -21.55% MoM, and Concentrates remained 0.85% share despite 151.14% YoY growth and a -32.58% MoM drop. The mix implies a deliberate tilt toward combustion formats with Flower and Pre-Roll expanding faster than the portfolio average 55.93% YoY brand growth, anchoring scale in Washington while de-emphasizing Vapor Pens near-term.

The category shifts position Sweetwater Farms as a Flower-first brand ranked 5 in Flower in Washington, using Pre-Roll momentum to widen entry points as average price fell 10.60% YoY and Flower average price sat at 24.21. With Vapor Pens declining -21.55% MoM against Pre-Roll’s +19.11% MoM and Flower’s +10.61% MoM, the brand’s demand is consolidating in value-accessible, combustion-led formats; this supports share defense in Flower while keeping Concentrates as an opportunistic niche given 151.14% YoY growth but volatile -32.58% MoM swings.

Competitive Landscape

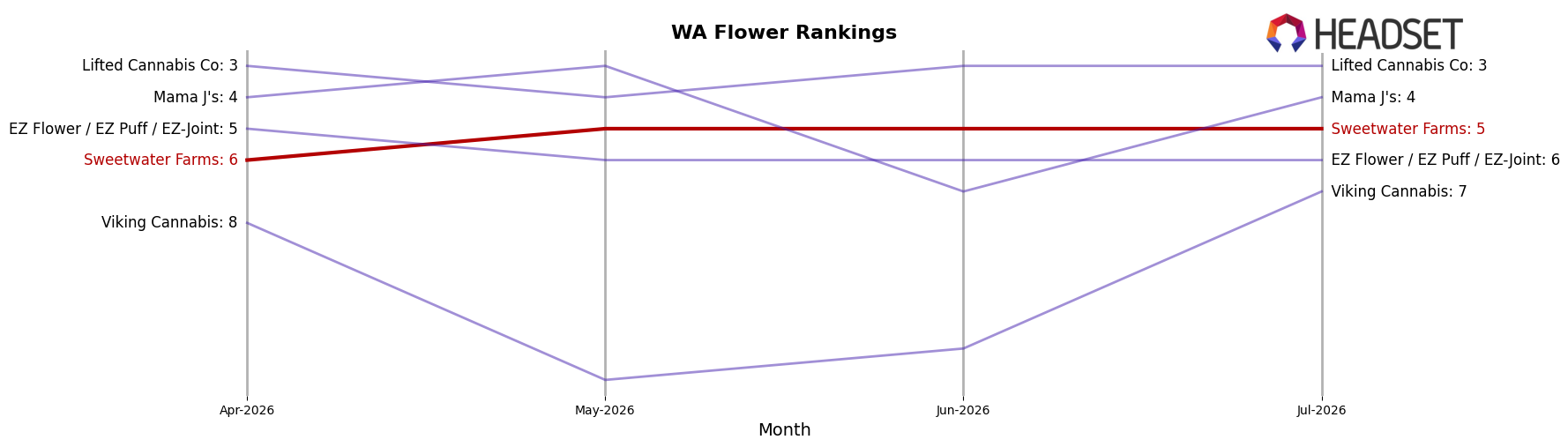

Sweetwater Farms sits at rank #5 in WA Flower in July 2026, improving 9 positions from #14 year over year, and edging up 1 spot from #6 in April 2026 while remaining 1 spot below its peak at #4 in March 2026; meanwhile, Phat Panda holds #1 with an 18.6% YoY sales lift and Legends stays at #2 despite a 22.9% YoY decline, indicating Sweetwater Farms is gaining relative rank against at least one top competitor even as the category leader expands. With Lifted Cannabis Co moving from #8 to #3 on 13.1% YoY sales growth and Mama J's flat at #4 on a 3.9% YoY sales dip, the pattern suggests Sweetwater Farms’ climb from #14 to #5 is driven more by consistent share capture than one-off volatility, implying a trajectory toward stable top-5 tenure if it can convert proximity to its March 2026 peak into sustained rank pressure on #4.

Notable Products

Sweetwater Farms saw no SKU with a month-over-month gain above 50% in July 2026, but Permanent Vacation (3.5g) advanced by 25.7% to rank 4 while Sugar Lemon Scone Pre-Roll 2-Pack (1g) rose 33.2% at rank 6. Permanent Vacation Pre-Roll 2-Pack (1g) held rank 1 with flat MoM data while Blackberry Milkshake Pre-Roll 2-Pack (1g) inched up 3.1% at rank 2, indicating leaders are stable rather than surging. Eight of the top ten are Pre-Roll SKUs, and within that cluster, Juicy GMO Pre-Roll 2-Pack (1g) added 1.9% at rank 3 while the category’s depth kept five ranks inside the top 7. The pattern implies Sweetwater Farms is consolidating around Pre-Rolls for volume while selectively scaling Flower with Permanent Vacation as a growth wedge rather than a full-line push.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.