Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

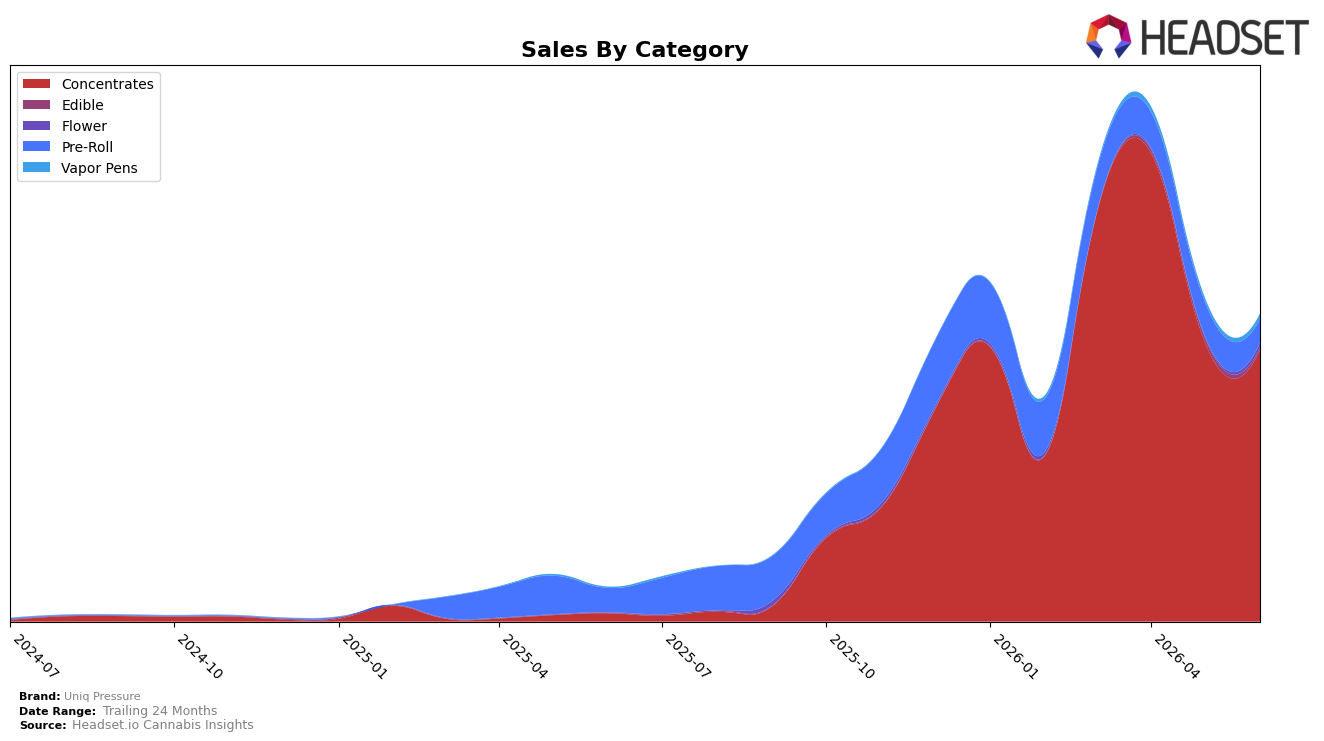

In June 2026, Uniq Pressure’s category mix is heavily concentrated, with Concentrates at 88.70% share and a 3,338.01% year-over-year surge alongside a 2.99% month-over-month dip, while Pre-Roll holds 7.70% share with a 1.78% YoY decline and a 30.15% MoM drop. Vapor Pens account for 1.58% share with 427.02% YoY growth and 29.35% MoM expansion, and Flower sits at 1.37% share with a 278.23% MoM increase against Edible’s 0.64% share and a 52.54% MoM contraction; the average price rose 85.27% YoY to $11.35. The mix implies a single-category dependency where triple-digit YoY growth in Concentrates coexists with volatile MoM swings across smaller lines, signaling that June 2026 gains are driven by Concentrates while portfolio balance is tightening rather than broadening.

That concentration coincides with a rank of 4 in Concentrates in Michigan, indicating competitive relevance at the category core while Pre-Roll’s 30.15% MoM decline and Edible’s 52.54% MoM decline weaken cross-category reach. Conversely, Vapor Pens’ 29.35% MoM growth and Flower’s 278.23% MoM spike, despite their combined 2.95% share, point to early traction levers that could mitigate risk if scaled; the thesis is that Uniq Pressure’s positioning is anchored in Concentrates leadership with rank-validated pull, but current share and MoM patterns imply limited diversification headroom unless Vapor Pens and Flower accelerate share from 1.58% and 1.37% toward double digits.

Competitive Landscape

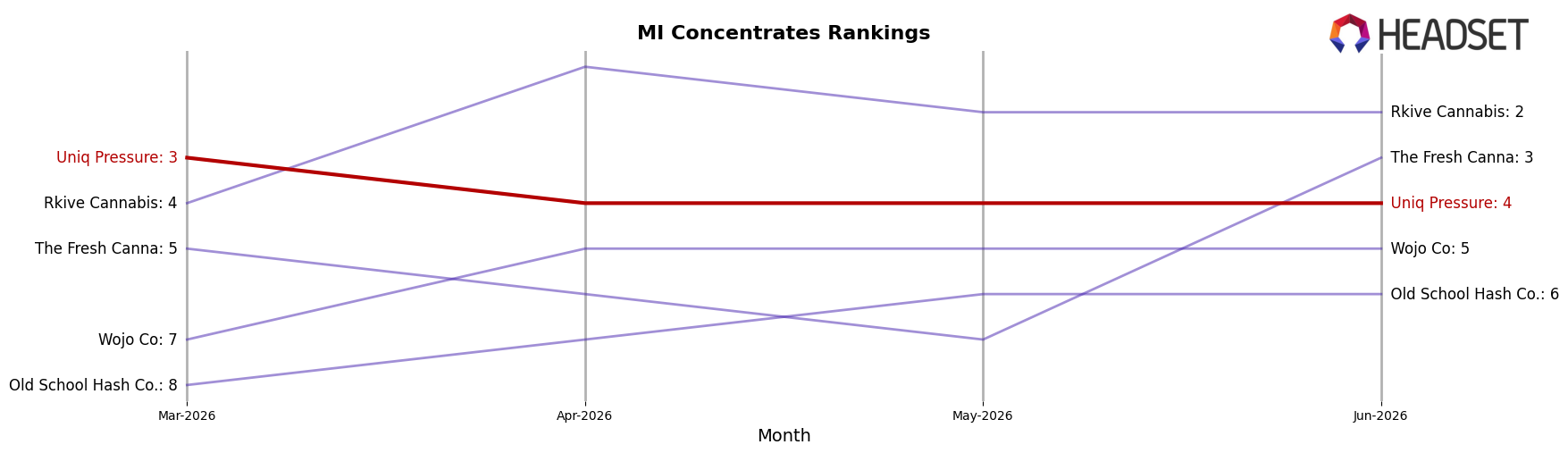

Uniq Pressure sits at rank #4 in MI Concentrates in June 2026 after a year-over-year jump of 129 positions from #133 to #4, while its three-month position eased from #3 to #4 and its best mark held at #3 in March 2026; meanwhile, The Limit held steady at #1 (flat YoY at #1) and The Fresh Canna climbed from #8 YoY to #3 as Wojo Co slipped from #3 YoY to #5 with a -9.1% sales change. With Rkive Cannabis moving from #4 YoY to #2 on 101.3% sales growth and The Fresh Canna advancing on 53.1% growth, the competitive mix tightened above Uniq Pressure, implying that the brand’s rapid rank ascent is meeting a ceiling near the top three and will require share capture from entrenched leaders to reattain #3.

Notable Products

Popz 41 Pre-Roll (1g) posted the steepest movement in June 2026 with a -51.2% month-over-month drop and sat at rank 8, while Green Crack Pre-Roll (1g) also contracted -41.0% at rank 4. Gush Mintz Bubble Hash Infused Pre-Roll (1.3g) was the lone gainer at +3.6% and held rank 2, but Super Runtz Pre-Roll (1g) slid -5.3% at rank 3. Four of the top ten are Pre-Roll SKUs concentrated in the top 9 ranks, but three logged double-digit declines and only one showed any month-over-month growth, whereas Concentrates occupied ranks 5–7 and 10 with stable placement and the single largest dollar contributor at $40,292 coming from Grape Zoda Rosin (1g). The pattern implies Uniq Pressure’s mix is tilting toward Concentrates for dependable volume while Pre-Rolls require SKU pruning and pricing or promo resets to arrest share leakage.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.