Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

K Savage (WA) is stocked at 109 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Everett, and Lynnwood. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

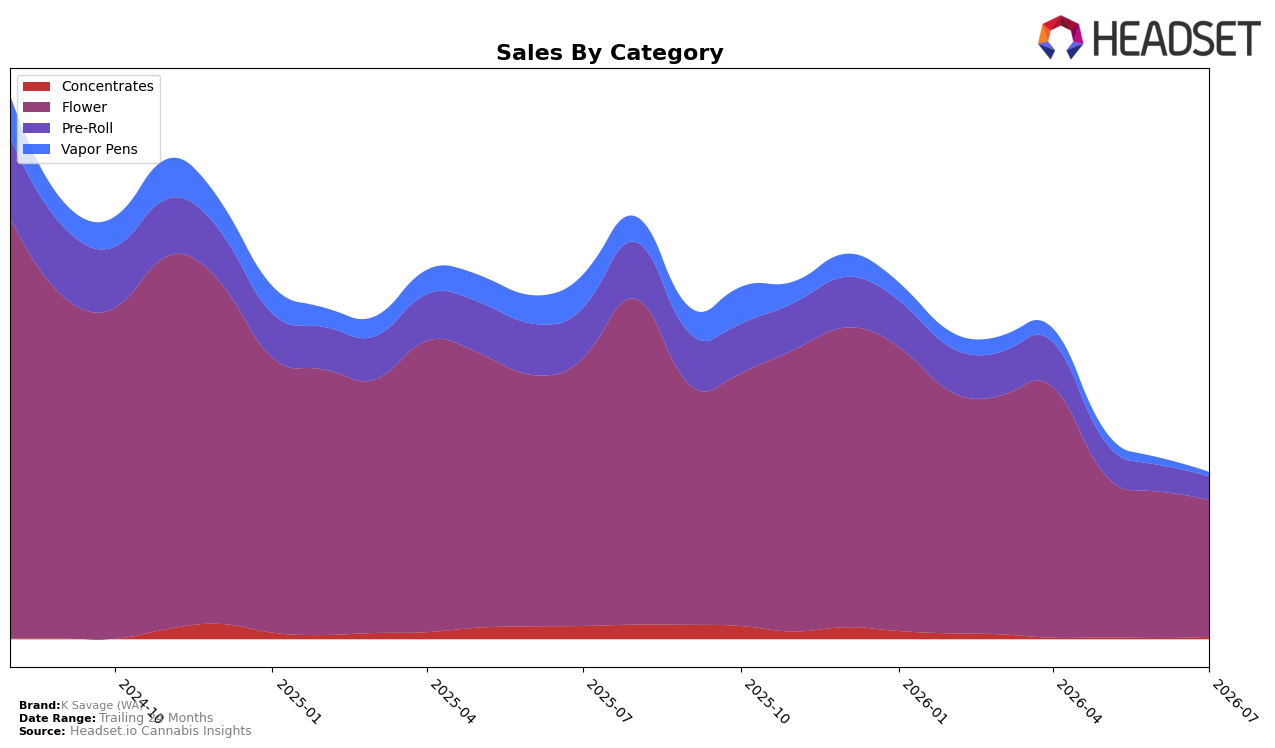

K Savage (WA) concentrated 81.59% of July 2026 sales in Flower, with Pre-Roll at 14.32% and Vapor Pens and Concentrates combining for 4.09%; the category mix shifted as Vapor Pens fell 41.96% month over month and 86.74% year over year while Concentrates jumped 86.54% month over month but remained down 81.60% year over year. Within core categories, Flower declined 6.68% month over month and 49.00% year over year and Pre-Roll slid 10.53% month over month and 52.42% year over year, pointing to a narrowing portfolio centered on Flower despite broad contraction.

The tilt toward Flower, alongside a category rank of 35 in Flower in Washington and a 3.84% year-over-year drop in average price, indicates value-led positioning is being used to defend share rather than expand into higher-price formats. With Vapor Pens shrinking to 2.62% share and Concentrates at 1.47% share, the brand’s mix shift reduces exposure to premium-adjacent formats even as Concentrates post a short-term 86.54% month-over-month rebound, implying near-term focus on stabilizing Flower while treating non-Flower as opportunistic rather than growth engines.

Competitive Landscape

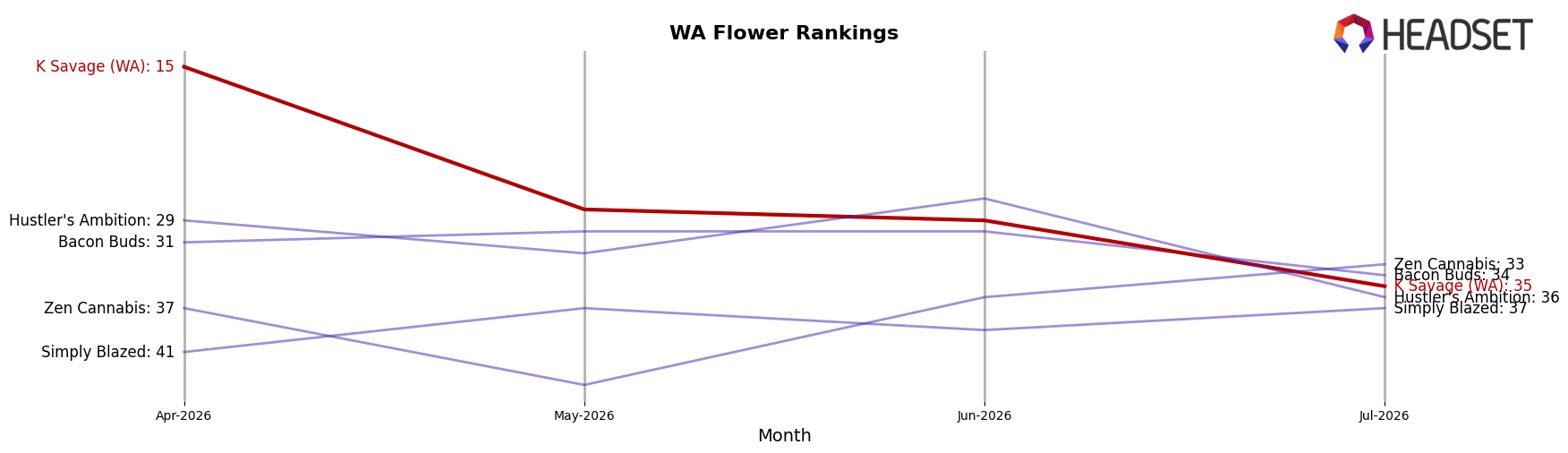

K Savage (WA) sits at rank #35 in WA Flower in July 2026, down 20 positions from #15 in July 2025 and down 20 from #15 just three months ago in April 2026, while its peak of #8 in November 2024 underscores a multi-quarter slide; meanwhile, Phat Panda held #1 year-over-year at #1 with sales up 18.6%, and Lifted Cannabis Co climbed from #8 to #3 with sales up 13.1%, contrasting with K Savage (WA)’s 20-rank retreat and placing it further from the top-5 corridor, implying the brand is ceding share to faster-rising leaders and will need a corrective strategy to arrest rank attrition.

Notable Products

Angela Pre-Roll 2-Pack (1g) posted the steepest decline at -31.3% MoM while dropping to rank 2, and Lilac Wine Pre-Roll 2-Pack (1g) fell -34.0% MoM while sitting at rank 5, together signaling a July 2026 retrenchment in Pre-Rolls despite GMO Pre-Roll 2-Pack (1g) holding rank 1 with +8.5% MoM. In contrast, Lilac Wine (3.5g) rose +11.1% to rank 3 and Blue Lobster (3.5g) gained +8.8% at rank 8, while Pink Ink (3.5g) slipped -13.3% at rank 9, implying that Flower is absorbing demand even as select SKUs wobble. Four of the top ten are Flower SKUs and three are Pre-Rolls, but the balance of growth sits with Flower where Angela (3.5g) advanced +4.1% at rank 4 and GMO (3.5g) added +5.2% at rank 6, with total July 2026 Flower sales across these leaders exceeding $84,000. The pattern implies K Savage (WA) is tilting toward premium eighths as the steadier volume engine while Pre-Rolls concentrate into one hero SKU rather than a broad lineup.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.