Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

7 SEAZ is stocked at 20 licensed dispensaries across New York, with the deepest coverage in New York, Albany, Arlington, Bay Ridge, and Bronx. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

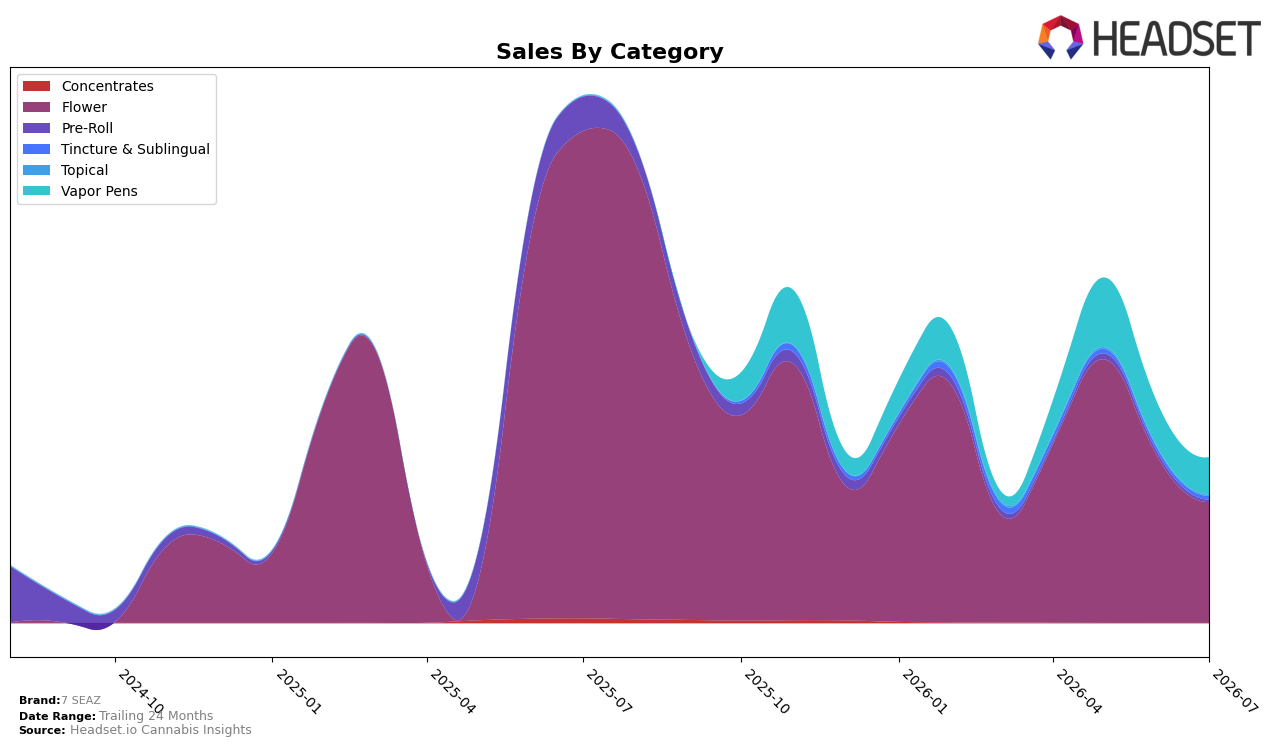

7 SEAZ’s mix in July 2026 tilted 73.65% toward Flower, where sales fell 75.27% year over year and 27.20% month over month, while Vapor Pens reached a 22.62% share with a 15.12% month-over-month decline and no year-over-year baseline. Pre-Roll compressed to 1.18% share with a 94.34% year-over-year drop and 50.08% month-over-month decline, as Tincture & Sublingual held 1.91% share with a 12.42% month-over-month slide and Topical remained niche at 0.64% share but rose 37.25% month over month from a small base. With the average price down 20.55% year over year to $49.41 and Flower average price at $69.89, the category skew concentrated exposure in the steepest-declining area, implying the brand’s overall 68.89% year-over-year sales contraction was driven primarily by a heavy Flower dependency and only partial cushioning from Vapor Pens.

Positionally, a 73.65% Flower weight combined with a rank of 50 in Flower in New York suggests limited shelf velocity where the brand leans most, while a 22.62% share in Vapor Pens creates a secondary foothold that is declining month over month by 15.12% and not yet offsetting core losses. The 37.25% month-over-month rise in Topical alongside a 50.08% month-over-month Pre-Roll drop indicates experimentation at the fringes without material scale impact, pointing to a near-term need to either de-risk the Flower mix or compress price/assortment gaps in Flower and Vapor Pens to stabilize rank and regain share.

Competitive Landscape

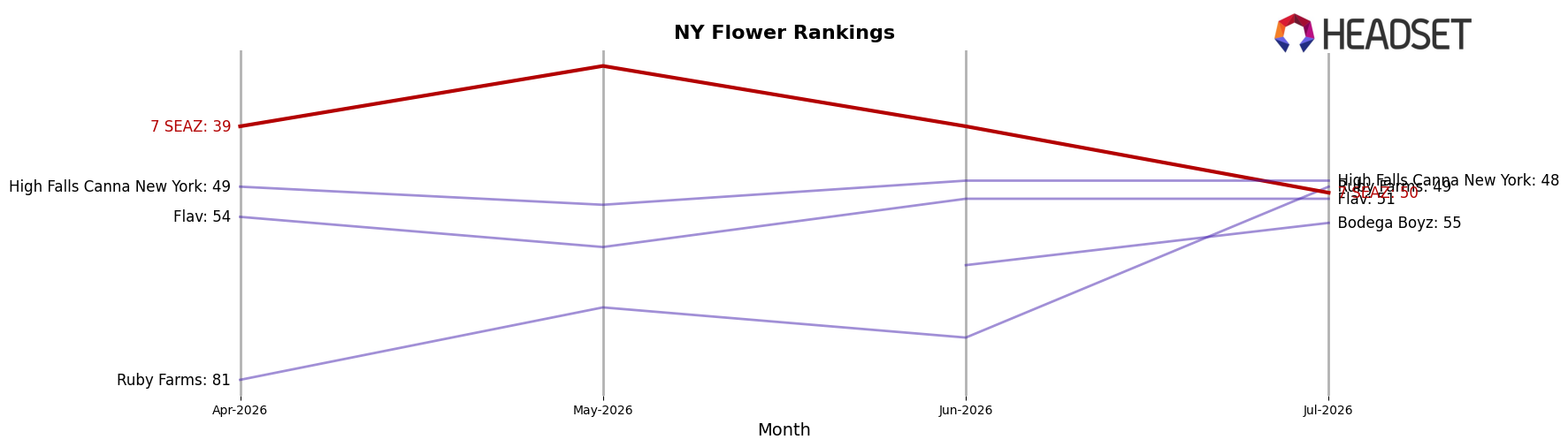

7 SEAZ sits at rank #50 in New York Flower in July 2026, down 34 positions year over year from #16, and down 11 positions since April 2026 when it was #39; in contrast, Find. held #1 in July 2026 after rising 8 places YoY while expanding sales by 46.7%, and Grassroots reached #5 with a 15-rank YoY climb alongside 79.8% sales growth, indicating that 7 SEAZ’s slide from its August 2025 peak at #16 to #50, combined with competitors’ upward rank shifts and double-digit growth rates, implies a repositioning is needed to regain share as the category concentrates toward faster-rising leaders.

Notable Products

Wave Rider - Miami Mimosa Distillate Disposable (1g) posted the steepest decline at -44.7% MoM and slid to rank 7, while Wave Rider - Bikini Diesel Distillate Disposable (1g) fell -20.7% to rank 2, implying volatility within the disposable lineup despite Wave Rider - California Citrus Distillate Disposable (1g) holding rank 1 with a +41.6% lift. Three Vapor Pens SKUs sit in the top eight and five Vapor Pens appear in the top ten, yet two of those top-eight pens dropped between -17.7% and -44.7%, signaling concentrated reliance on a format with uneven momentum. In contrast, Flower held steadier with Strawberry Cough (7g) up +15.4% at rank 3 and 24K Gold (7g) down -21.7% at rank 9, alongside Holy Grail Kush x Hibachi Supreme (14g) entering the top ten with $20,825 in July 2026. The mix points to 7 SEAZ leaning into Vapor Pens for headline velocity but needing Flower’s steadier ranks to balance risk as disposable performance bifurcates.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.