Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Play Cannabis is stocked at 220 licensed dispensaries across Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Grand Rapids, and Ann Arbor. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

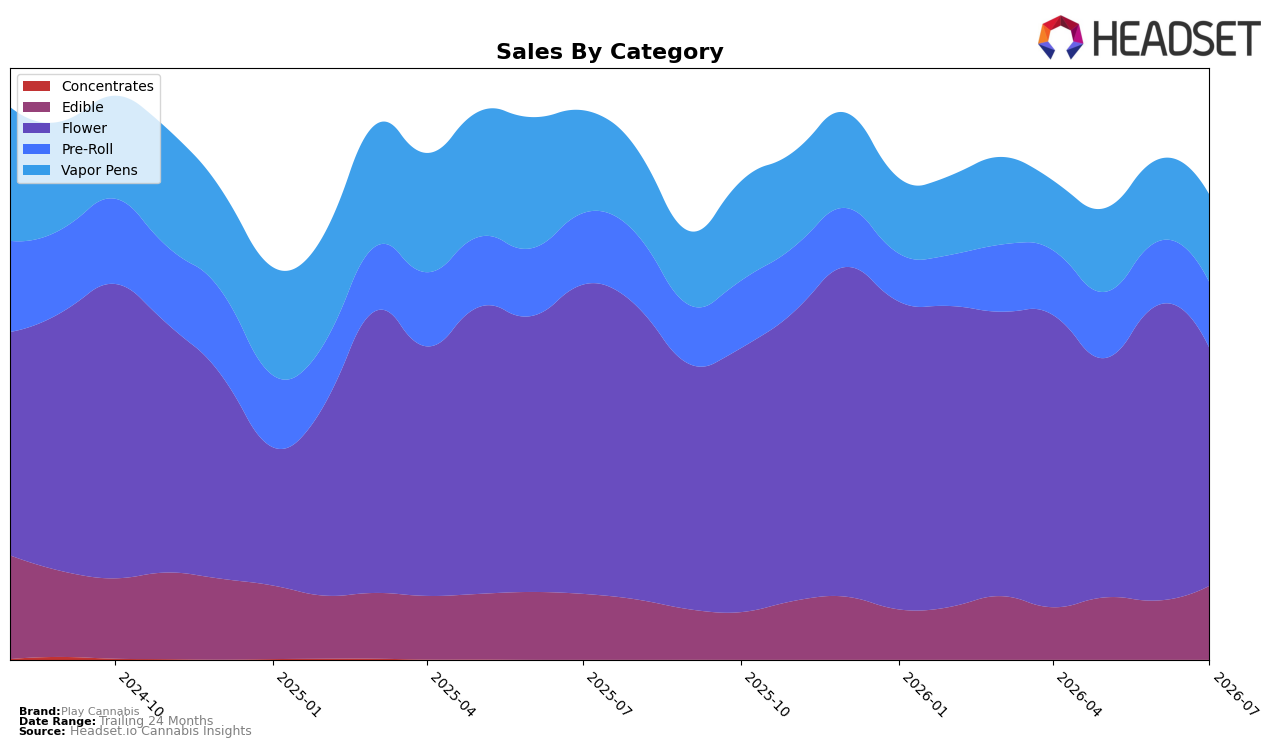

Play Cannabis concentrated 51.19% of July 2026 sales in Flower, where year-over-year declined 23.16% and month-over-month slipped 19.53%, while Vapor Pens held 18.83% share with a 14.77% YoY decline but a 6.95% MoM uptick. Edible expanded to 15.89% share with 12.29% YoY growth and 24.88% MoM growth, and Pre-Roll represented 14.09% share with an 8.17% YoY decline but a 3.11% MoM increase. With brand-wide sales down 15.40% YoY and average price down 17.35% YoY, the mix now leans away from the contracting Flower core and toward faster-moving Edible and stabilizing Vapor Pens, implying July 2026 was a pivot month in which category balance began to mitigate the Flower drag.

Holding rank 7 in Flower in Michigan while Flower’s MoM fell 19.53% signals erosion in the core that limits share capture, but double-digit MoM growth in Edible at 24.88% and a 6.95% MoM rise in Vapor Pens suggest near-term gains accrue where price points are lowest. Given the 15.40% YoY brand decline alongside a 12.29% YoY lift in Edible, the sustainable path is reallocating assortment and merchandising toward Edible and Vapor Pens while defending Flower rank 7, implying positioning should shift from a Flower-led identity to a multi-format value footprint that trades lower average prices for higher velocity.

Competitive Landscape

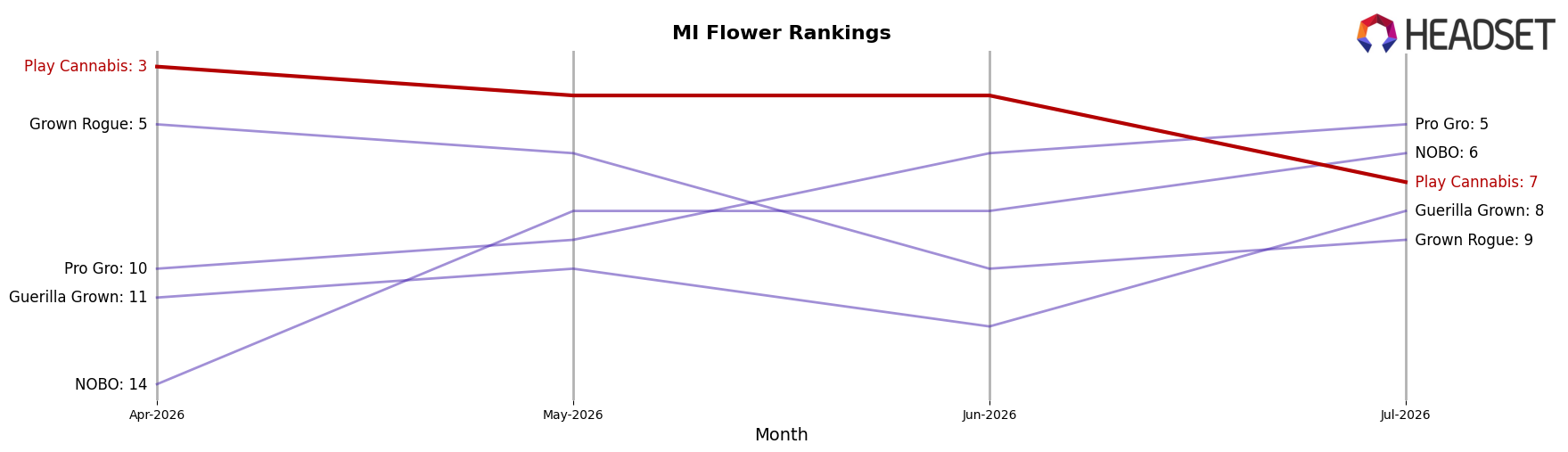

Play Cannabis sits at rank #7 in MI Flower in July 2026, down 3 places year over year from #4 and down 4 spots from its three-month position of #3, even though it previously peaked at #2 in February 2026; meanwhile, High Minded held #1 despite a -12.5% YoY sales change and Goodlyfe Farms advanced from #5 to #3 with +36.8% YoY sales, indicating Play Cannabis is ceding rank to competitors gaining momentum despite mixed category contractions at the top.

Notable Products

Berry Burst Gummies 4-Pack (200mg) posted the largest month-over-month gain, up 45.0% to rank 2 in July 2026, while Pink Lemonade Gummies 4-Pack (200mg) rose 33.9% to hold rank 1. Peach Gummies 4-Pack (200mg) climbed 42.3% at rank 5, but Watermelon Gummies 4-Pack (200mg) in rank 6 inched up only 1.5%, creating a widening spread between fast movers and stable SKUs. Eight of the top ten are Edible gummies, and three Live/Hash Rosin variants sit within ranks 3, 4, and 7, concentrating mix in solventless cues even as core fruit flavors dominate unit velocity. The pattern implies Play Cannabis is consolidating leadership in gummies with a two-track strategy: flavor-led volume at ranks 1–2 and premium rosin line extensions that deepen price laddering without diluting rank concentration.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.