Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Abundant Organics is stocked at 31 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Mesa, Tucson, Chandler, and Tempe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

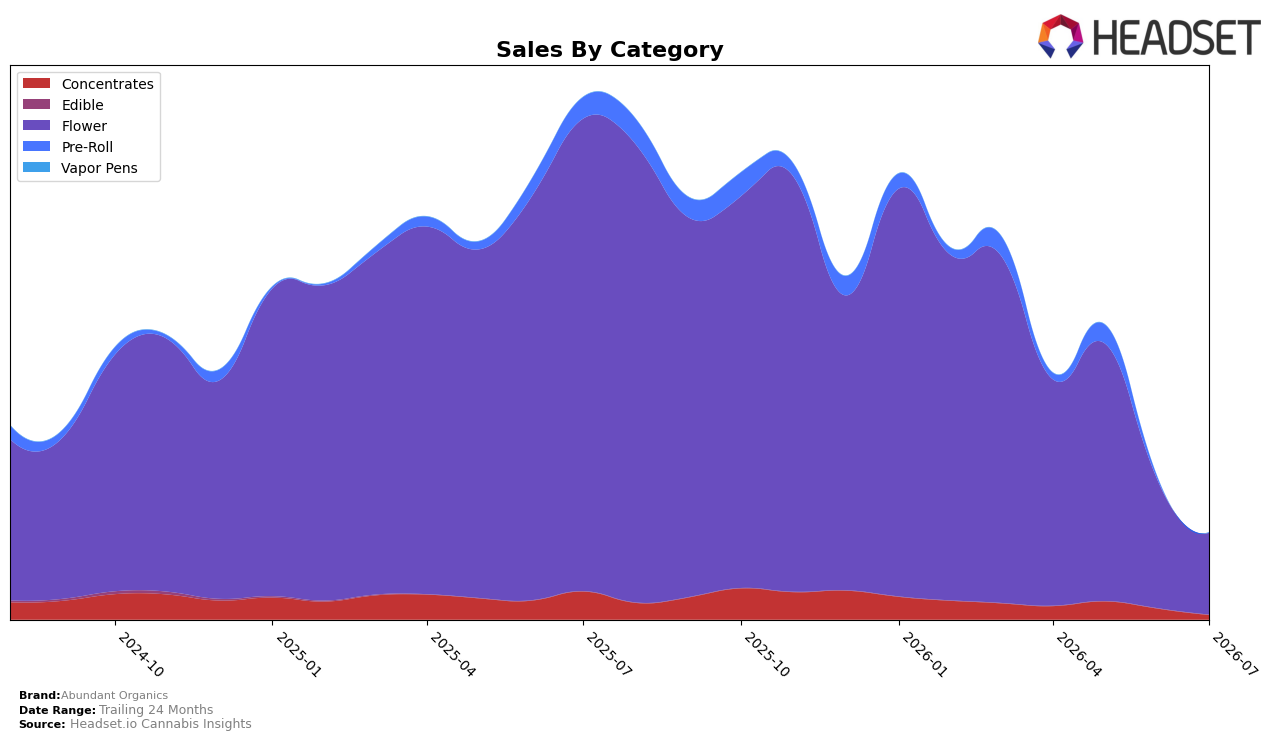

Abundant Organics concentrated 94.96% of July 2026 sales in Flower, with Concentrates at 5.03% and Pre-Roll at 0.02%; within this mix, year-over-year declines were -82.79% for Flower and -84.49% for Concentrates, while month-over-month shifts were -36.25% for Flower and -59.72% for Concentrates, indicating contraction across core lines. The brand’s average price rose 29.41% year over year to $36.90, and Flower’s average price sat at $37.08 versus $34.00 in Concentrates, suggesting a premium skew even as the brand’s overall sales fell -83.58% year over year; this pattern implies volume loss concentrated in Flower is driving most of the downturn while price increases partially offset unit declines.

With Flower ranking 37th in Arizona and holding 94.96% category share of the brand’s mix, the -36.25% month-over-month pullback in Flower paired with a -59.72% month-over-month drop in Concentrates signals narrowing breadth that raises exposure to single-category volatility. The -99.93% year-over-year collapse in Pre-Roll share to 0.02% alongside a 29.41% year-over-year price lift indicates a trade-up strategy or reduced promotional intensity that is not converting to sustained rank gains, implying Abundant Organics is positioned as a higher-priced Flower-first player whose short-term resilience depends on stabilizing Flower velocities in Arizona rather than rebuilding peripheral categories immediately.

Competitive Landscape

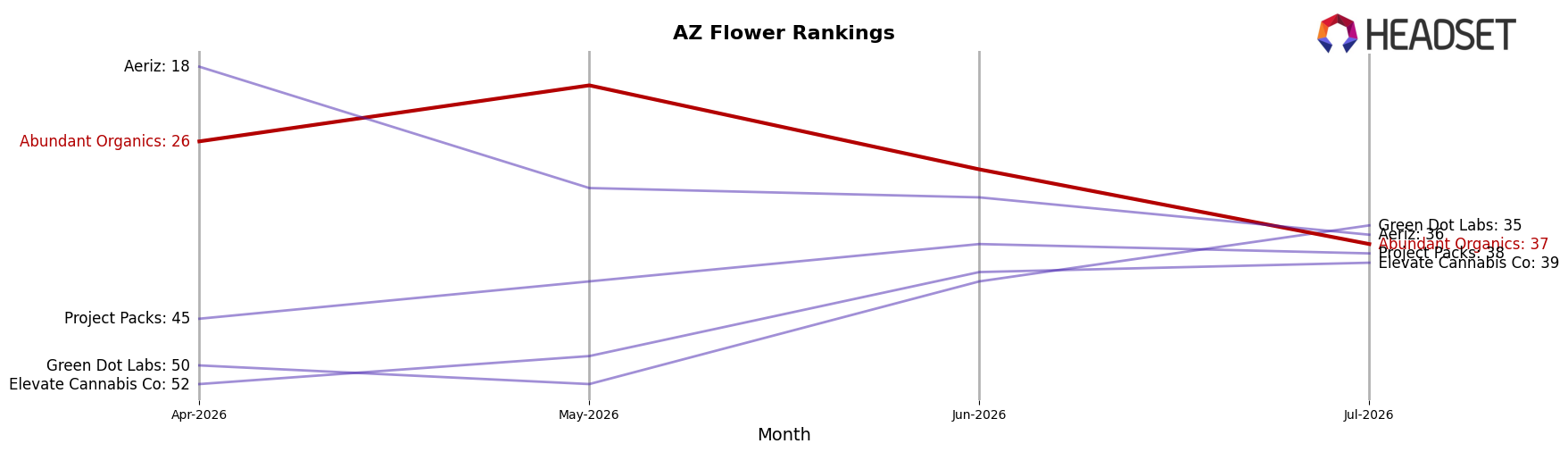

Abundant Organics sits at rank #37 in AZ Flower in July 2026, down 29 positions from its January 2026 peak at #8 and 11 spots lower than its April 2026 position at #26, signaling a steep descent from a prior top-10 foothold; meanwhile, Just Flower climbed to #1 with a 21.8% year-over-year sales increase and Brown Bag reached #4 alongside a 79.0% YoY gain, while Fenix slipped to #5 with a -6.9% YoY change, indicating that Abundant Organics’ rank erosion aligns more with underperformance relative to faster-advancing rivals than with a broad market contraction; the trajectory implies the brand must counter accelerating share consolidation at the top or risk further displacement as competitors extend their lead.

Notable Products

Viennetta (3.5g) led the movement in July 2026 with a -22.6% month-over-month decline while sliding to rank 3, indicating a pullback even as Jenny Le Pew (Bulk) held rank 1 and Sugar Puss (14g) sat at rank 2. With all top-10 items in Flower and two SKUs tied at rank 9, the rank concentration suggests assortment breadth but thin differentiation at the middle, further underscored by a single SKU at rank 4 not offsetting the -22.6% drop at rank 3. The $22,958 posted by Sugar Puss (14g) at rank 2 alongside the -22.6% for Viennetta (3.5g) implies the mix is leaning into heavier-weight Flower formats while smaller pack sizes are ceding momentum. Net effect: Abundant Organics is consolidating around Flower dominance with volume-weighted SKUs, signaling near-term focus on fewer, higher-throughput strains rather than broad experimentation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.