Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

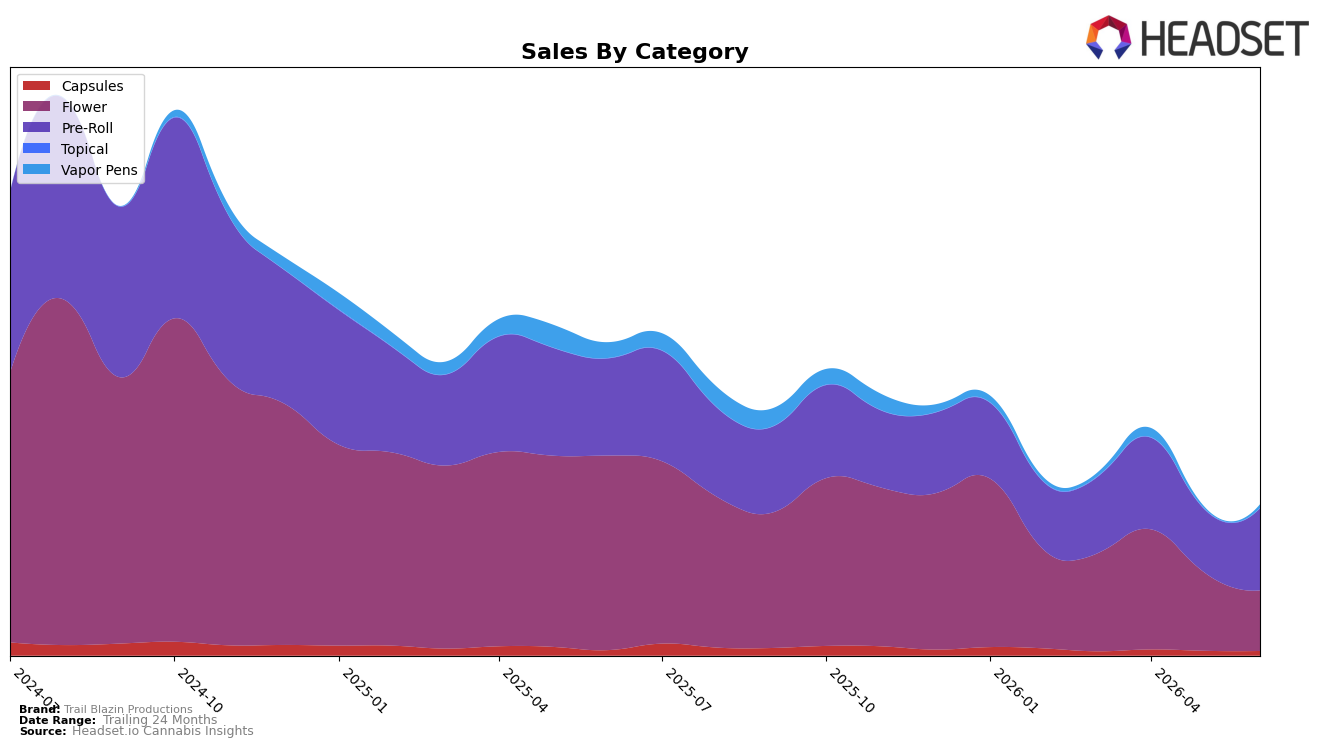

Trail Blazin Productions shifted decisively toward Pre-Roll in June 2026, with Pre-Roll capturing 54.57% share on 30.09% month-over-month growth even as its year-over-year sales were down 15.60%, while Flower slid to 40.21% share with a 22.60% month-over-month decline and a 68.99% year-over-year drop. Smaller lines moved in opposite directions: Vapor Pens doubled month-over-month by 100.72% but remained only 2.26% of mix after a 78.12% year-over-year fall, and Capsules held 2.97% share with a 3.58% month-over-month decline and a 16.35% year-over-year contraction. With brand-wide sales down 51.98% year-over-year and average price down 9.57% to $16.75, the pattern implies mix is consolidating into a lower-priced Pre-Roll center while premium-priced Flower retrenches, compressing overall revenue despite tactical month-over-month gains in value-led formats.

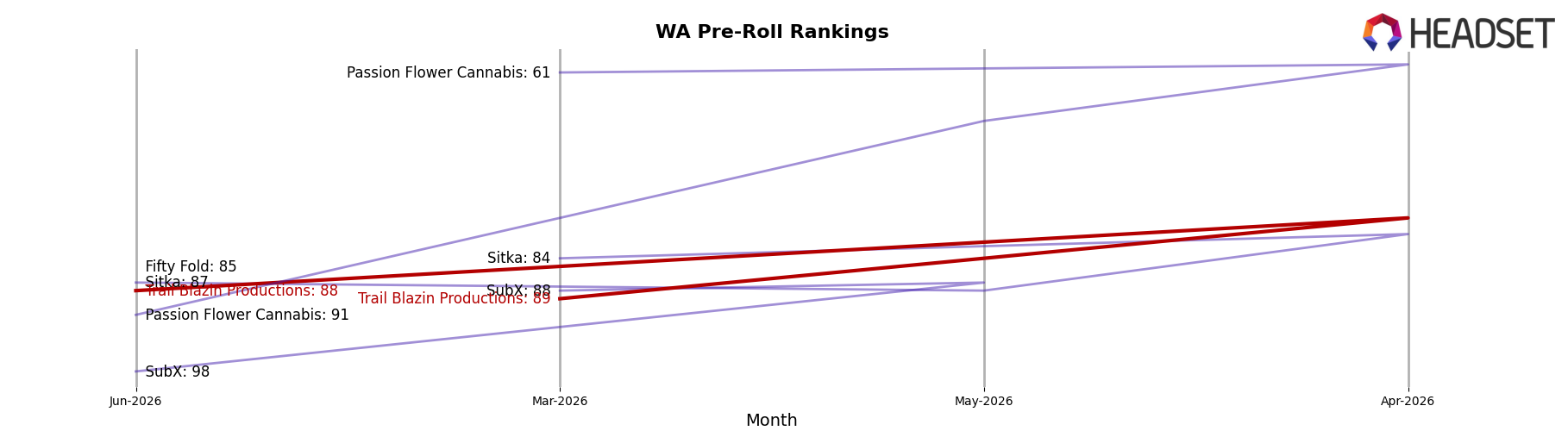

In Washington Pre-Roll, Trail Blazin Productions sits at rank 88, and the mix tilt toward a 12.72 average price in Pre-Roll versus 28.82 in Flower points to a price-access positioning rather than premium potency leadership. The vapor rebound (100.72% month-over-month) alongside continued Capsules softness (3.58% month-over-month decline) suggests opportunistic experimentation at the edges without scale impact, reinforcing that near-term share defense likely depends on sustaining Pre-Roll growth while preventing further 22.60% month-over-month erosion in Flower; the implication is a need to anchor around value-tier convenience where rank 88 leaves room to climb by converting Pre-Roll momentum into repeat velocity.

Competitive Landscape

Trail Blazin Productions sits at rank #88 in WA Pre-Roll in June 2026, improving 5 positions from #93 year over year, yet slipping 1 place from #89 in March 2026; the brand remains well below its #53 peak from June 2024, a 35-rank decline from that high. Competitive movement is tightening at the top: Ooowee climbed from #2 to #1 while Phat Panda moved the other way from #1 to #2, and Lifted Cannabis Co advanced from #6 to #4 as Stingers held steady at #5, indicating ladder mobility concentrated in the top 5 while mid-tier ranks showed less churn. The pattern—modest YoY recovery of 5 ranks alongside a 35-rank gap from the prior peak and a recent 1-rank dip—implies stabilization at a lower tier rather than an imminent return to prior top-60 positioning.

Notable Products

Dutch #47 Pre-Roll 2-Pack (1.2g) posted the largest month-over-month gain at 114.7%, climbing into rank 2 while Amnesia Pre-Roll 2-Pack (1.2g) rose 71.1% to hold rank 1. Countering the surge, Northern Lights #5 Preroll 2-Pack (1.2g) fell 24.7% to rank 5 and Purple Urkle Pre-Roll 2-Pack (1.2g) dropped 38.5% to rank 9, indicating a bifurcation within the lineup. With seven of the top ten coming from the Pre-Roll category and a single Flower entry, Harlequin (3.5g), jumping 67.9% to rank 3 and generating $3,296 in June 2026, the portfolio is concentrating around Pre-Rolls while selectively lifting a value-forward Flower SKU. The pattern implies Trail Blazin Productions is consolidating around fast-turn Pre-Rolls with a targeted anchor in an accessible Flower strain to balance velocity and basket size.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.