Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

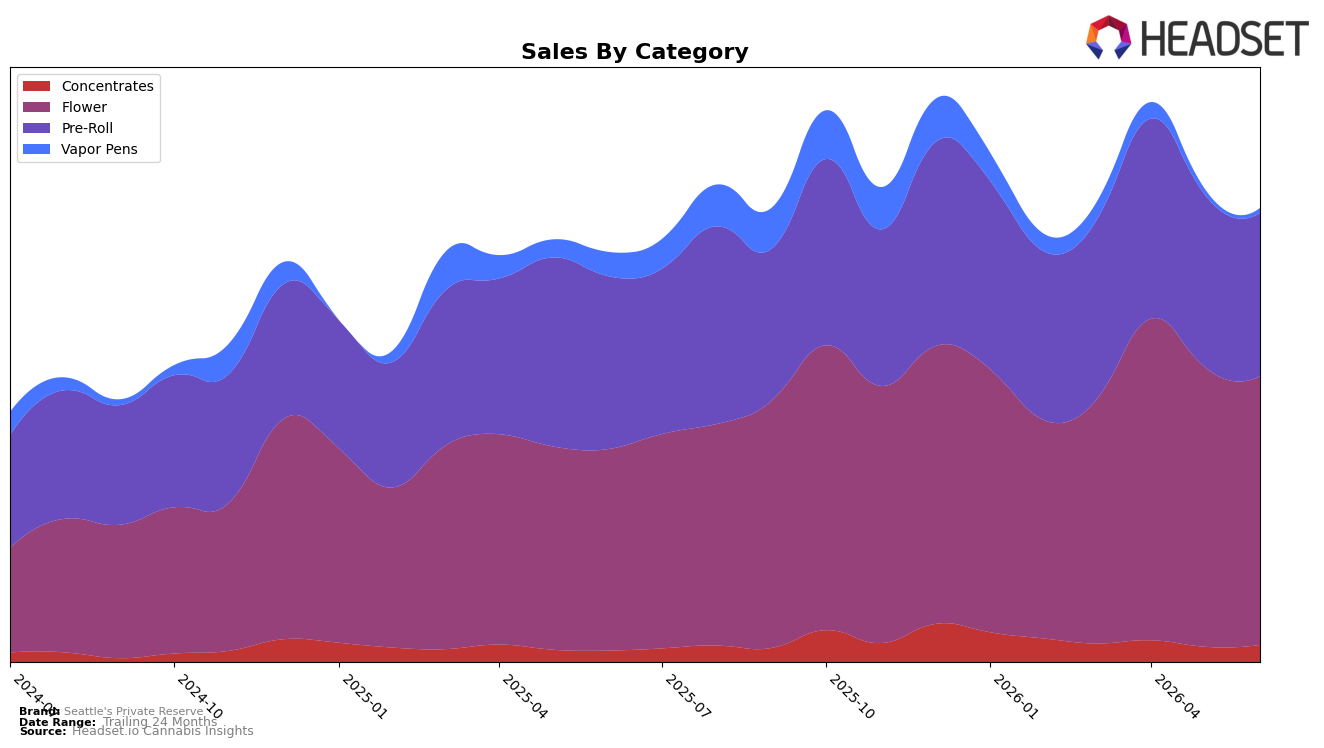

In June 2026, Seattle's Private Reserve leaned into Flower at 52.45% share with year-over-year growth of 29.32% but a month-over-month dip of 3.60%, while Pre-Roll held 33.80% share with a 4.81% YoY decline and a 4.66% MoM decline; Concentrates rose 14.46% YoY and 4.18% MoM to 7.96% share, and Vapor Pens fell 37.18% YoY and 2.22% MoM to 5.80% share. With brand-level sales up 8.41% YoY and average price up 0.70%, the mix indicates dependence on Flower offsets contraction in Pre-Roll and Vapor Pens, implying a portfolio tilting toward higher-growth inhalables where Flower expansion can carry overall momentum despite short-term MoM softness.

Given a Flower rank of 24 in Washington and average Flower pricing at $21.19 versus a brand-wide average price of $12.51, the brand is positioned mid-pack on premiumized Flower while maintaining volume via lower-priced Pre-Rolls at $6.81. The shift—Flower gaining YoY share while Pre-Roll and Vapor Pens retract and Concentrates advance 14.46% YoY—suggests prioritizing Flower-led differentiation and selective investment in Concentrates to diversify risk, using Flower’s scale to fund categories with improving traction and de-emphasizing Vapor Pens where a 37.18% YoY drop signals weak fit.

Competitive Landscape

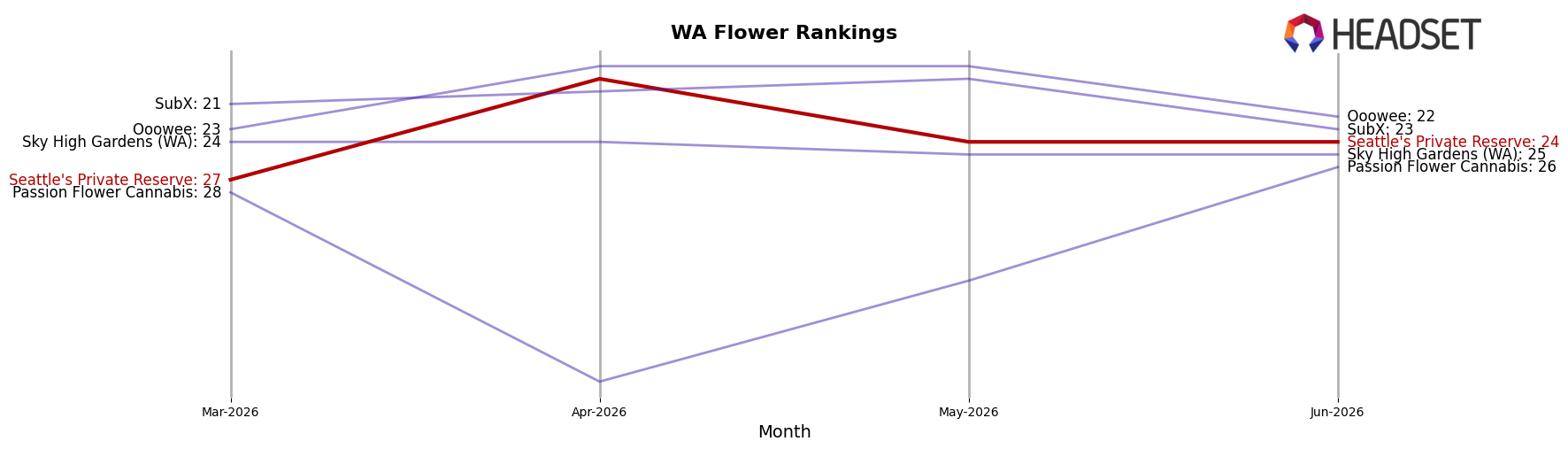

Seattle's Private Reserve sits at rank #24 in June 2026, up 7 positions from #31 year over year, but down 5 spots from its April 2026 peak at #19, signaling mid-year slippage after earlier gains; meanwhile, three-month movement from #27 to #24 represents a 3-rank improvement, contrasted with Phat Panda holding #1 with a 16.6% year-over-year sales increase and Lifted Cannabis Co rising from #8 to #3 alongside a 17.9% sales lift, indicating that climbing peers are compressing room above while Seattle's Private Reserve’s trajectory implies gradual improvement but insufficient momentum to defend April 2026’s higher watermark without a sharper share capture.

Notable Products

Cake Frosting Pre-Roll 2-Pack (2g) delivered the standout movement in June 2026 with +137.6% month over month to rank 1, while Cake Frosting (3.5g) rose +68.2% to rank 2, indicating a unified strain-led surge across both Pre-Roll and Flower. Sour Diesel Pre-Roll 2-Pack (2g) climbed +79.0% to rank 3 as Gushers Pre-Roll 2-Pack (2g) slipped -6.7% at rank 4, and Frankenstein Pre-Roll 2-Pack (2g) dropped -14.9% at rank 9, signaling a bifurcation between gains at the top and attrition in the lower ranks. With eight of the top ten in Pre-Roll and only one Flower SKU in the top two, the assortment is concentrating around multi-pack Pre-Rolls even as a single Flower SKU contributes $29,058, pointing to a two-pronged strategy of value-led Pre-Roll volume and a flagship Flower anchor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.