Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

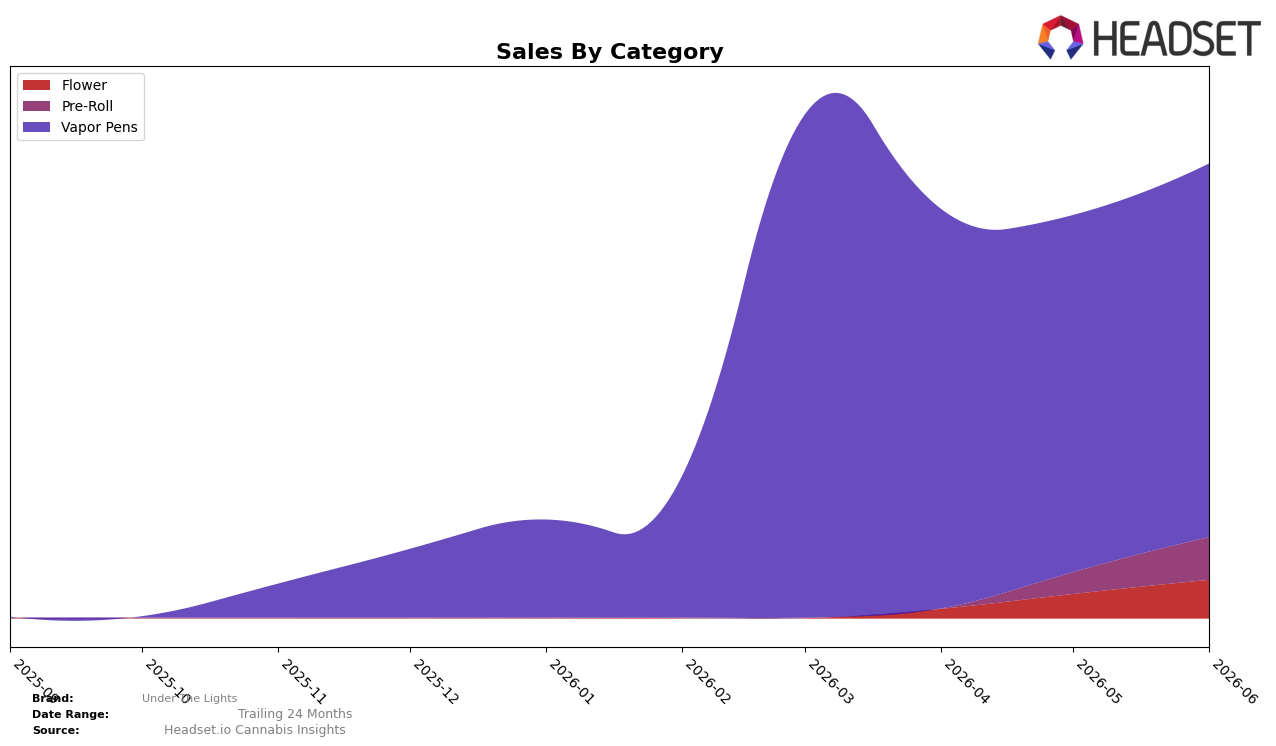

Under The Lights concentrated 82.25% of June 2026 sales in Vapor Pens while Pre-Roll and Flower accounted for 9.31% and 8.45%, respectively, indicating a portfolio still anchored to a single category despite rapid month-over-month changes. Vapor Pens grew 4.65% MoM, contrasted with 97.57% MoM in Pre-Roll and 58.75% MoM in Flower, a mix shift that lifted smaller formats faster than the core. Average prices diverged by category at $40.69 for Vapor Pens versus $27.99 for Pre-Roll and $64.84 for Flower, implying different velocity-to-price tradeoffs across segments. In Illinois Vapor Pens, a rank of 29 suggests mid-pack placement where incremental share gains may require balancing growth in Pre-Roll’s 9.31% share against the 82.25% Vapor Pen base; the pattern implies near-term upside comes from sustaining Pre-Roll’s 97.57% MoM surge without eroding the Vapor Pen anchor.

The acceleration in Pre-Roll (+97.57% MoM) and Flower (+58.75% MoM) alongside a modest +4.65% MoM in Vapor Pens implies Under The Lights is broadening trial beyond its core, with category elasticity favoring lower ticket Pre-Rolls at $27.99 and premium basket builders in Flower at $64.84. With Vapor Pens still at 82.25% share and ranked 29 in Illinois, maintaining visibility in the core while converting new Pre-Roll and Flower buyers into repeat purchases is the practical lever; the pattern implies positioning should shift from single-category dominance to a three-tier ladder that uses Pre-Roll for acquisition, Vapor Pens for retention, and Flower for premium trade-up.

Competitive Landscape

Under The Lights is ranked #29 in Illinois Vapor Pens in June 2026, down 5 positions from #24 in March 2026, and 5 positions below its three-month rank of #24; this contrasts with &Shine holding #1 while its year-over-year sales fell 12.7%, and Select staying at #2 with a 6.8% YoY sales decline, indicating Under The Lights lost rank share even as category leaders retained top-two positions amid contraction. With Joos steady at #3 during a 9.6% YoY sales drop and RYTHM fixed at #5 despite a 3.8% YoY dip, the brand’s slide from a peak rank of #24 to #29 implies momentum loss driven more by relative competitive stability than absolute market growth.

Notable Products

Grandaddy Purple Distillate Cartridge (1g) posted the month’s sharpest move with +112.0% MoM to rank 4, while Durban Gelato Distillate Disposable (2g) fell -15.6% to rank 5, indicating a tilt toward cartridges over disposables within Vapor Pens. OG Kush Distillate Cartridge (1g) surged +70.8% to rank 3 as Laughing Buddha Distillate Cartridge (1g) slipped -5.8% but held rank 1, signaling consolidation at the top rather than a wholesale reshuffle. Four of the top ten are Pre-Roll SKUs, led by Orange Daiquiri Pre-Roll 7-Pack (3.5g) up +68.8% at rank 6 and White Runtz Pre-Roll 7-Pack (3.5g) up +60.0% at rank 9, suggesting multi-pack Pre-Rolls are gaining traction even as Vapor Pens remain the revenue core at $34301 for the category leader. The pattern implies Under The Lights is skewing toward higher-velocity cartridges while seeding repeatable basket builders in multi-pack Pre-Rolls, setting up a two-pillar mix that prioritizes fast-moving flavors over hardware formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.