Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Atta is stocked at 29 licensed dispensaries across Missouri, with the deepest coverage in St. Louis, Cassville, Des Peres, Kansas City, and Lee's Summit. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

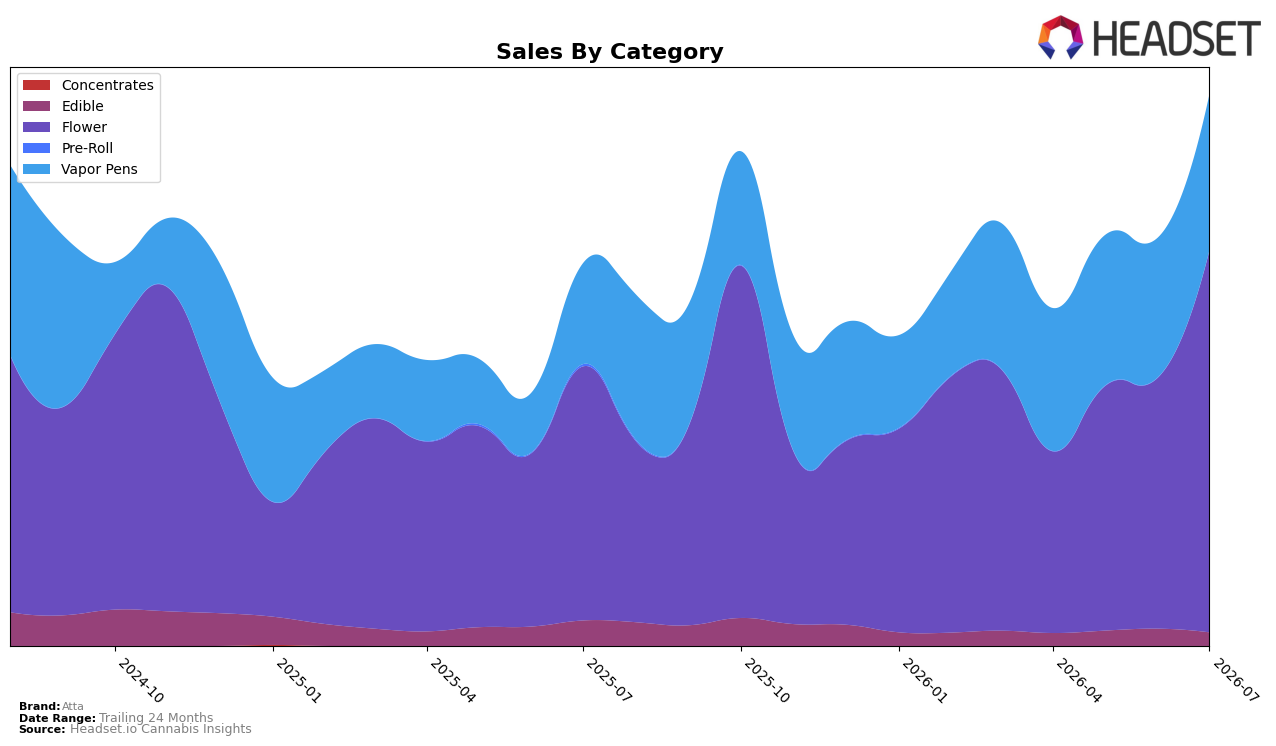

In July 2026, Atta’s category mix tilted further toward Flower, which held 69.31% share with year-over-year growth of 50.31% and month-over-month growth of 52.12%, while Vapor Pens accounted for 28.29% share with 54.55% YoY and 11.67% MoM growth; Edible shrank to 2.40% share with -47.38% YoY and -21.75% MoM. Average price lifted 24.28% YoY to $35.26 as Flower’s average price sat at $42.06, indicating premiumization concurrent with a 44.25% YoY brand sales lift; the pattern implies mix-led growth concentrated in higher-priced Flower while Edible de-prioritization reduces diversification risk coverage.

With Atta ranked 16 in Flower in Missouri and Flower’s share at 69.31% alongside a 52.12% MoM surge, the brand’s volume and visibility are increasingly tied to a single category; Vapor Pens’ 28.29% share with 11.67% MoM growth provides a secondary pillar, but the -47.38% YoY in Edible signals retreat from a low-price segment. The combination of a 24.28% YoY average price increase and a 54.55% YoY upswing in Vapor Pens suggests pricing power anchored in inhalables, implying a positioning shift toward higher-value inhalable dominance rather than a broad multi-format footprint.

Competitive Landscape

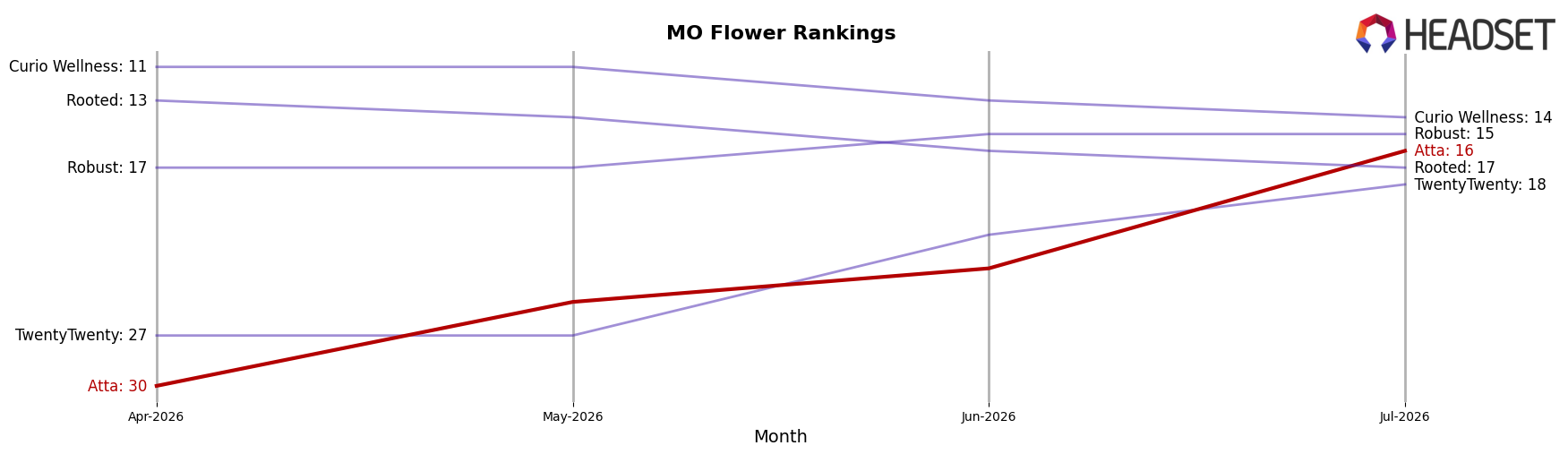

Atta ranks #16 in MO Flower in July 2026, improving 5 positions from #21 year over year, and rising 14 spots from #30 in April 2026, while matching its peak rank of #16 in July 2026; in contrast, Sinse Cannabis moved from #4 to #2 with an 8.99% YoY sales gain and Illicit / Illicit Gardens held at #3 despite a -12.78% YoY change, as Flora Farms stayed #1 with a -1.25% YoY shift and Local Cannabis Co. advanced from #10 to #5 on 41.83% YoY growth; this pattern implies Atta’s upward rank trajectory is driven more by mid-tier share churn than category-wide expansion, signaling a window to consolidate gains before faster climbers compress the middle ranks.

Notable Products

Super Snocone Distillate Cartridge (1g) posted the steepest decline at -33.5% MoM while dropping to rank 3, whereas Mango Tango Triple Pass Distillate Cartridge (1g) surged +51.2% MoM to rank 2 with $31,564 in July 2026, indicating a sharp reallocation of demand within the lineup. Badass Blueberry Distillate Cartridge (1g) grew +37.1% MoM to hold rank 1, and Bruce Banner Triple Pass Distillate Cartridge (1g) fell -11.3% MoM to rank 7, with Pineapple Swing Distillate Cartridge (1g) also sliding -10.7% MoM to rank 8. Eight of the top ten are Vapor Pens SKUs, concentrating category exposure at 80% of the leaderboard and amplifying volatility risk as gains above +50% and declines below -10% coexist in July 2026. Taken together, the mix points to Atta leaning into a volatile Vapor Pens core where rapid winners are offsetting sharp laggards, implying a strategy centered on flavor rotation and rapid refresh over stable, long-cycle SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.