Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Achieve is stocked at 11 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Sun City, Apache Junction, El Mirage, and Flagstaff. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

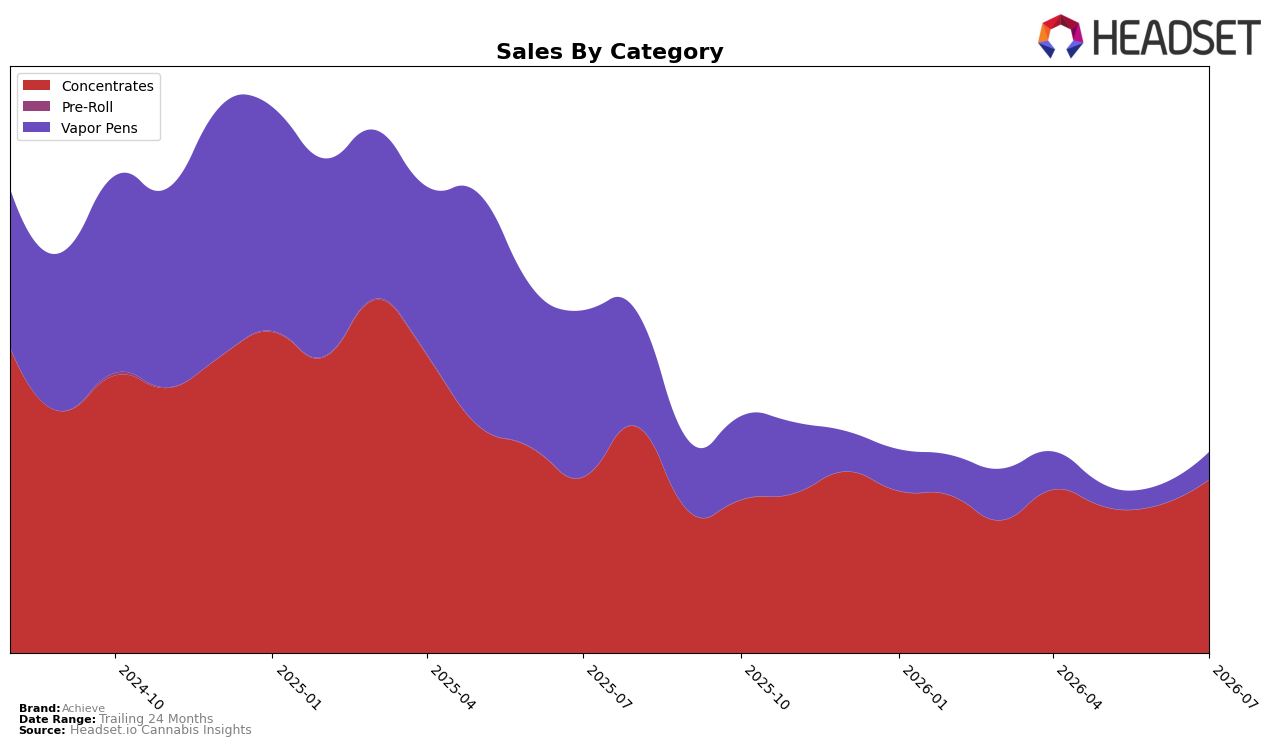

Concentrates carried 86.34% share in July 2026 while Vapor Pens held 13.66%, with Concentrates up 17.54% MoM but down 1.48% YoY and Vapor Pens up 39.92% MoM but down 83.57% YoY; this mix coincided with an overall brand sales decline of 41.47% YoY. Average price fell 25.51% YoY to $21.21, with Concentrates pricing at 19.62 and Vapor Pens at 43.66, while Achieve’s Concentrates rank sat at 18 in Arizona; the pattern implies Achieve is leaning into lower-priced Concentrates for volume recovery while nursing a severely compressed Vapor Pens base.

The MoM lift in both categories (+17.54% for Concentrates and +39.92% for Vapor Pens) alongside deep YoY contraction (−1.48% and −83.57%, respectively) suggests short-cycle promotions or price resets are moving units without repairing the longer-cycle demand gap, and the 86.34% Concentrates weighting concentrates risk into a single category. Holding rank 18 in Arizona for Concentrates while total brand sales are down 41.47% YoY indicates Achieve’s positioning is anchored to value-driven Concentrates rather than premium Vapor Pens at 13.66% share, implying near-term stability depends on sustaining sub-$20 pricing even as it constrains premium mix expansion.

Competitive Landscape

Achieve sits at rank #18 in July 2026 in AZ Concentrates, down 2 positions year over year from #16 and up 1 position versus 3 months ago at #19, indicating a mild rebound after a longer drift from its peak at #10 in March 2025. In contrast, Canamo climbed from #2 to #1 while growing sales 14.9% year over year, and Mohave Cannabis Co. slipped from #1 to #2 with a 15.1% year-over-year sales decline, while Grow Sciences advanced from #6 to #3 on 61.5% growth; this mix of upward and downward competitor mobility alongside Achieve’s -2 rank delta implies Achieve is losing relative momentum at the top of the table but stabilizing in the mid-tier, pointing to share defense rather than category leadership in the near term.

Notable Products

Ronny Burger RSO (1g) posted the largest month-over-month gain at 190.6% and climbed into rank 3, while Slappy Gilmore Hash (1g) rose 118.0% to rank 1, indicating demand is swinging toward both RSO and hash formats. Tropicana Cherry Hash (1g) fell 70.7% and sits at rank 5, and Blue Dream Live Resin Sauce (1g) declined 20.4% to rank 8, creating a bifurcation where winners expanded triple digits as laggards contracted double digits. With five of the top ten in Concentrates and three in Vapor Pens, the mix tilts toward extract-led offerings, implying Achieve is concentrating assortment and marketing on high-velocity concentrate SKUs while letting underperforming flavors cycle down.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.