Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Zzzonked is stocked at 157 licensed dispensaries across Massachusetts, New Jersey, and 3 other states, 105 of them in Massachusetts, with the deepest coverage in Worcester, Fall River, Quincy, Marlboro, and Taunton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

Zzzonked’s July 2026 mix is concentrated in Edible at 99.63% share, with Edible sales up 1.93% month over month but down 4.68% year over year, while Tincture & Sublingual holds 0.37% share with a 35.26% MoM decline and a 34.16% YoY decline. Despite a 9.20% YoY drop in average price to $23.14, overall brand sales are down 4.84% YoY and up 23.21% over 24 months, indicating pricing has been used to defend volume as Edible stabilizes MoM and Tincture & Sublingual contracts further.

Within Edible in Massachusetts, Zzzonked holds rank 9, and the 1.93% MoM lift in its 99.63% category anchor suggests short-term momentum, while the 4.68% YoY dip signals ongoing pressure that required a 9.20% price reduction. The collapse in Tincture & Sublingual share to 0.37% alongside a 35.26% MoM decline implies the brand’s positioning is consolidating around value-forward Edibles, where price elasticity is supportive, and away from smaller adjacencies that are not sustaining rank or mix.

Competitive Landscape

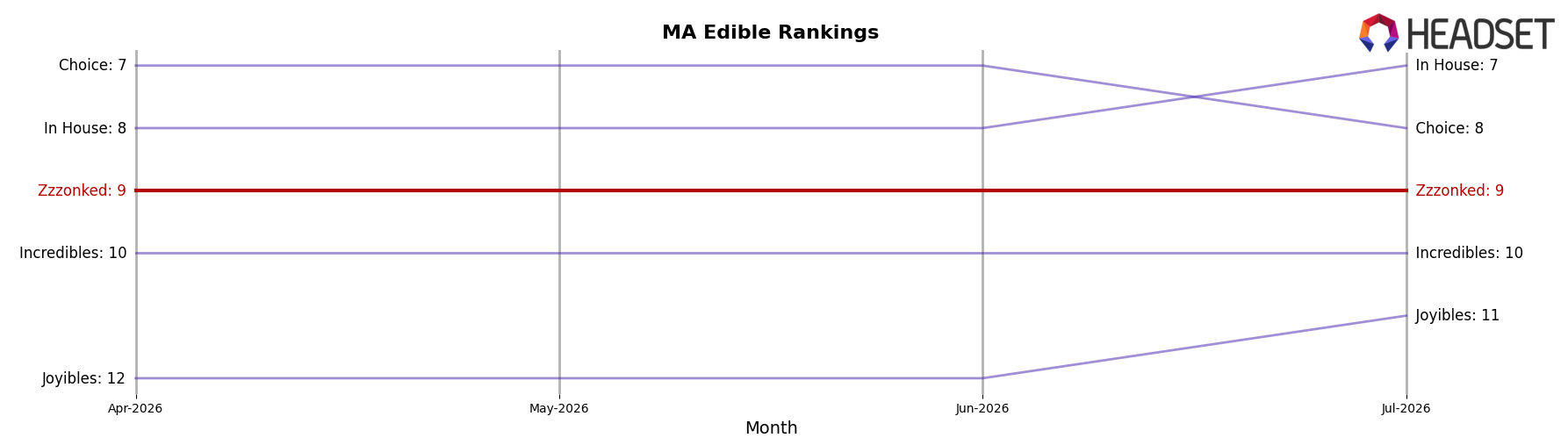

Zzzonked sits at #9 in Massachusetts Edible for July 2026, unchanged YoY from #9, while its peak of #7 in August 2024 has not been revisited and its 3‑month rank also held at #9, indicating flat positioning amid shifting leaders; in contrast, Camino moved from #2 to #1 with 42.46% YoY sales growth and Wyld climbed from #5 to #3 alongside 29.71% YoY sales growth, signaling that competitors are converting share gains as Zzzonked neither advanced in rank nor capitalized on category momentum, implying that the current trajectory locks the brand into a mid‑tier slot unless a share-accretive move changes the ranking spread.

Notable Products

CBD/THC/CBN Sleepy Tincture (150mg CBD, 150mg THC, 450mg CBN, 30ml) posted the steepest downturn in July 2026 at -35.3% MoM while sliding to rank 5, contrasting with the category core where CBD/THC/CBN 1:1:1 Sleepy Pineapple Dreams Gummies 20-Pack rose +16.5% MoM to hold rank 4. At the top, CBD/THC/CBN 1:1:1 Sleepy Mixed Berry Gummies 20-Pack grew +9.2% MoM at rank 1, whereas CBD/THC/CBN 1:1:1 Tutti Frutti Sleepy Gummies 20-Pack fell -14.6% MoM at rank 3, and four of the top ten are Edible SKUs concentrated in 1:1:1 sleep formulations. The legacy Pineapple Dream Gummies 10-Pack dropped -76.3% MoM at rank 6 on just $579, indicating SKU rationalization pressure at the lower price tier. The pattern implies Zzzonked is consolidating around high-rank 1:1:1 Edible sleep formats while deprioritizing tinctures and niche 10-packs, signaling a tilt toward flavor-led, multi-cannabinoid gummies as the commercial backbone.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.