Where to Buy

Swisher is stocked at 343 licensed dispensaries across Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Grand Rapids, and Flint. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

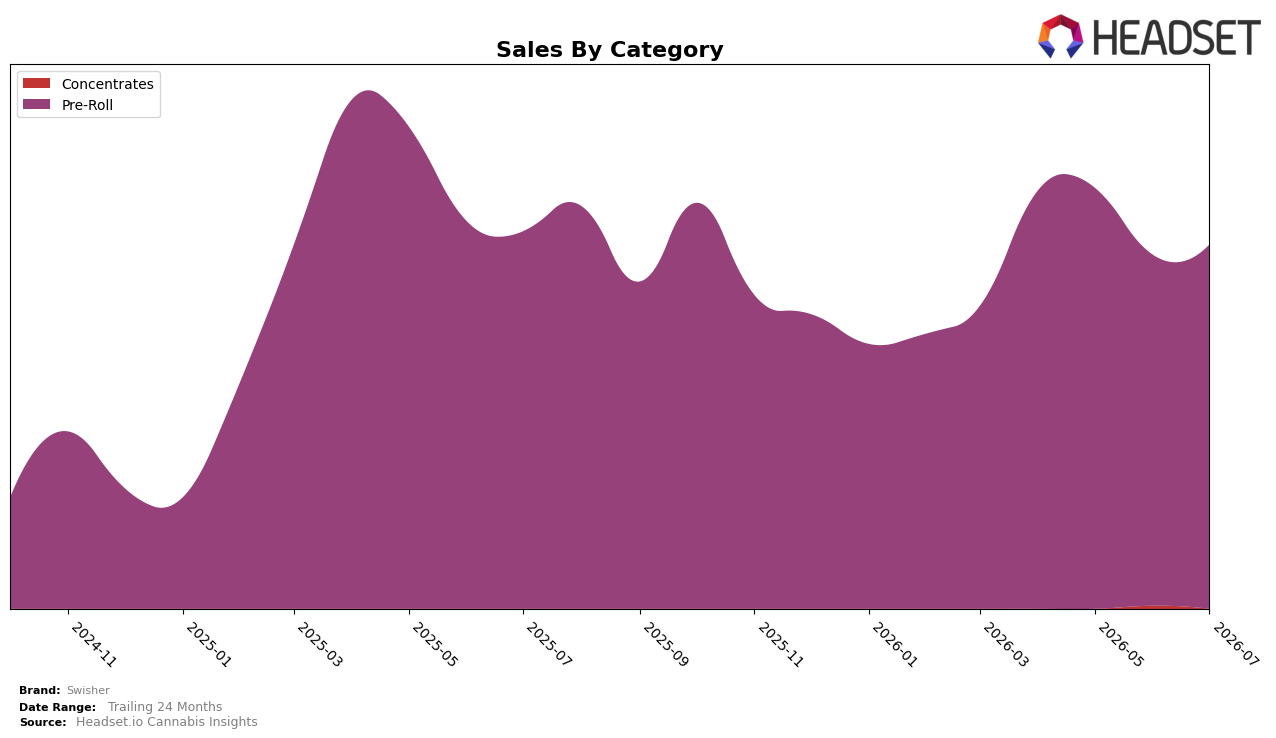

Market Insights Snapshot

In July 2026, Swisher’s category mix remained fully concentrated in Pre-Roll at 100.0% share, with Pre-Roll sales up 3.84% month over month but down 3.54% year over year. Average price declined 22.34% year over year to $17.75, while the brand’s rank in Michigan Pre-Roll sat at 19. These combined shifts imply volume is carrying the month-over-month lift despite price compression, while the year-over-year dip and a rank position of 19 indicate limited headroom without mix diversification.

The coexistence of a 3.84% month-over-month sales gain and a 22.34% year-over-year price drop suggests Swisher is relying on lower-price positioning to drive units, yet a 3.54% year-over-year sales decline and rank 19 in Michigan Pre-Roll point to constrained differentiation within a single-category portfolio. This pattern implies that without expanding beyond a 100.0% Pre-Roll mix or trading up within the Pre-Roll tiering ladder, the brand’s price-led volume strategy risks capping share gains and keeping rank pressure in place.

Competitive Landscape

Swisher sits at rank #19 in MI Pre-Roll in July 2026, down 4 spots year over year from #15 and slipping 5 positions from #14 three months ago, while its historical peak was rank #10 in May 2025; in contrast, Mitten Extracts climbed from #7 to #4 and Jeeter held flat at #1 year over year with a 4.0% sales gain, whereas Cali-Blaze stayed at #2 despite a 38.5% sales decline. The directional gap widens as Swisher’s 12-month rank delta is -4 while peer moves include a +3 shift for Mitten Extracts and a -1 drift for Goodlyfe Farms from #4 to #5, implying that Swisher’s downward trajectory is less about broad market compression and more about losing relative position to brands that are either holding or advancing within the top 5.

Notable Products

Peach Mango Infused Blunt 5-Pack (2.5g) posted the steepest shift in July 2026 with a -28.4% month-over-month change and slid to rank 7, while Strawberry Kiss Infused Blunt (1.5g) surged +54.2% to rank 4, implying consumer momentum is rotating from some multi-pack flavors toward single-stick novelty. Classic Grape Infused Blunt 5-Pack (2.5g) climbed +37.8% MoM and sits at rank 2 alongside a parallel +33.0% for Classic Grape Infused Blunt (1.5g) at rank 3, indicating cross-size strength within the same flavor family. Five-packs still anchor the leaderboard with multiple top-10 placements, yet Watermelon Infused Blunt 5-Pack (2.5g) at rank 1 grew only +3.6% MoM against faster-rising singles, and the category’s July 2026 mix features at least seven Pre-Roll SKUs in the top ten, concentrating demand in flavor-forward formats. The pattern implies Swisher is shifting toward flavor families where both single and multi-pack formats can be activated, but near-term mix will favor high-velocity singles to recover share lost by underperforming multi-pack variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.