Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

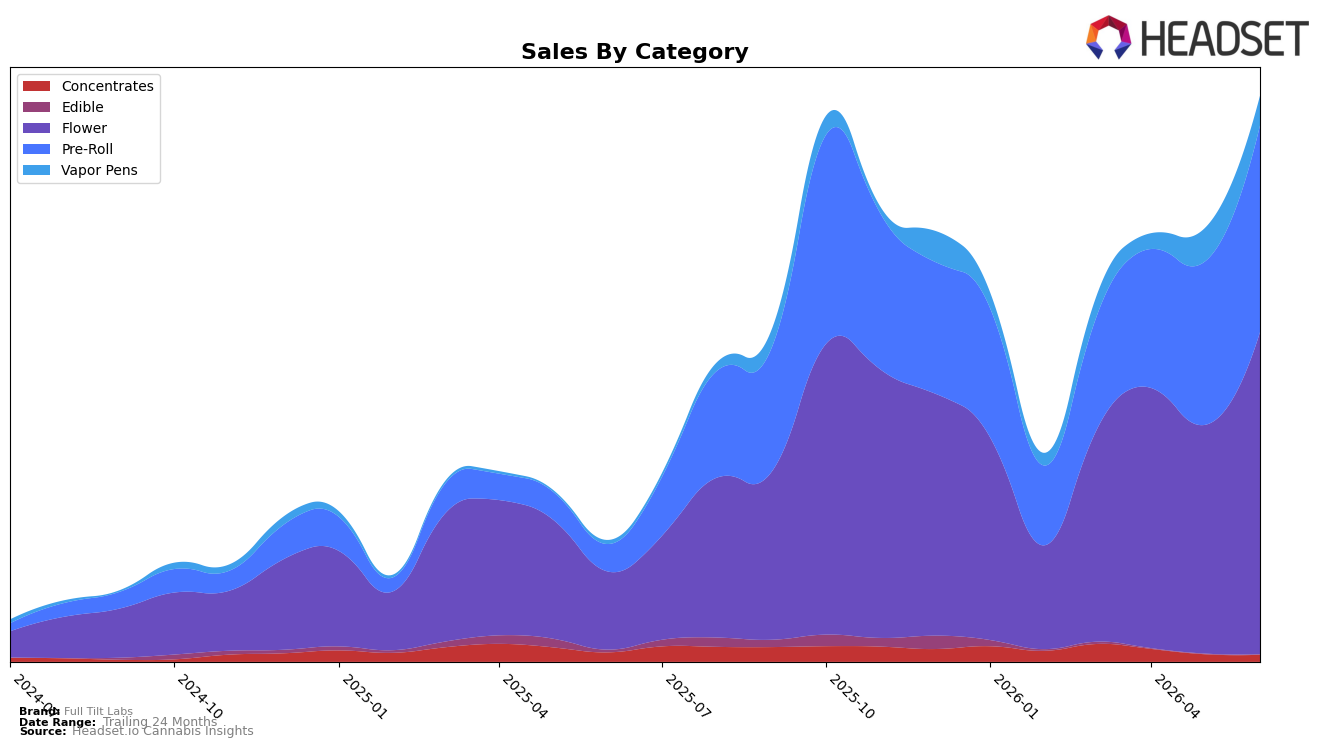

In June 2026, Full Tilt Labs concentrated 56.97% share in Flower with 314.13% YoY and 40.89% MoM growth, while Pre-Roll held 36.55% share with 656.65% YoY and 26.67% MoM, signaling that two inhalable formats now account for 93.52% of mix; Vapor Pens slipped to 5.22% share with 680.96% YoY but an -11.14% MoM decline, and Concentrates and Edible combined for 1.26% share with -25.69% YoY and -31.37% MoM in Edible. Average price rose 0.78% YoY to $39.84 as Flower’s higher average price of 62.17 and Concentrates at 72.10 outweighed Edible’s low 14.64 and Pre-Roll’s 25.72; together with a category rank of 13 in Flower in New Jersey, the pattern implies a sales engine driven by premium-leaning Flower and scale-oriented Pre-Roll while near-term softness in Vapor Pens caps basket expansion.

The tilt toward Flower and Pre-Roll—up 40.89% and 26.67% MoM respectively—paired with Vapor Pens’ -11.14% MoM signals assortment prioritization toward fast-turn inhalables at the expense of breadth in Concentrates (-6.87% MoM) and Edible (-31.37% MoM); this mix, combined with 314.13% YoY in Flower versus 656.65% YoY in Pre-Roll, implies positioning that leverages Pre-Roll for trial and traffic while anchoring value perception in higher-priced Flower. Holding the 13 rank in New Jersey Flower alongside a 56.97% mix share there and a 0.78% brand-wide price lift suggests the path to rank gains runs through maintaining Flower price integrity while moderating Pre-Roll discount depth to convert Pre-Roll-driven acquisition into upsell without reinflating Vapor Pens’ churn.

Competitive Landscape

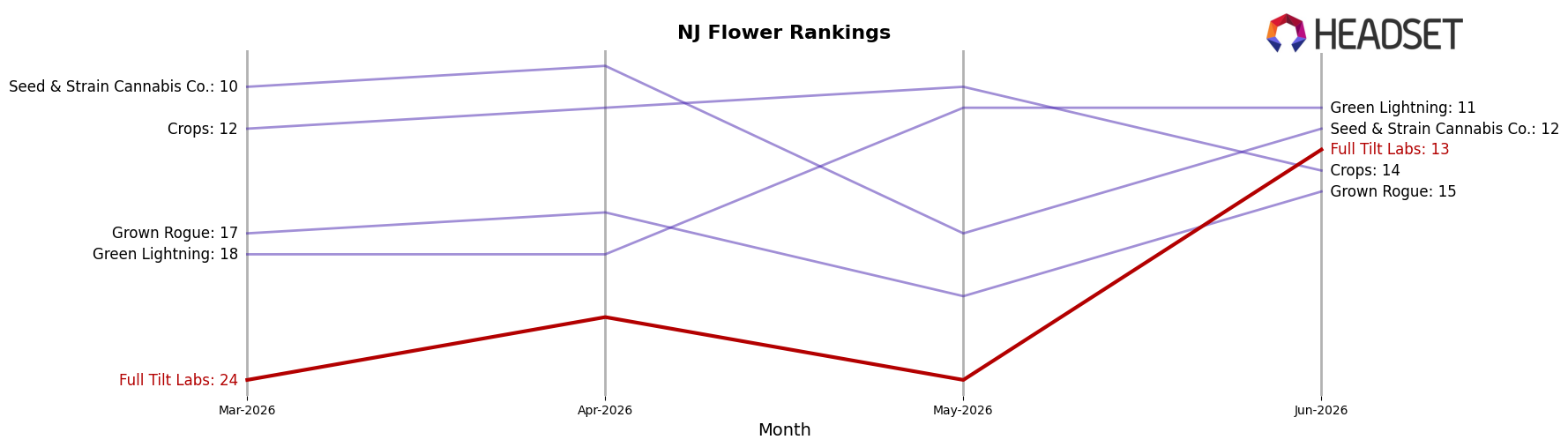

Full Tilt Labs is ranked #13 in New Jersey Flower in June 2026, up 23 positions from #36 year over year, and 11 positions from #24 in March 2026; this marks a new peak rank at #13 in June 2026 while also compressing the gap to the top 10. Competitive context is shifting: Find. climbed from #12 to #1 with a 225.99% year-over-year sales increase, while Ozone held near the top moving from #2 to #2 as sales contracted 10.61%, indicating that share is rotating toward faster risers; against that backdrop, Full Tilt Labs’ jump of 23 ranks year over year and 11 ranks over three months implies a momentum-driven entry into the tier just below the leaders, setting expectation for near-term top-10 contention if the trajectory persists.

Notable Products

Crippy Dog (3.5g) led the downside with a -22.7% month-over-month change while sliding to rank 7, whereas ZUBAI (3.5g) delivered a +57.6% MoM surge to rank 2, narrowly behind Fruity Pebbles Distillate Cartridge (1g) at rank 1 with +28.5% MoM. Pre-Roll SKUs account for six of the top ten, but the most dynamic movement is concentrated in Flower where one SKU gained over +50% and another fell over -20%, implying deliberate SKU pruning alongside targeted push for a single breakout flower.

ZUBAI (3.5g) generated $59,183 in June 2026 while Fruity Pebbles Distillate Cartridge (1g) held the top spot with a smaller +28.5% MoM rise, indicating mix shift toward higher-velocity Flower even as Vapor Pens retain the #1 rank. With four Pre-Roll placements in ranks 3–6 and two more in ranks 8–10, the breadth sits in multi-pack Pre-Rolls, but the growth signal rests in a two-gear portfolio of one accelerating Flower and one stabilizing pen, suggesting emphasis on a hero Flower SKU supported by a steady flagship cartridge.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.