Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Viking Cannabis is stocked at 140 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellevue, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

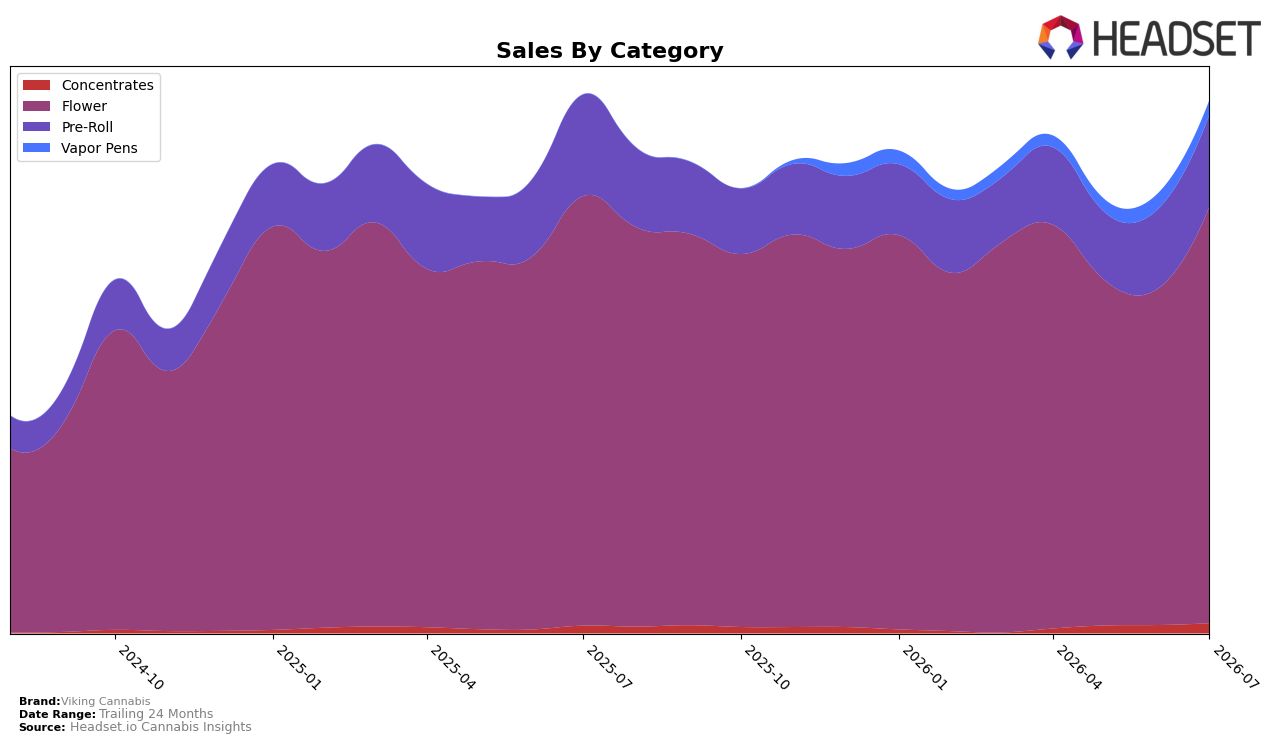

In July 2026, Viking Cannabis concentrated 78.26% of sales in Flower while Pre-Roll held 17.22% and Vapor Pens and Concentrates combined for 4.52%, with Flower up 23.88% month over month but down 2.97% year over year. Pre-Roll rose 15.73% month over month yet fell 9.49% year over year, whereas Concentrates climbed 22.73% month over month and 32.55% year over year as Vapor Pens declined 7.97% month over month with no year-over-year basis. With brand-level sales down 1.07% year over year alongside a 6.32% year-over-year increase in average price and a Flower rank of 7 in Washington, the pattern implies the brand is leaning harder into higher-priced Flower for near-term volume recovery while long-term growth depends on sustaining the outsized momentum in Concentrates despite its 1.86% share and stabilizing the Pre-Roll contraction.

The mix shift—Flower’s month-over-month surge of 23.88% paired with a year-over-year decline of 2.97% and Pre-Roll’s 15.73% month-over-month rise against a 9.49% year-over-year drop—signals a recapture of existing buyers rather than new segment expansion, while Concentrates’ 32.55% year-over-year growth on a 1.86% share points to a small but accelerating foothold that can diversify risk. Given a 7th-place Flower rank in Washington and a brand-wide 6.32% average price lift year over year, the implication is that positioning hinges on defending Flower share with price-led premiumization and reallocating marginal investment toward Concentrates to compound its double-digit growth as Vapor Pens contract 7.97% month over month.

Competitive Landscape

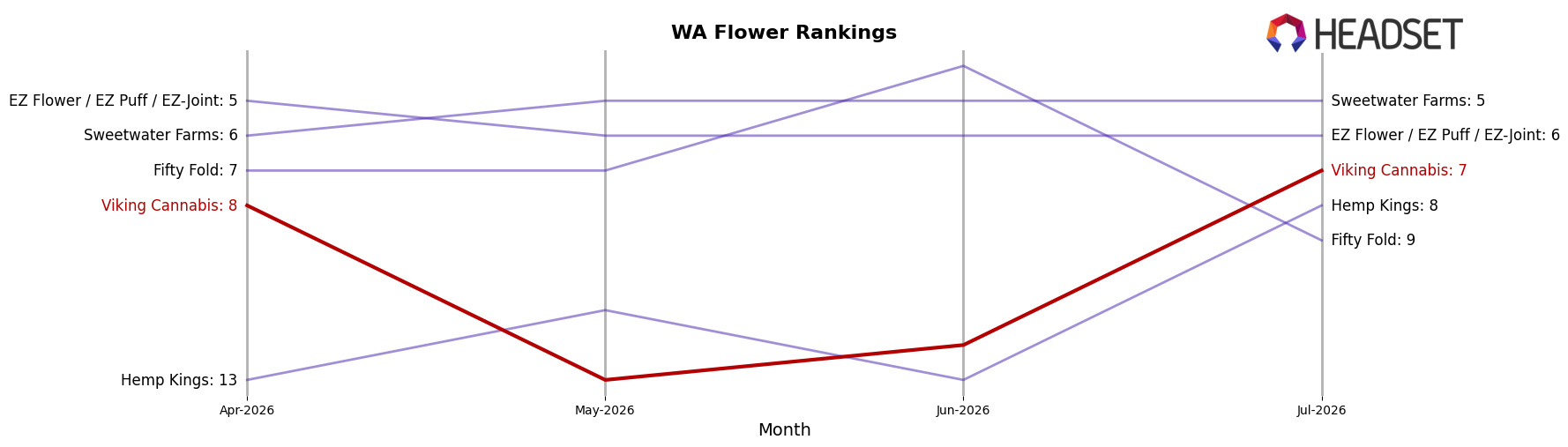

Viking Cannabis sits at rank #7 in WA Flower for July 2026, improving 2 positions from #9 year over year, and edging up 1 spot from #8 in April 2026, while matching its peak rank of #7 also set in July 2026; in contrast, Phat Panda held at #1 year over year with a +18.6% sales change, and Lifted Cannabis Co climbed from #8 to #3 alongside +13.1% sales growth, indicating that Viking Cannabis’s steady rank gains amid competitors’ sharper upward moves suggest a gradual consolidation in the upper tier rather than a breakout into the top five.

Notable Products

Blockberry (3.5g) posted the single biggest move in July 2026 with a 50.0% month-over-month jump into rank 9, while Block Berry Pre-Roll 2-Pack (1g) fell 24.7% to rank 8, indicating volatility between flower and pre-roll formats within the same flavor family. Candy Mac (3.5g) held rank 1 on a 38.6% lift and Oil Tanker (3.5g) stayed at rank 2 with a 24.5% gain, and four of the top ten are Flower SKUs compared to six Pre-Roll SKUs, suggesting breadth but heavier growth momentum in flower. Old School Lemons Pre-Roll 2-Pack (1g) rose 23.6% to rank 4 while the Old School Lemons Infused Pre-Roll 2-Pack (1g) entered at rank 3 with $8,079, showing infused formats can secure high placement even as traditional pre-rolls vary. The pattern implies Viking Cannabis is tilting product energy toward higher-velocity flower strains while selectively using infused pre-rolls to anchor premium visibility, creating a two-tier mix that prioritizes scalable flower gains over more variable pre-roll demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.