Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Electraleaf is stocked at 194 licensed dispensaries across New York and Massachusetts, 184 of them in New York, with the deepest coverage in New York, Buffalo, Rochester, Queens, and Albany. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

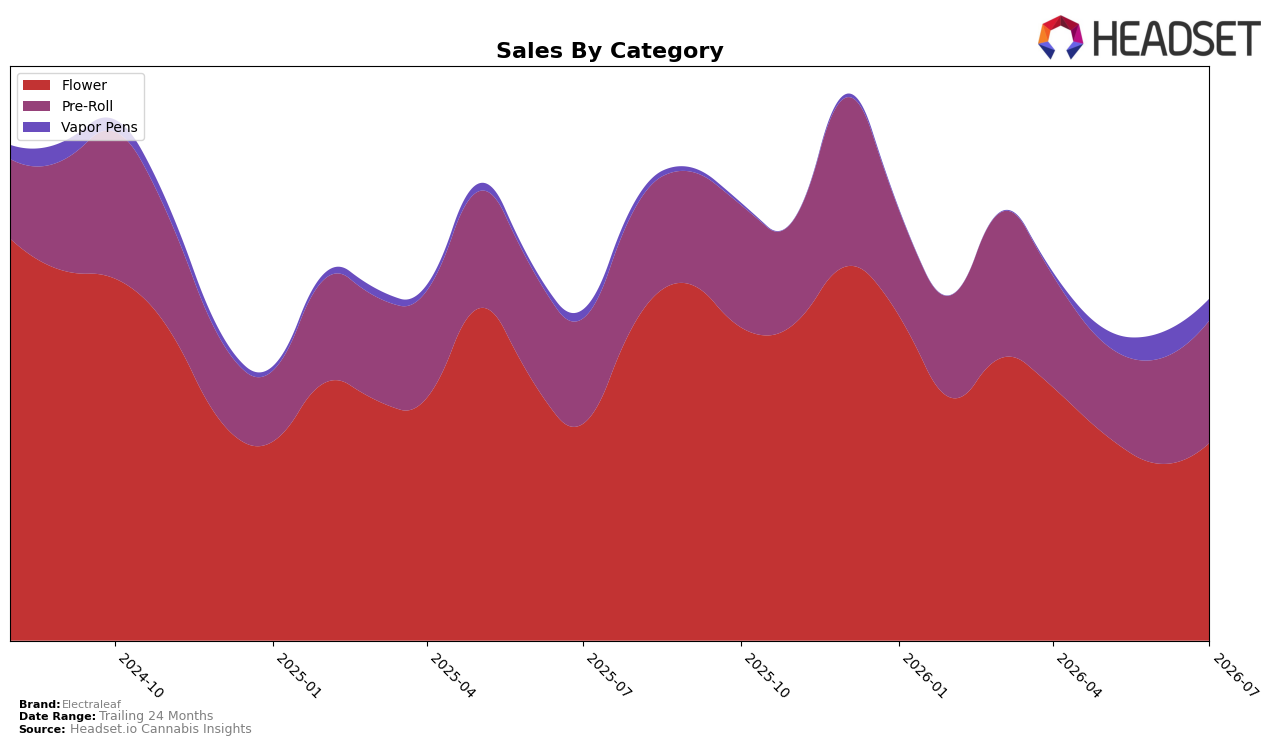

Electraleaf’s mix in July 2026 tilted toward Flower at 57.66% share, despite Flower sales falling 8.86% year over year and rising 11.60% month over month, while Pre-Roll climbed to 35.83% share with 16.28% YoY growth and 17.25% MoM growth. Vapor Pens remained a smaller 6.51% share, with a 135.48% YoY surge but a 13.84% MoM decline, and the brand’s average price fell 5.51% YoY as overall sales grew 3.26% YoY; taken together, this mix indicates the brand is leaning into faster-turning Pre-Rolls while buffering volatility in Vapor Pens and stabilizing Flower momentum.

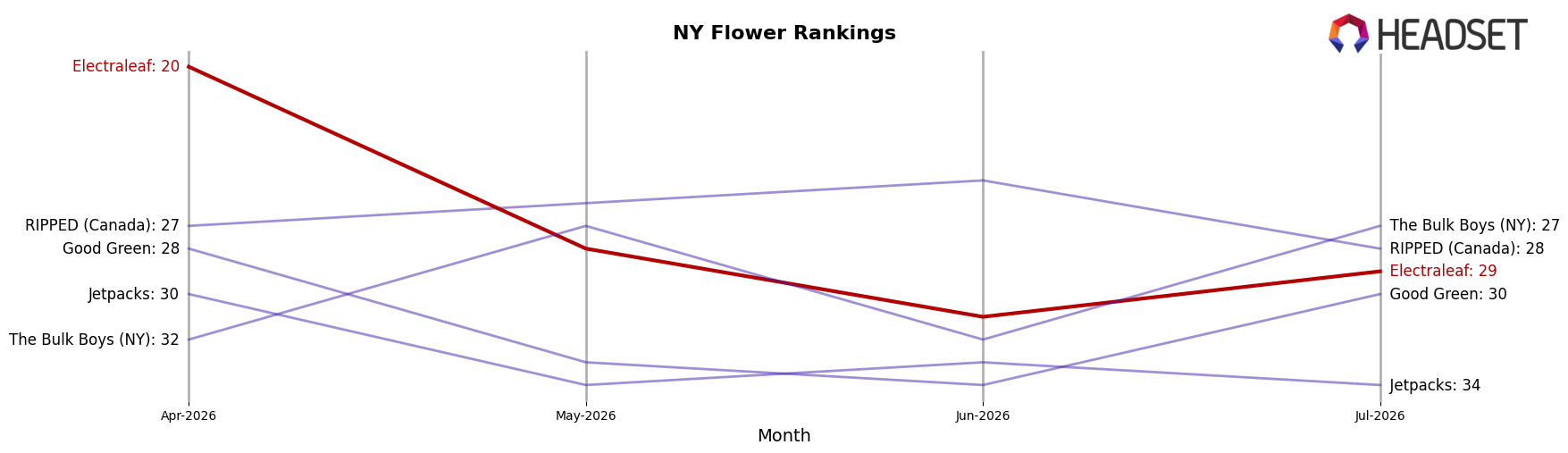

With a Flower rank of 29 in New York and Flower still the majority at 57.66% share, the 11.60% MoM gain in Flower paired with a 17.25% MoM rise in Pre-Roll implies near-term positioning built on accessible price points and multi-pack or value-led formats, consistent with the 5.51% YoY price decline. The 135.48% YoY lift but 13.84% MoM pullback in Vapor Pens suggests opportunistic rather than core positioning in that category, reinforcing a strategy where Pre-Roll expansion offsets Flower’s 8.86% YoY drag to keep total brand sales up 3.26% YoY while maintaining headroom to improve rank from 29 in Flower.

Competitive Landscape

Electraleaf sits at rank #29 in New York Flower for July 2026, down 8 positions year over year from #21, and 9 spots below its April–June 2026 three‑month mark of #20; against this slide, its historical peak of #6 in July 2024 sets a two‑year drop of 23 ranks that coincides with a category reshuffle where Find. advanced from #8 to #1 and Grassroots moved from #15 to #5 while posting a 79.8% YoY sales increase versus a 51.5% YoY sales decline for Dank. By Definition; the pattern implies Electraleaf’s trajectory is being outrun by faster risers at the top while also ceding ground to brands that are contracting less severely, pointing to a need to reenter the upper tiers before further rank erosion compounds.

Notable Products

Blue Dream Pre-Roll (1g) posted the standout movement in July 2026 with a +75% month-over-month surge, climbing to rank 2 while Han Solo Burger Pre-Roll (1g) fell -49% to rank 9, signaling a sharp split in Pre-Roll momentum. Four of the top ten are Pre-Roll SKUs, anchored by Purple Haze Pre-Roll (1g) at rank 1, even as Flower entries like Purple Haze (3.5g) dropped -40% to rank 7 and Blue Lobster (3.5g) slid -12% to rank 10. Wedding Cake (3.5g) declined -18% at rank 8 against the Pre-Roll gains, suggesting consumer spend is rotating toward ready-to-use formats despite some flagship Flower volume at $76,771. The pattern implies Electraleaf is consolidating around Pre-Roll-led velocity while legacy Flower SKUs retrench, pointing to pack-type convenience as the near-term commercial driver.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.