Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

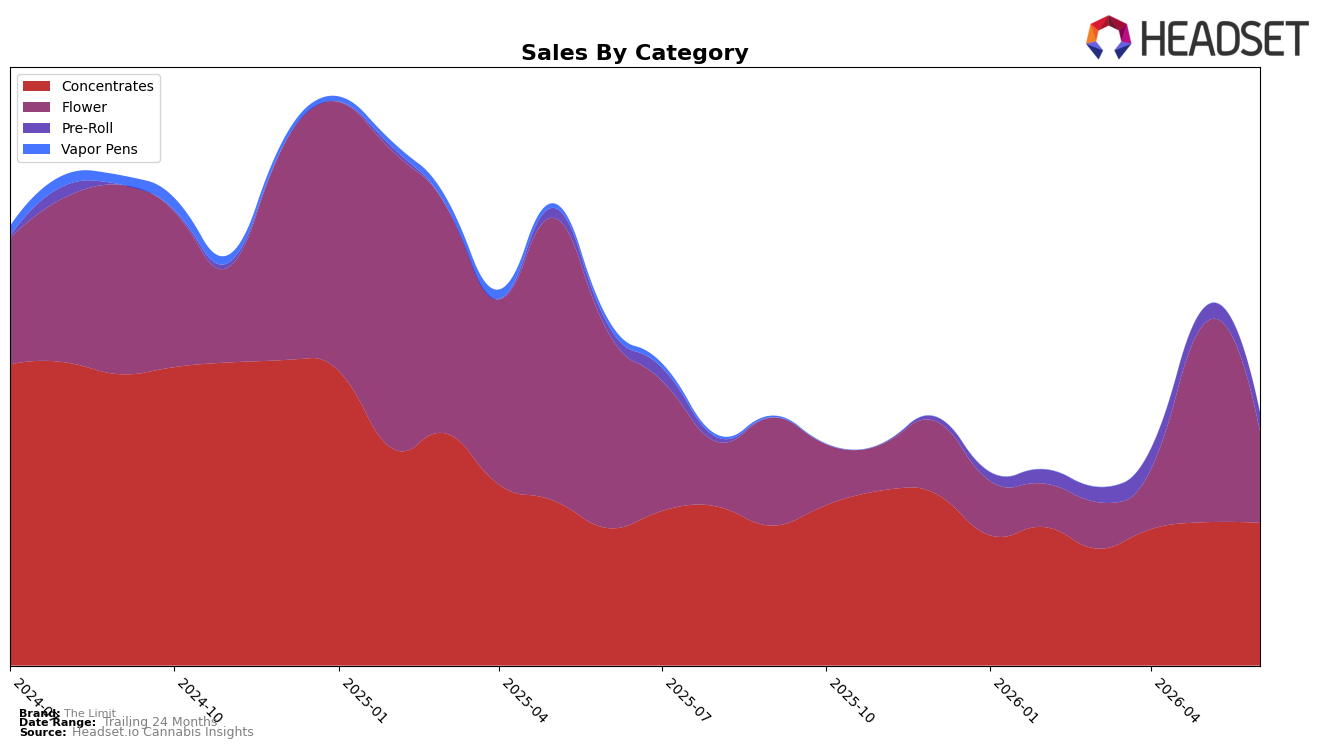

In June 2026, The Limit’s mix tilted further toward Concentrates at 56.46% share, where category sales grew 3.86% year over year despite a 0.43% month-over-month dip, while Flower contracted to 36.11% share with a 53.36% YoY decline and a 54.08% MoM drop. Pre-Roll expanded to 7.43% share on 159.81% YoY growth and 18.16% MoM growth, aided by a category-low average price of $6.13 versus $16.74 in Concentrates and $14.64 in Flower; this implies the brand is reallocating volume from a sharply retrenching Flower base into faster-growing, lower-priced Pre-Rolls while defending its leading Concentrates position at rank 1 in Michigan.

With average price down 14.32% year over year to $14.18 and overall brand sales down 26.84% YoY, the 3.86% YoY gain in Concentrates and 159.81% YoY surge in Pre-Roll indicate a price-led, value-seeking shift that offsets some of Flower’s 53.36% YoY decline. The Limit’s number 1 rank in Concentrates in Michigan combined with an 18.16% MoM lift in Pre-Roll suggests a barbell positioning: premium-leaning Concentrates anchoring share, paired with aggressively priced Pre-Rolls to capture trade-down, implying the brand’s path to stabilizing the 26.84% YoY sales contraction depends on sustaining Concentrates leadership while scaling Pre-Roll without further compressing mix margin.

Competitive Landscape

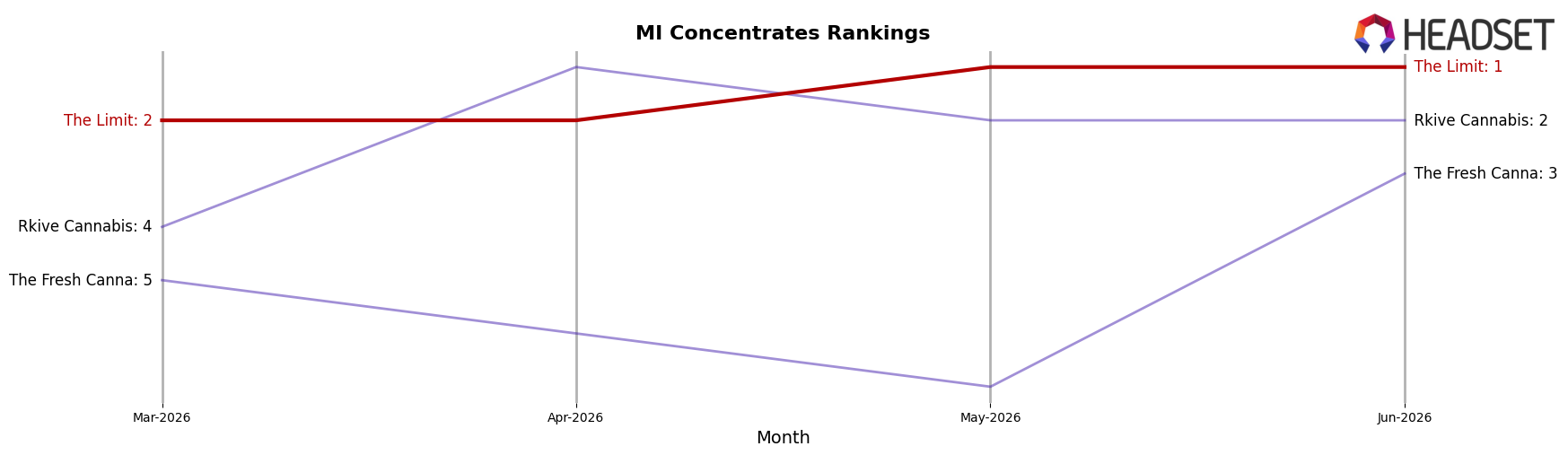

The Limit holds rank #1 in MI Concentrates in June 2026, unchanged from rank #1 in June 2025, after rising from #2 in March 2026 to its peak at #1 in June 2026; this stability contrasts with Rkive Cannabis improving from #4 to #2 year over year while Uniq Pressure surged from #133 to #4 with a 3338% YoY sales increase. Meanwhile, The Fresh Canna climbed from #8 to #3 alongside a 53% YoY sales gain, whereas Wojo Co slipped from #3 to #5 with a 9% YoY sales decline; together these moves indicate The Limit’s flat YoY rank at #1 masks tightening pressure from faster-rising challengers and implies that maintaining leadership will require defending against rapid share capture just below the top spot.

Notable Products

Candy Gas (28g) set the tone in June 2026 with a -37.2% month-over-month drop while holding rank 1, a sharper decline than Cotton Candy Gelato (28g) at -10.7% from rank 5, signaling volume concentration at the top despite contraction. Gelato 33 (28g) in rank 3 inched up +6.0% MoM, but Flower still accounts for six of the top ten SKUs, indicating a category-heavy mix even as the flagship softens. Among Concentrates, Tahitian Dream Live Resin (5g) fell -14.4% at rank 8 while Bixcotti Live Resin (5g) debuted at rank 2 with $45,465, pointing to a pivot where premium Concentrates cushion volatility in legacy Flower. The pattern implies The Limit is leaning into higher-rank Concentrates to offset sharp MoM swings in top Flower SKUs, setting a course toward a more balanced, margin-protective mix.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.