Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

WA Grower is stocked at 15 licensed dispensaries across Washington, with the deepest coverage in Vancouver, Elma, Lacey, Longview, and Olympia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

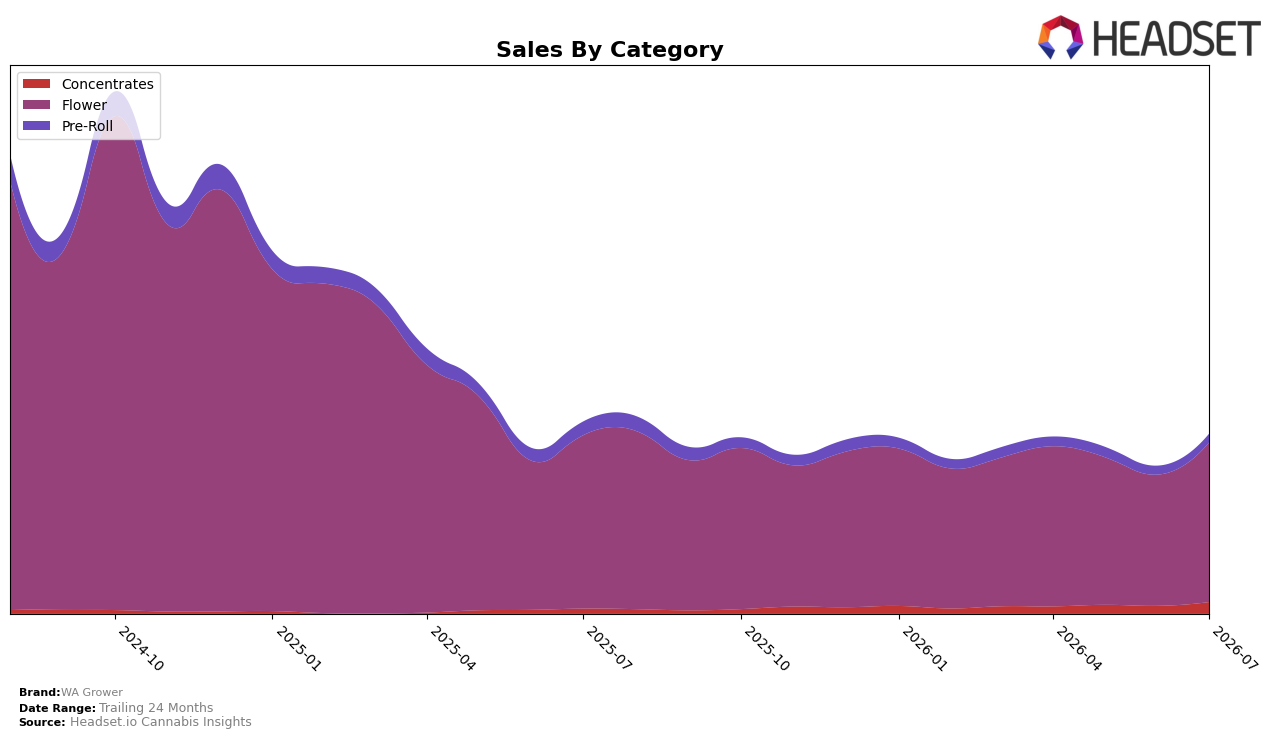

WA Grower concentrated 88.64% of July 2026 sales in Flower while holding 6.50% in Concentrates and 4.86% in Pre-Roll, and the brand’s Flower rank sat at position 30 in Washington. Flower contracted year over year by 7.94% but expanded month over month by 21.57%, Concentrates surged 126.68% YoY and 47.78% MoM, and Pre-Roll fell 36.03% YoY and 1.42% MoM; this mix shift implies the brand is leaning into a two-pillar portfolio where Flower volume recovery is complemented by a fast-growing but still small Concentrates line, while Pre-Roll remains a drag.

Given overall brand sales down 6.32% YoY and average price nearly flat at -0.16% YoY, the 21.57% MoM lift in Flower alongside a 47.78% MoM lift in Concentrates suggests volume-led stabilization rather than price-driven gains, and the 30th-place Flower rank signals mid-pack visibility that depends on sustaining the Concentrates acceleration. With Flower still at 88.64% share and Pre-Roll shrinking 36.03% YoY, the path to improved positioning is to convert Concentrates’ 6.50% share into low-teens while protecting Flower’s rank, since the current mix concentration magnifies category-specific volatility.

Competitive Landscape

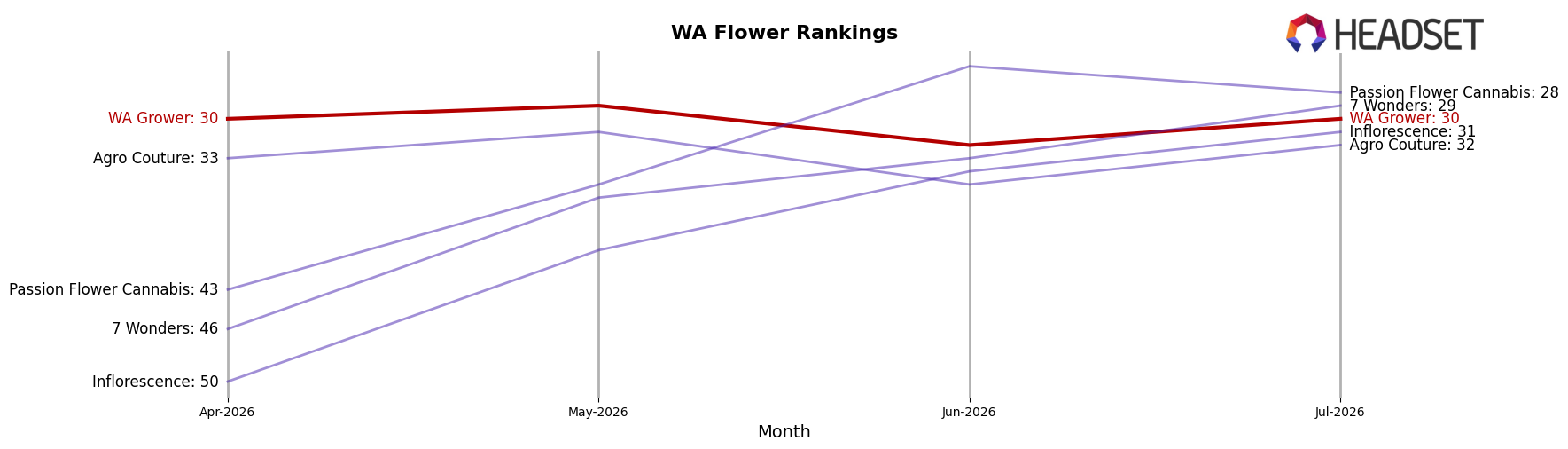

WA Grower is ranked #30 in WA Flower in July 2026, down 1 position year over year from #29, and flat versus April 2026 when it also sat at #30; this sits far from its peak of #6 in December 2024, indicating a 24-place slide from that high-water mark. In contrast, Phat Panda held #1 year over year with sales up 18.6%, while Legends stayed at #2 despite a 22.9% sales decline, and Sweetwater Farms climbed from #14 to #5 on 48.2% growth—movement that brackets WA Grower’s stagnant three-month rank at #30 and suggests its competitive position is being set more by rivals’ double-digit swings than by its own momentum. The pattern implies WA Grower’s trajectory is one of stability at a lower tier rather than recovery toward the top 10, and without a catalyst that changes relative velocity against rising brands, the probability of reclaiming anything near the December 2024 rank looks low.

Notable Products

Indica RSO (1g) posted the largest month-over-month move in July 2026 at +89%, vaulting to rank 2, while Gorilla Glue #4 (3.5g) rose +86% to rank 1; with Blue Dream (7g) up +32% at rank 6, the outsized gains clustered at the top rather than the middle. Flower dominates breadth—six of the top ten are Flower SKUs—yet the lone Concentrates entry at rank 2 signals category mix diversification despite Flower’s rank concentration. The double surge at ranks 1 and 2, alongside modest Flower growth bands of +14% and +3% deeper in the set, implies WA Grower is tilting the portfolio toward a few momentum leaders while testing non-Flower traction to lift overall velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.