Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

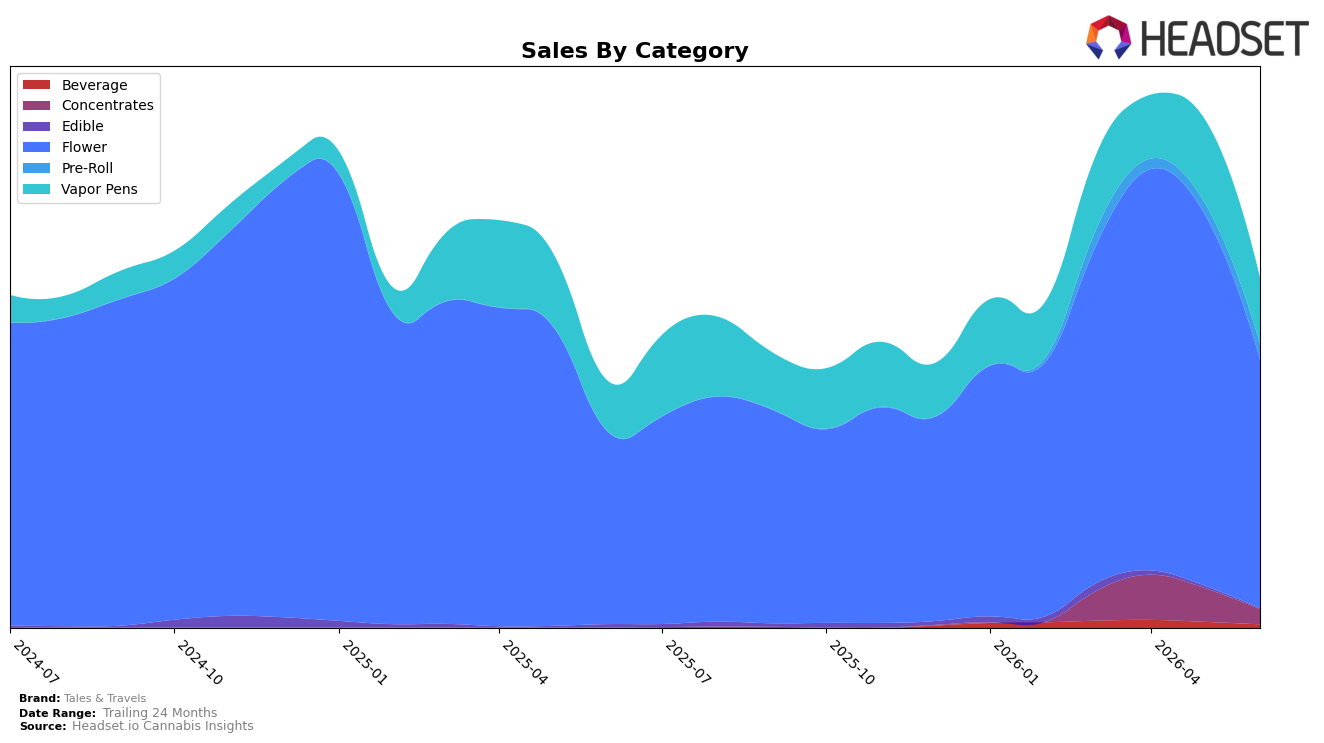

In June 2026, Tales & Travels concentrated 71.24% of sales in Flower with a 29.60% year-over-year lift but a 33.08% month-over-month drop, while Vapor Pens held 18.84% share with 31.04% YoY growth and a 21.11% MoM decline; Pre-Roll rose 39.00% MoM to 4.45% share as Concentrates fell 55.59% MoM to 4.25% share. Edible contracted 81.94% YoY and 72.43% MoM to just 0.16% share, and Beverage declined 40.13% MoM to 1.07% share, coinciding with a 13.00% YoY decrease in average price to $37.06. The pattern indicates a reliance on high-velocity inhalables that expanded YoY but retrenched MoM, with Pre-Roll absorbing some downshift from Flower while price reductions likely supported unit throughput at the expense of mix breadth.

With Flower ranked 18th in Illinois and comprising 71.24% of volume against a 21.11% MoM pullback in Vapor Pens, the portfolio tilts toward value-sensitive inhalables where short-cycle promotions can swing share. The 39.00% MoM gain in Pre-Roll alongside a 33.08% MoM decline in Flower implies trade-down within inhalables, while a 55.59% MoM fall in Concentrates and a 40.13% MoM fall in Beverage signal limited traction in premium or niche formats; this positions Tales & Travels to capture price-flexible demand but constrains defense against format shifts unless Flower volatility is buffered by sustained Pre-Roll expansion and stabilized pen pricing.

Competitive Landscape

Tales & Travels sits at rank #18 in IL Flower in June 2026, up 7 positions from #25 year over year but down 6 spots from #12 three months ago; the brand also pulled back from its April 2026 peak of #11, indicating a mid-year cooling after early gains. In contrast, High Supply / Supply held at #1 year over year with sales up 32.1%, while RYTHM stayed at #2 despite a 5.2% YoY sales decline, and Good Green climbed from #4 to #3 with a 30.9% sales increase; this mix of top-end stability and selective upward mobility implies that Tales & Travels’ rank trajectory—improving YoY yet slipping from a recent #11 peak—signals share pressure from faster-rising incumbents and the need to convert early-year momentum into sustained placement.

Notable Products

Banana Mango Distillate Disposable (1g) posted the steepest movement in June 2026 with a -27.2% month-over-month drop and fell to rank 9, while Pink Lemonade Distillate Disposable (1g) also declined -22.2% at a shared rank 7, signaling demand compression in disposables despite Strawberry Guava Distillate Disposable (1g) inching up +3.1% at rank 6. Flower concentrated the top ten with five SKUs, including Fruit Stand (3.5g) up +13.3% at rank 2 and Georgia Pie (3.5g) down -2.3% at rank 4, indicating steadier velocity in Flower versus volatility in Vapor Pens. Peach Crescendo Pre-Roll (1g) held rank 1 with $7,114 in sales and no reported month-over-month rate, contrasting with Vapor Pens where two SKUs declined more than 20% and one improved slightly. The mix implies Tales & Travels is leaning into Flower and a hero Pre-Roll for stability while discretionary Vapor Pen flavor rotations require pruning or price recalibration to reduce variance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.