Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Rkive Cannabis is stocked at 97 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Monroe, Adrian, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

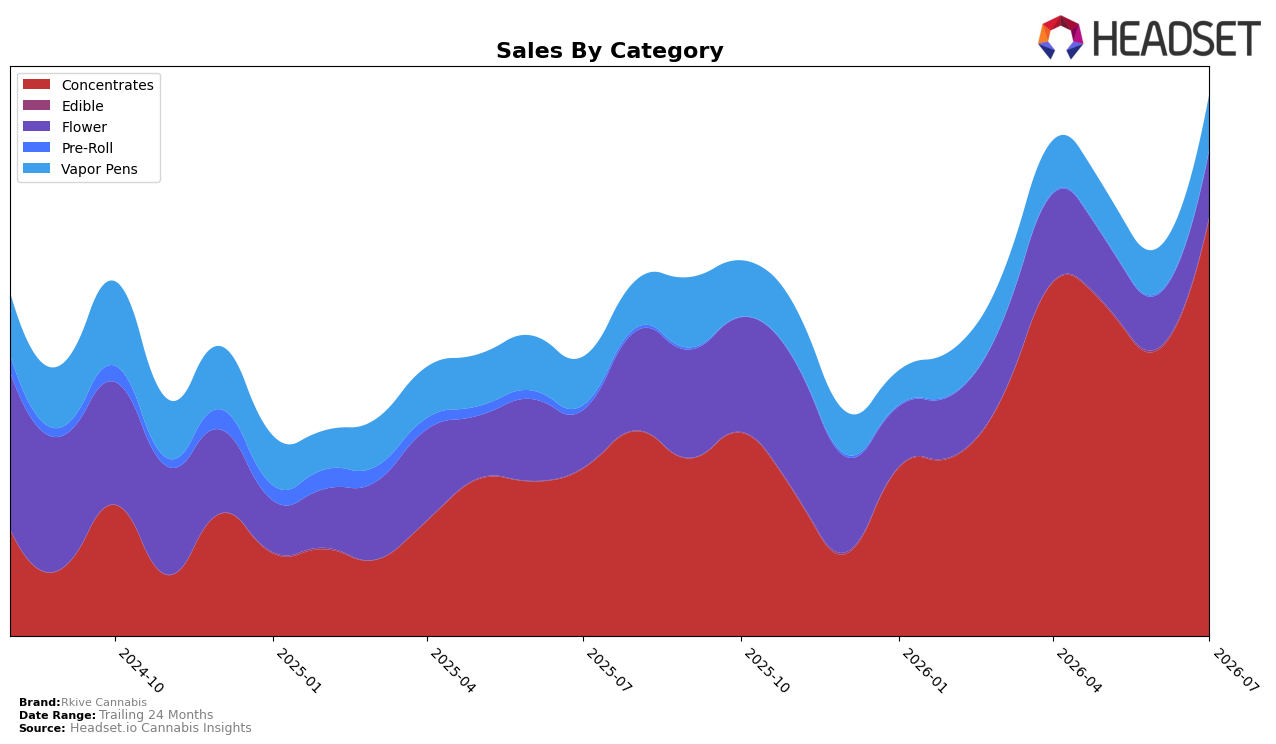

Rkive Cannabis concentrated its July 2026 sales mix in Concentrates at 77.22% share with 150.23% year-over-year growth and 46.35% month-over-month growth, while Flower held 12.20% share with 15.13% YoY and 23.82% MoM, and Vapor Pens accounted for 10.11% share with 13.36% YoY and 22.13% MoM. Minor tiers moved unevenly: Edible grew 151.52% YoY but declined 11.86% MoM at 0.25% share, and Pre-Roll contracted 73.25% YoY despite a 12.49% MoM uptick at 0.22% share. With brand-level sales up 94.95% YoY alongside a 27.89% YoY increase in average price to $35.89, the mix skews toward higher-price, faster-growing Concentrates, implying the portfolio is oriented to premium potency formats rather than breadth across inhalables.

Holding the number 1 rank in Concentrates in Michigan while keeping Flower and Vapor Pens to a combined 22.31% share positions Rkive Cannabis as a category specialist rather than a full-line generalist, and the 46.35% MoM surge in Concentrates versus 23.82% in Flower suggests shelf-space and marketing gravity continue to favor extraction SKUs. The simultaneous 151.52% YoY uptick in Edible from a 0.25% base and a 73.25% YoY decline in Pre-Roll at 0.22% share indicate peripheral experimentation without material rebalancing, so near-term competitive posture hinges on defending premium-price Concentrates leadership in Michigan while carefully pacing expansion in lower-price inhalables to avoid diluting the 27.89% YoY price lift.

Competitive Landscape

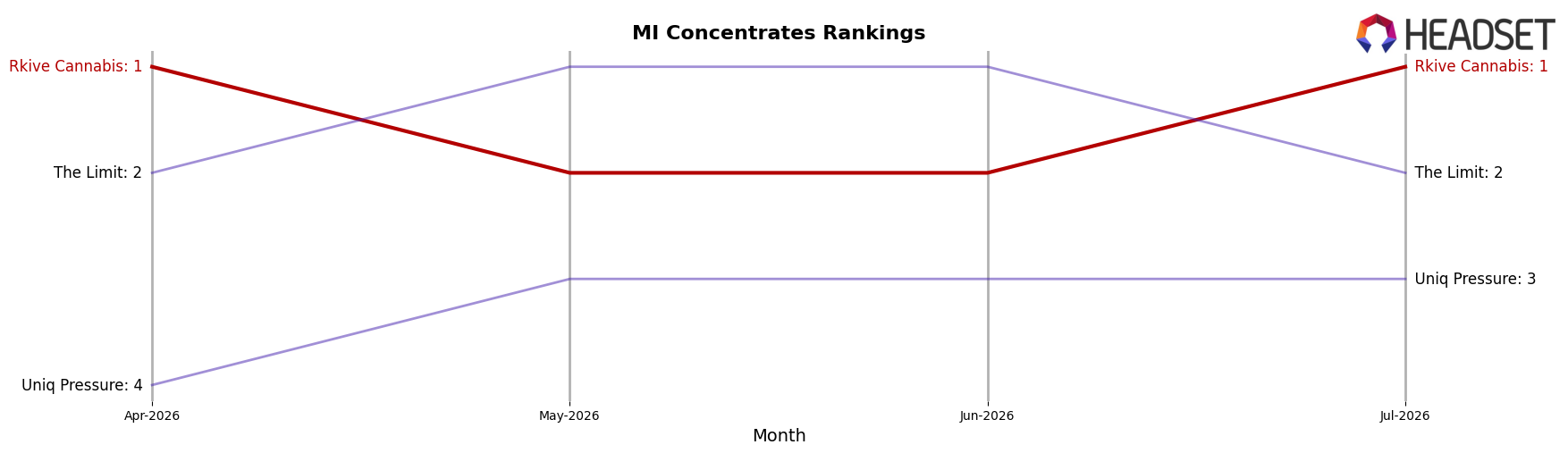

Rkive Cannabis sits at rank #1 in MI Concentrates in July 2026 after rising 4 positions year over year from #5, and it has held #1 for the past three months while hitting its peak rank #1 in July 2026; in contrast, The Limit slipped from #1 year over year to #2 with a -1.7% sales decline, and Uniq Pressure climbed from #145 to #3 with a 9,866.4% sales surge—yet still trails the top slot. The competitive middle tightened as The Fresh Canna moved from #6 to #4 on 22.0% growth while Cannalicious Labs dropped from #2 to #5 with a -29.6% contraction, indicating churn below the lead. The pattern implies Rkive Cannabis’s ascent to #1 and stability at that rank reflect share consolidation at the top even as rapid movers reshuffle ranks beneath it.

Notable Products

Black Maple (3.5g) posted the standout movement in July 2026 with a +77.4% month-over-month surge to rank 2, while Strawberry Banana Play Gummies (200mg) slipped -11.9% to rank 7, indicating divergent traction between Flower and Edible formats. Crostata Rosin Cartridge (0.5g) advanced +62.5% to rank 8, and three of the top ten are Concentrates anchored by live resin and hash rosin at ranks 1, 3, 6, and 10, pointing to a concentrate-led lineup despite Flower’s accelerating gains. The mix implies Rkive Cannabis is tilting toward higher-potency inhalables where velocity is rising fastest, with Flower breakouts complementing a concentrates core rather than displacing it.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.