Where to Buy

The Lid is stocked at 34 licensed dispensaries across New Jersey, with the deepest coverage in Franklin Township, Jersey City, Andover, Atlantic City, and Bloomfield. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

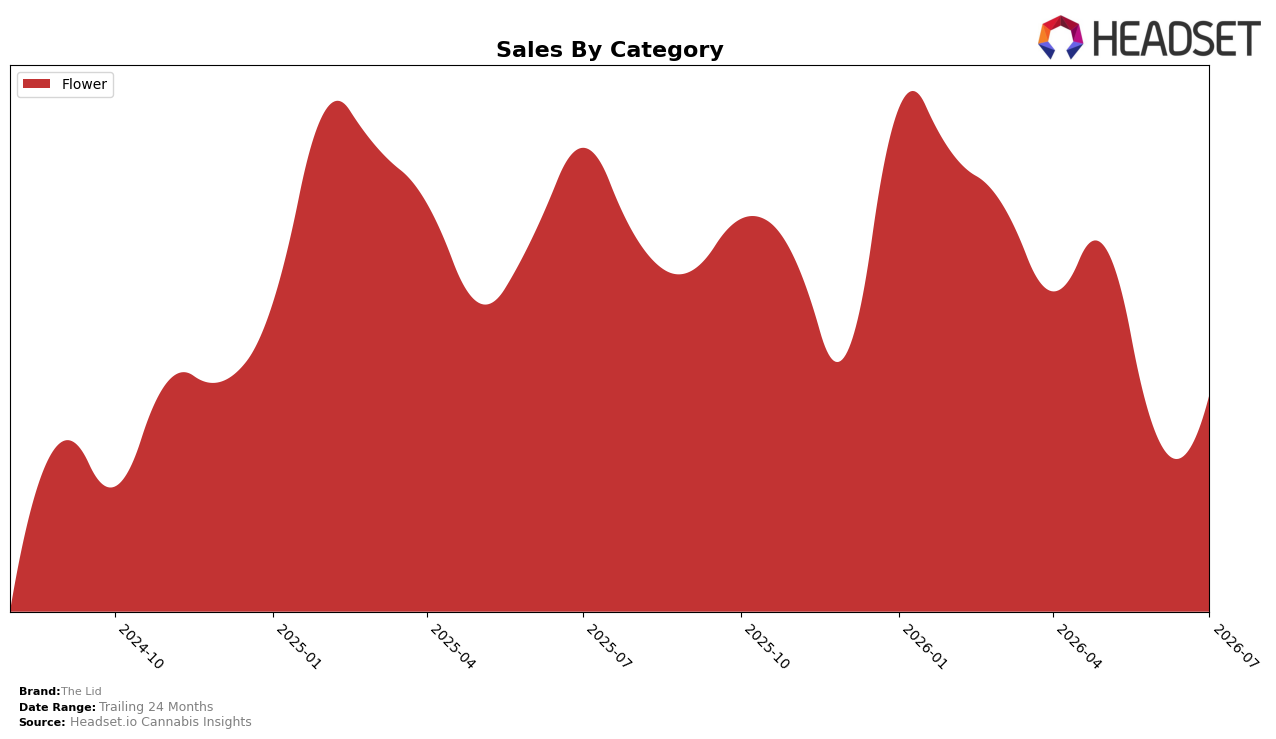

In July 2026, The Lid operated as a single-category brand with Flower at 100.0% of sales, posting a year-over-year decline of 38.9% alongside a month-over-month increase of 12.8%, while average price slipped 1.0% YoY. Within Flower, the brand held rank 23 in New Jersey, and the all-brand 24-month sales trend declined 18.9%, indicating that the recent monthly uptick did not offset the longer downward pull. The pattern implies a narrow product scope that amplifies category volatility: a one-category, rank-23 position in a single state leaves The Lid exposed to YoY contractions even when MoM demand rebounds.

The consolidation in Flower—100.0% mix with a 12.8% MoM gain but a 38.9% YoY drop—suggests The Lid is relying on short-cycle promotional or seasonal lift rather than sustained share capture at rank 23 in New Jersey. With average price down 1.0% YoY against a 24-month sales decline of 18.9%, the price move has not translated to durable growth, implying that mix breadth or tiering, not further discounting, is the likely lever for stabilizing position.

Competitive Landscape

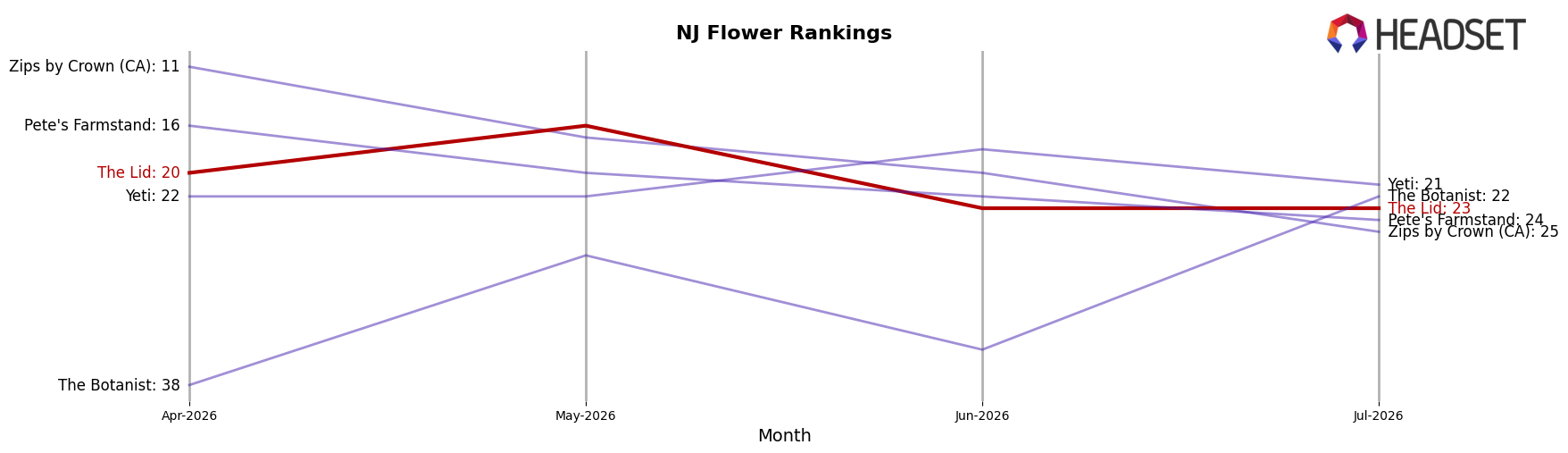

The Lid sits at rank #23 in NJ Flower for July 2026, down 12 positions year over year from #11, and 3 spots lower than April 2026 when it was #20; the brand’s peak rank of #9 in January 2026 underscores a slide of 14 places from that high, while competitor movements contextualize the pressure as Ozone holds #1 after a year-over-year move from #2 and a -13.1% sales change, and Find. climbed from #10 to #2 with +129.0% sales growth. Meanwhile, Simply Herb advanced from #6 to #3 and Good Green rose from #9 to #4, placing The Lid’s 3-rank drop since April 2026 alongside rivals’ upward rank shifts of 3–8 places; this pattern implies The Lid is losing relative velocity in shelf position and consumer pull as faster-rising peers compress its share of top-tier slots.

Notable Products

Cherry Hill Pre-Ground (14g) posted the steepest movement in July 2026 with a -51.6% month-over-month decline while sitting at rank 9, contrasting with Butler Biscotti Pre Ground (14g) which rose +11.3% MoM at rank 3. The top two positions were held by Waretown Watermelon Pre Ground (14g) at rank 1 and Pennington Papaya Pre Ground (28g) at rank 2, and eight of the top ten were Flower pre-ground or shake formats, indicating a concentration in value-oriented Flower. With Trenton Trop Pre Ground (14g) slipping -6.5% MoM at rank 5 and total Flower dominance across ranks 1 through 10, the mix implies The Lid is consolidating around bulk and pre-ground Flower while deprioritizing slower-moving SKUs like Cherry Hill Pre-Ground (14g).

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.