Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

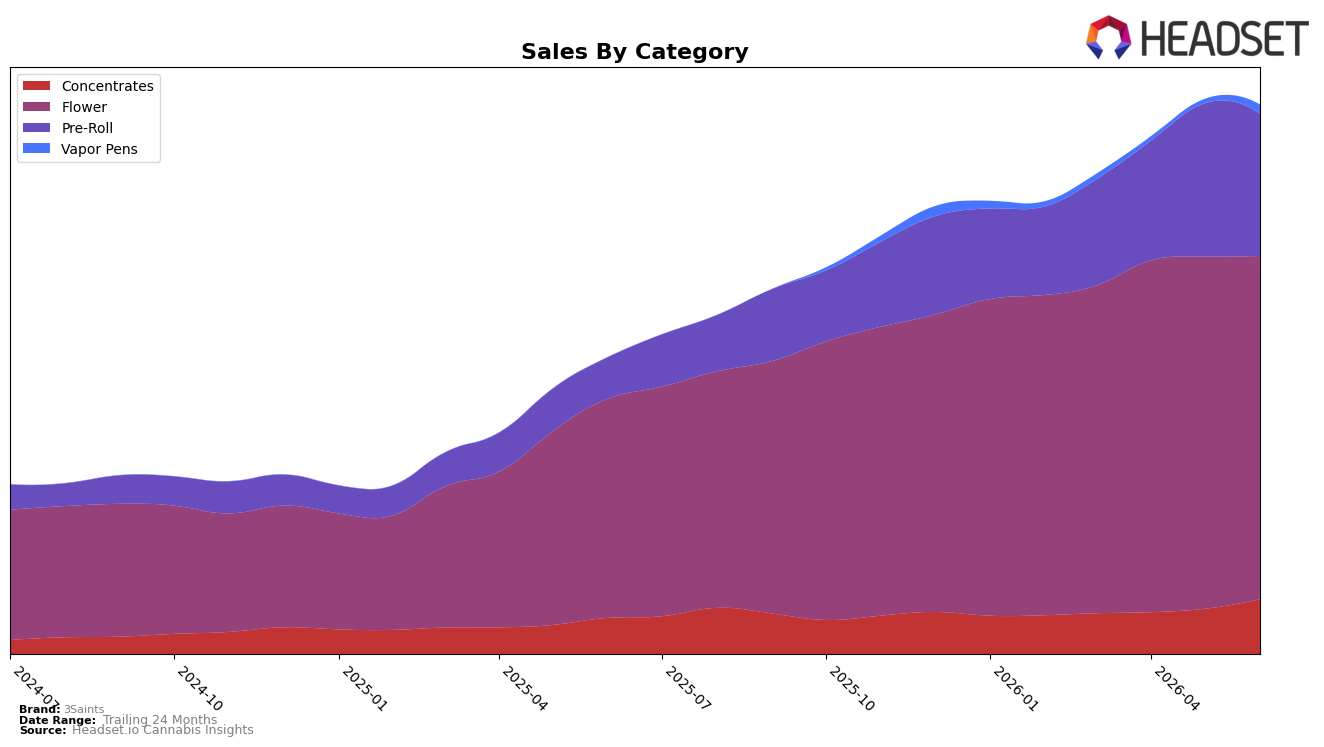

In June 2026, 3Saints concentrated 62.52% of sales in Flower with year-over-year growth of 56.52% but a month-over-month decline of 2.54%, while Pre-Roll held 25.87% share with a 244.19% year-over-year surge and a 7.30% month-over-month pullback. Concentrates reached 9.95% share with 52.24% year-over-year growth and a 21.34% month-over-month increase, and Vapor Pens, though only 1.66% share, jumped 120.87% month-over-month without a year-over-year baseline. With overall brand sales up 85.19% year-over-year and average price up 23.50%, the mix implies a pivot from Flower’s historical dominance toward higher-velocity Pre-Roll and a nascent push in Vapor Pens, while Concentrates acts as a stabilizer on recent momentum.

The category shifts suggest 3Saints is trading some depth in Flower for reach across faster-turn formats, given Pre-Roll’s 244.19% year-over-year growth despite a 7.30% month-over-month dip and Vapor Pens’ 120.87% month-over-month spike from a 1.66% base. Holding a Flower rank of 6 in Alberta while Pre-Roll and Vapor Pens build from smaller shares positions the brand as a Flower-led player diversifying into convenience-led segments; this balance should protect against single-category volatility evidenced by Flower’s 2.54% and Pre-Roll’s 7.30% month-over-month declines.

Competitive Landscape

3Saints sits at rank #8 in ON Flower for June 2026, up four positions from #12 year over year and down one spot from a peak at #7 in May 2026; the one-month slip from #7 to #8 contrasts with a 4-rank YoY climb that narrows distance to leaders. Meanwhile, Spinach advanced from #4 to #1 while growing sales 38.3% YoY, and Back Forty / Back 40 Cannabis fell from #1 to #4 with a 11.3% YoY sales decline, indicating that 3Saints’ move from #12 to #8 positions it to benefit when incumbents rotate but its dip from #7 to #8 in June 2026 signals that sustained share gains will require converting spring momentum into stability against faster-rising leaders.

Notable Products

Blueberry Muffinz Pre-Roll 4-Pack (2g) posted the steepest decline in June 2026 at -16.27% while sliding to rank 6, and Strawberry Cheezequake Pre-Roll 4-Pack (2g) fell -10.73% at rank 3, together signaling softening multi-pack Pre-Roll momentum. In contrast, Black Afghan Hash (2g) rose +23.29% to rank 4 as Kush Cookies (14g) in Flower gained +5.91% at rank 8, while flagship Kush Cookies (3.5g) dipped -7.32% but held rank 1. With five of the top ten positioned in Pre-Roll and most of those posting -3% to -16% MoM, the category mix tilts toward volume SKUs whose monthly volatility can compress rank stability. The pattern implies 3Saints is leaning on Flower and Concentrates to offset Pre-Roll softness, nudging the commercial focus toward fewer, higher-yield formats rather than breadth across Pre-Roll packs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.