Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

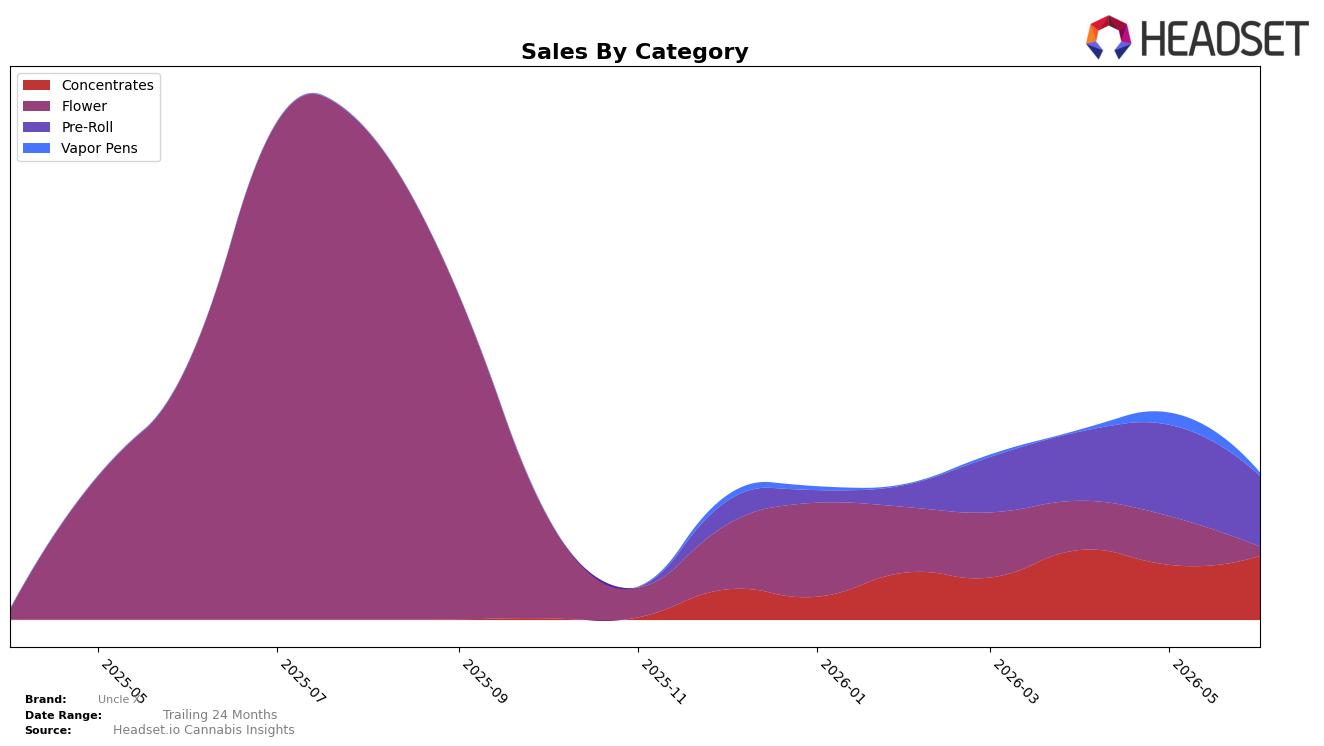

Uncle X concentrated nearly half of June 2026 sales in Pre-Roll at 48.00% share, while Concentrates accounted for 43.69%, indicating a two-category skew that tightened month over month as Pre-Roll dropped 22.91% MoM and Concentrates rose 16.30% MoM. Flower collapsed to 6.12% share with a 96.53% year-over-year decline and an 81.50% month-over-month fall, and Vapor Pens slipped to 2.18% share with a 73.09% MoM decline; alongside a 42.43% YoY reduction in average price and a 43.38% YoY sales contraction, the mix shift implies price-led retrenchment toward lower-priced formats. With Pre-Roll ranked 27 in Arizona and averaging $27.55 versus Concentrates at $19.84, the simultaneous Pre-Roll volume pullback and Concentrates uptick suggest consumers are trading down within the portfolio rather than expanding category breadth, implying margin pressure anchored in format and price tier.

The pivot toward Concentrates (+16.30% MoM) as Pre-Roll declines (−22.91% MoM) signals a repositioning from a higher-price, rank-constrained Pre-Roll presence (rank 27 in Arizona) toward value-oriented inhalables, reinforced by a 42.43% YoY average price drop that likely re-anchors consideration on deal-seeking missions. The 96.53% YoY and 81.50% MoM collapse in Flower, coupled with a 73.09% MoM Vapor Pens decline, reduces multi-category touchpoints and concentrates demand risk into two formats; this concentration, together with a 48.00% Pre-Roll share and 43.69% Concentrates share, implies Uncle X is prioritizing depth over breadth and should treat Pre-Roll as a defensible traffic driver while using Concentrates as the elasticity lever to stabilize share.

Competitive Landscape

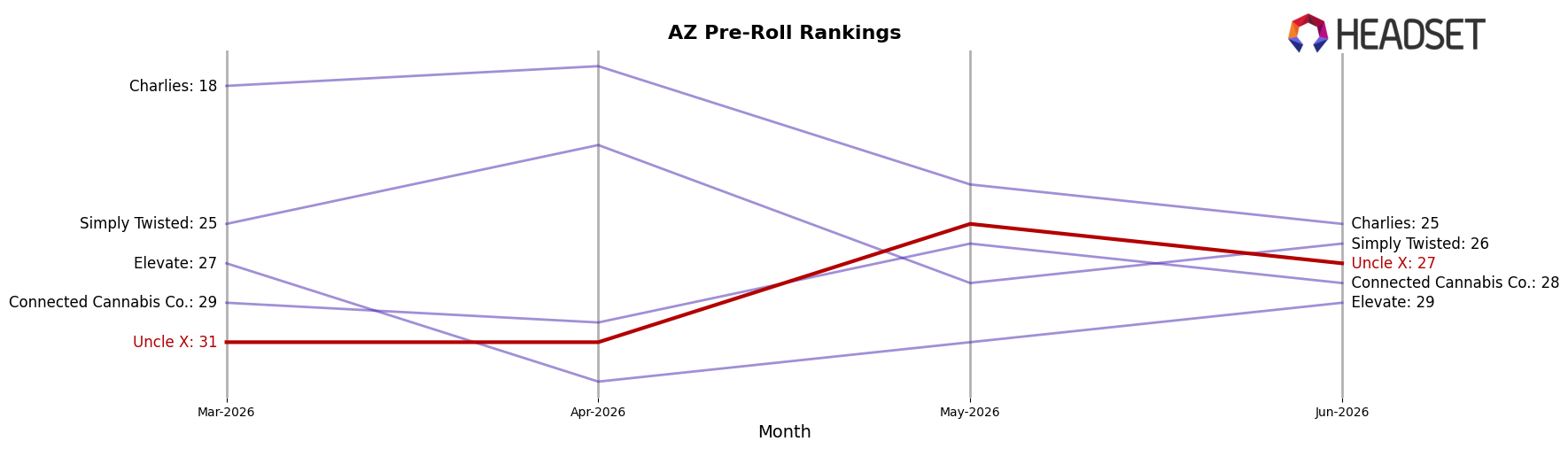

Uncle X sits at rank #27 in AZ Pre-Roll for June 2026, improving 4 positions from #31 in March 2026 and sitting 2 positions below its peak of #25 in May 2026. In directional context, Jeeter holds #1 with a 32.6% year-over-year sales increase while STIIIZY is at #2 with a -4.2% year-over-year change, indicating Uncle X’s two-position pullback from May 2026 to June 2026 occurred amid mixed momentum at the top. The pattern implies Uncle X’s recent rise from #31 to #27 is more about incremental share capture than a category-wide tide, suggesting future gains will depend on sustaining month-over-month rank lifts rather than expecting displacement of top-5 incumbents.

Notable Products

Gastro Pop #4 Pre-Roll 14-Pack (7g) posted the headline movement in June 2026 with a +23.3% month-over-month gain to rank 2, while Axilla Pre-Roll 28-Pack (14g) held rank 1 with a 0-rank delta and no reported month-over-month rate, signaling that momentum is accruing below the top slot rather than expanding the lead. Four of the top ten are Pre-Roll SKUs while six are Concentrates, and the highest-ranked Concentrate, Peanut Butter Gelato Sugar (1g), sits at rank 3 with a 0-rank delta and no month-over-month rate, indicating that share-of-attention is clustering at the category poles rather than diversifying across mid-tier items. The Gastro Pop #4 Badder (5g) in Concentrates placed at rank 6 without a stated month-over-month change, contrasting with the +23.3% lift in its Pre-Roll sibling at rank 2, which implies product-form elasticity within the same strain family. Overall, the mix points to Uncle X leaning into larger pack Pre-Rolls for scalable velocity while keeping Concentrates broad for basket variety, a direction that prioritizes high-frequency formats over experimentation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.