Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

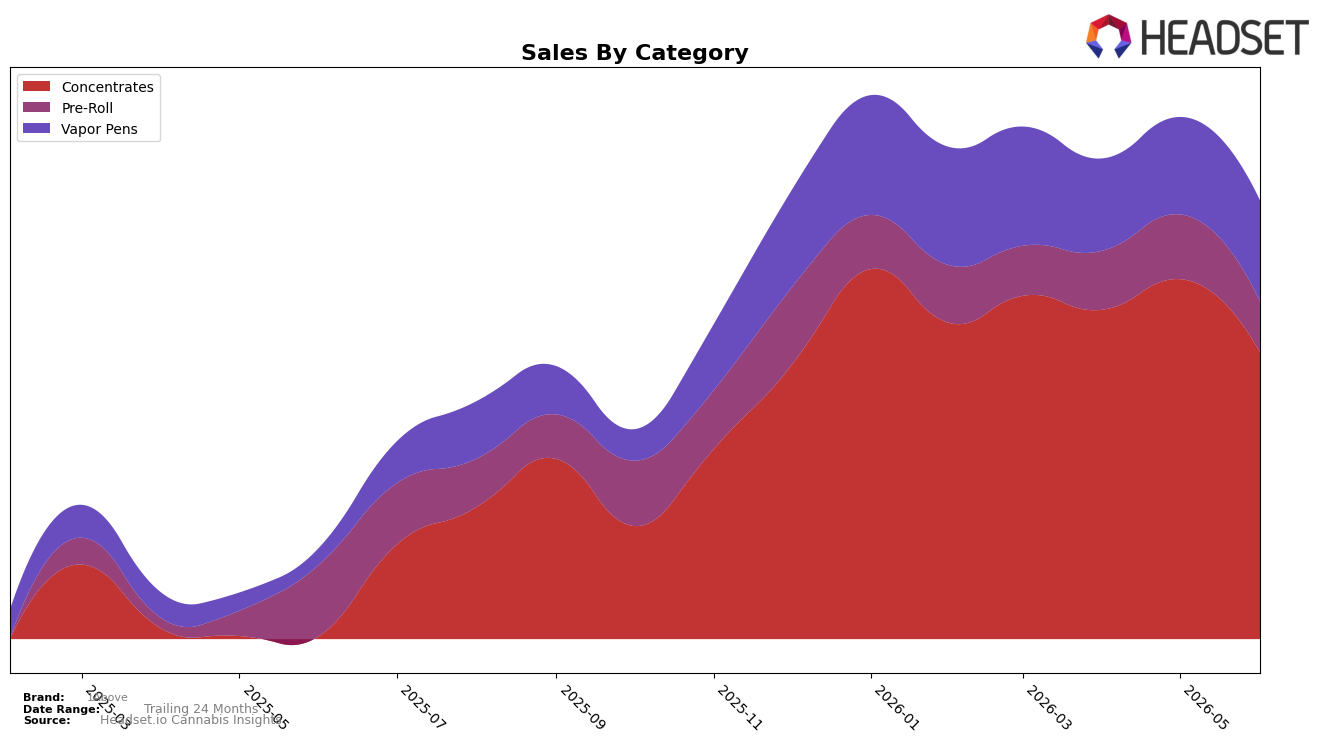

In June 2026, 1Above concentrated 65.44% of sales in Concentrates with a 10,244.13% year-over-year surge but a -20.34% month-over-month dip, while Vapor Pens held 22.98% share with 506.77% YoY growth and a 3.56% MoM uptick; Pre-Roll contracted to 11.59% share with -28.84% YoY and -21.17% MoM. The overall average price rose 34.16% YoY to $45.53 as Concentrates carried a higher $52.64 average, pointing to premium-mix inflation even as the largest category retrenched MoM. Together with a category rank of 15 in Concentrates in Ontario, the mix shift implies a scale anchored in Concentrates that is volatile month to month but revenue-accretive via higher pricing.

The juxtaposition of a -20.34% MoM decline in Concentrates against a 3.56% MoM gain in Vapor Pens suggests partial substitution toward a lower-priced format at $36.42, yet the 65.44% share concentration and 10,244.13% YoY lift keep the brand’s positioning tied to high-THC extracts rather than breadth across formats. With Pre-Roll contracting -28.84% YoY and losing -21.17% MoM to just 11.59% share, 1Above is narrowing its role in value-driven entry formats, effectively trading distribution breadth for depth in Concentrates where it sits at rank 15 in Ontario; this pattern implies pricing power anchored in Concentrates, but near-term growth sensitivity to monthly category swings until Vapor Pens scales beyond 25% share.

Competitive Landscape

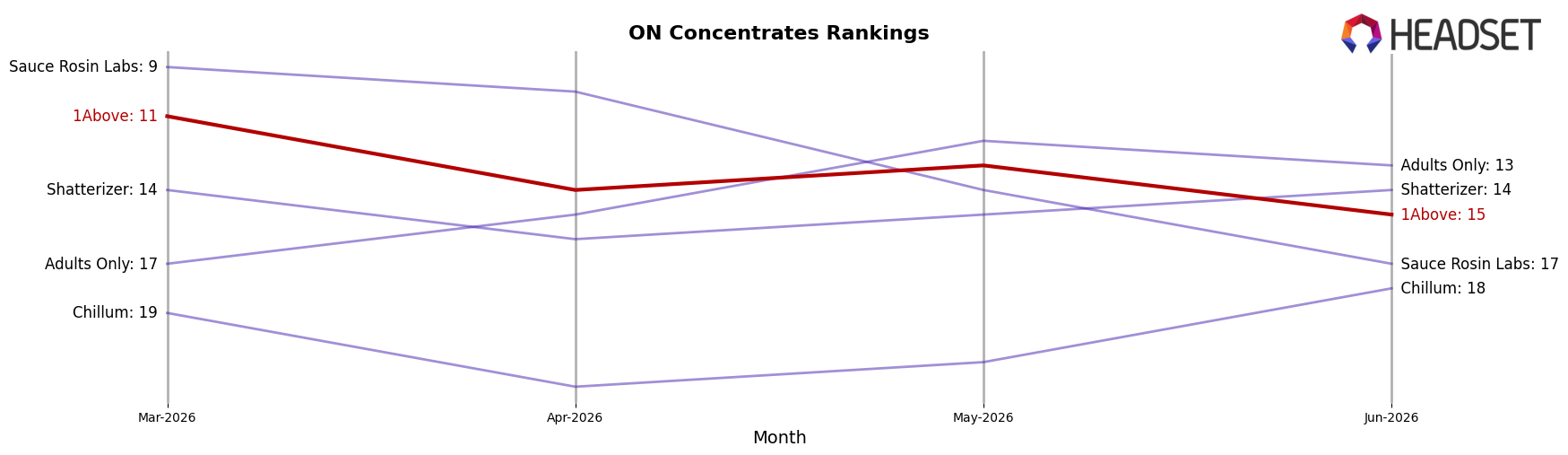

1Above is ranked #15 in ON Concentrates in June 2026, improving 74 positions year over year from #89, while sliding 4 spots from #11 three months ago; the brand’s peak was #10 in January 2026, placing its current rank 5 positions below that high. Against competitors, Vortex Cannabis Inc. held #1 with a -1.8% YoY sales change as 1Above advanced 74 ranks YoY, and Pura Vida climbed from #4 to #2 with 49.2% YoY sales growth while 1Above moved from #89 to #15; this spread suggests 1Above is gaining distribution or SKU relevancy faster than many peers even as leaders consolidate top slots. With Nugz (Canada) static near the top at #3 after a -6.6% YoY sales change and BoxHot rising from #8 to #4 on 44.1% YoY growth, 1Above’s YoY surge paired with a recent quarter slip implies momentum is rebalancing toward mid-tier consistency rather than a rapid return to January 2026 peak positioning.

Notable Products

Blue Zushi x Lemonberry Hash Hole Infused Pre-Roll 2-Pack (2g) plunged 79.7% month over month to rank 8, while Blockberry Rosin Disposable (0.5g) fell 60.8% to rank 7, indicating a sharp pullback in long-tail SKUs despite 73u Live Rosin (1g) holding rank 1 with a 18.0% decline. Two Pre-Roll SKUs sat in the top ten and both declined at least 10.4% while Vapor Pens split with a 5.8% gain for Hybrid Juice Bar Rosin Disposable (0.5g) at rank 2 versus a 60.8% slide for Blockberry, suggesting format volatility concentrated in Pre-Rolls and lower-ranked pens. Concentrates were mixed, with Zoap 73u Live Rosin (1g) down 40.8% at rank 5 contrasted by Lemonberry 73u Live Rosin (1g) up 38.8% at rank 6, pointing to strain-level substitution more than category weakness. Overall, the product mix implies 1Above is increasingly anchored by a few tiered Concentrates and one leading Vapor Pen, steering assortment toward fewer SKUs with consistent repeat rather than breadth-heavy pushes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.