Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

White Label Extracts (OR) is stocked at 245 licensed dispensaries across Oregon, with the deepest coverage in Portland, Eugene, Salem, Bend, and Medford. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

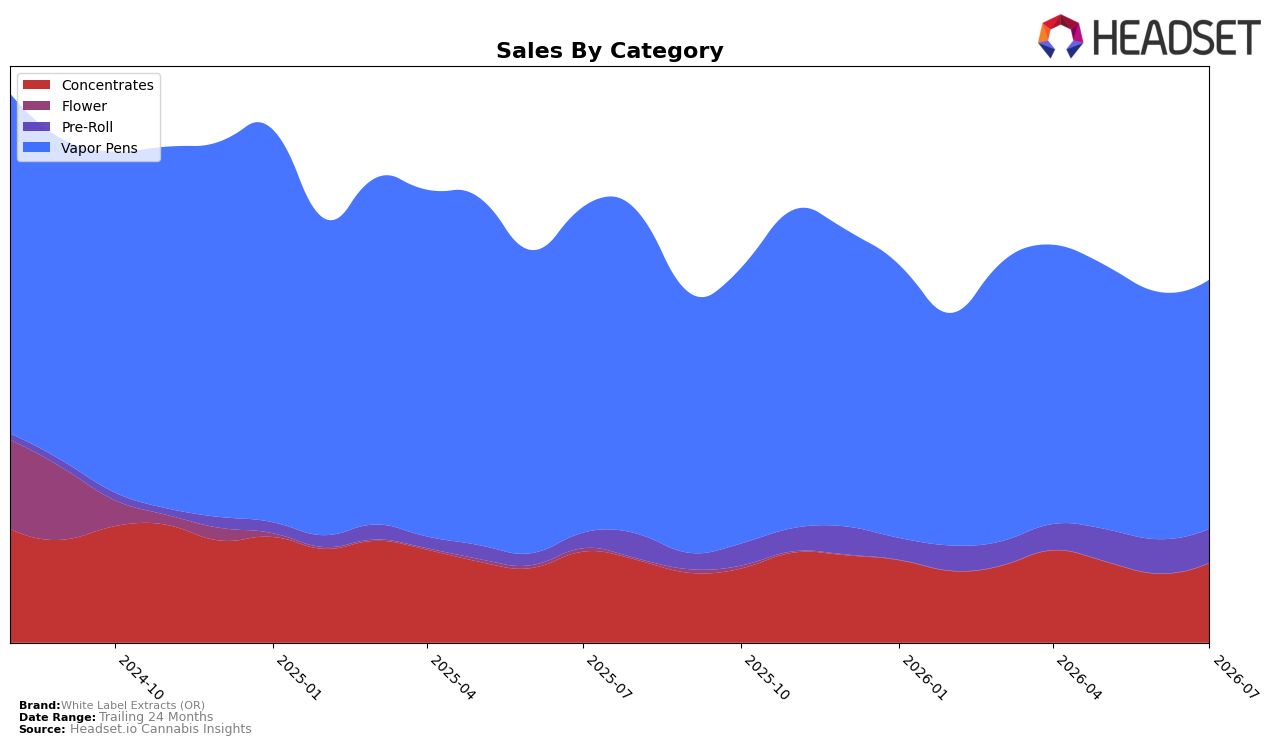

White Label Extracts (OR) concentrated 68.81% of July 2026 sales in Vapor Pens, where year-over-year sales fell 23.52% while month-over-month sales inched up 0.76%; Concentrates held 21.95% share with a 12.51% year-over-year decline but a 15.70% month-over-month gain. Pre-Roll expanded to 9.24% share on a 119.93% year-over-year surge despite a 1.22% month-over-month slip, and the brand’s overall average price was down 13.97% year over year while total brand sales declined 16.73% year over year. Taken together, the tilt toward Vapor Pens alongside accelerating Concentrates and a sharply expanding Pre-Roll base implies a portfolio in transition that is leaning on lower-priced formats to offset weakness in its largest category in Oregon.

Within Vapor Pens, an 11th place rank in Oregon sets a mid-pack benchmark, while the 0.76% month-over-month uptick contrasts with the 23.52% year-over-year drop, and Concentrates’ 15.70% month-over-month rise against a 12.51% year-over-year decline points to near-term traction from pricing at $20.07 and $16.08 average price levels, respectively. With Pre-Roll’s 119.93% year-over-year growth building a 9.24% share despite a 1.22% month-over-month dip and the brand’s 24-month sales down 24.92%, the pattern suggests positioning that prioritizes accessible price tiers to reclaim volume while using Pre-Roll as an entry point to rebuild household penetration.

Competitive Landscape

White Label Extracts (OR) sits at rank #11 in OR Vapor Pens in July 2026, sliding 5 positions year over year from #6 while easing 1 spot since April 2026 from #10, and the gap from its peak at #3 in December 2024 signals a multi-quarter retreat; meanwhile, Buddies climbed to #1 from #2 with 17.3% YoY sales growth and Entourage Cannabis / CBDiscovery fell to #2 from #1 with a 33.4% YoY sales decline, indicating leadership churn at the top that White Label Extracts (OR) hasn’t capitalized on. The combination of a 5-rank YoY drop and a 1-rank three-month dip implies a trajectory toward mid-tier status unless mix, pricing, or distribution changes reverse the share drift.

Notable Products

Glitter Bomb x Sluricane Infused Pre-Roll (1g) posted the steepest decline at -24.9% month over month and slid to rank 2, while Permafrost x Where's My Bike Live Resin Infused Pre-Roll (1g) fell -15.4% to rank 7, signaling demand compression in infused pre-rolls despite Honeycomb Pave x Apricot Honey Bun Infused Pre-Roll (1g) gaining 15.1% at rank 4. Four of the top ten are Pre-Roll SKUs, but Vapor Pens held tighter retention with Haze Liquid Live Resin Cartridge (1g) down only -8.8% at rank 9 and Citrique Live Resin Cartridge (1g) stable at rank 5, pointing to relatively steadier pen loyalty versus more volatile infused pre-rolls. With Blueberry Muffins x Grape Crepe Live Resin Infused Pre-Roll (1g) at rank 1 and a $4,806 sales print, the mix concentrates at the top around a single infused pre-roll while mid-pack softness widens, implying the brand should lean into hero SKUs in Pre-Roll while shoring up depth and consistency in Vapor Pens to smooth month-to-month swings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.