Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Autumn Brands is stocked at 240 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, San Francisco, West Hollywood, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

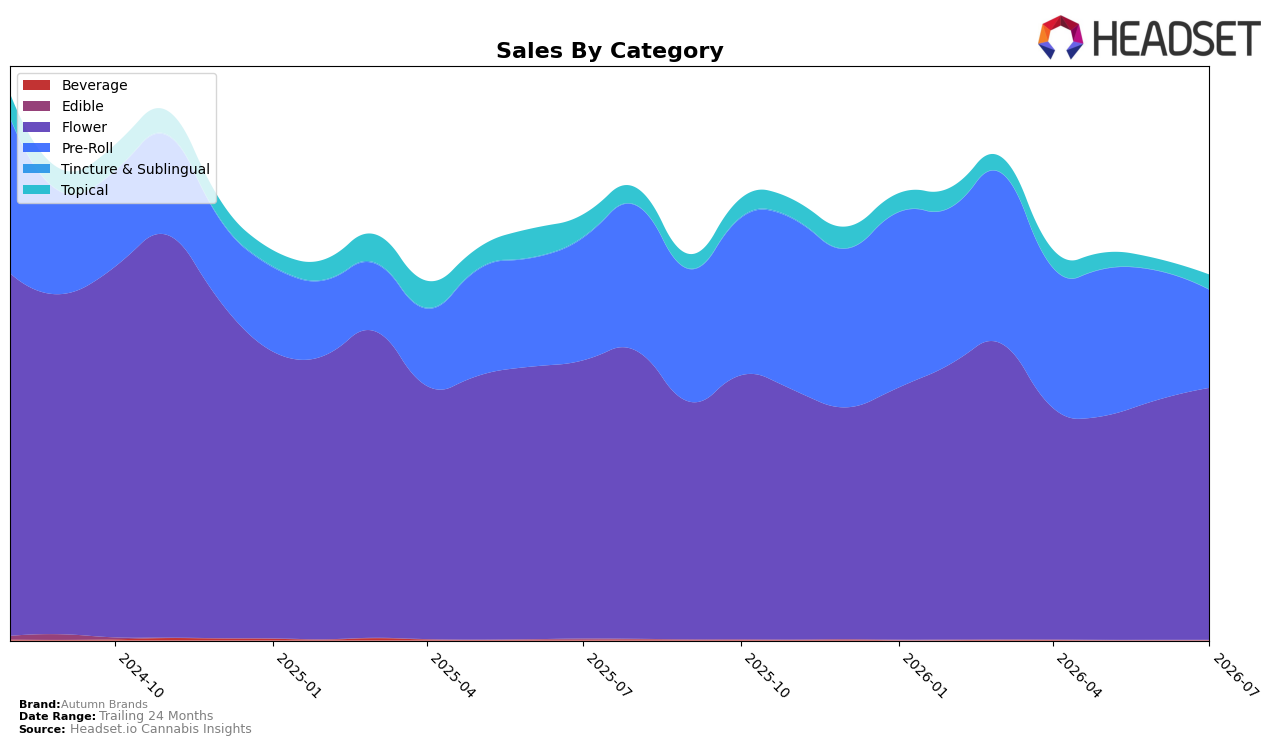

Autumn Brands concentrated 69.17% of July 2026 sales in Flower with a month-over-month gain of 4.98% but a year-over-year decline of 9.44%, while Pre-Roll held 26.83% share with a steep 24.04% month-over-month drop and a 20.07% year-over-year decline; Topical remained a 3.999% niche yet jumped 28.46% month-over-month despite a 34.09% year-over-year contraction. Average price fell 2.39% year-over-year to $19.58, and in Flower specifically the brand sat at rank 69 in California, implying a portfolio leaning on a single category where near-term momentum is offset by longer-cycle erosion.

The shift—Flower stabilizing month-over-month at +4.98% as Pre-Roll retrenches by 24.04% and Topical spikes 28.46% off a small base—implies Autumn Brands is consolidating around its core while trimming or losing velocity in a secondary format that once carried over a quarter of sales. With overall brand sales down 14.21% year-over-year and a 26.94% two-year slide, the current mix suggests a need to convert Flower’s incremental July 2026 gains into sustained rank improvement from position 69 in California and to either reposition Pre-Roll or pivot share toward higher-margin niches like Topical without sacrificing the 69.17% Flower anchor.

Competitive Landscape

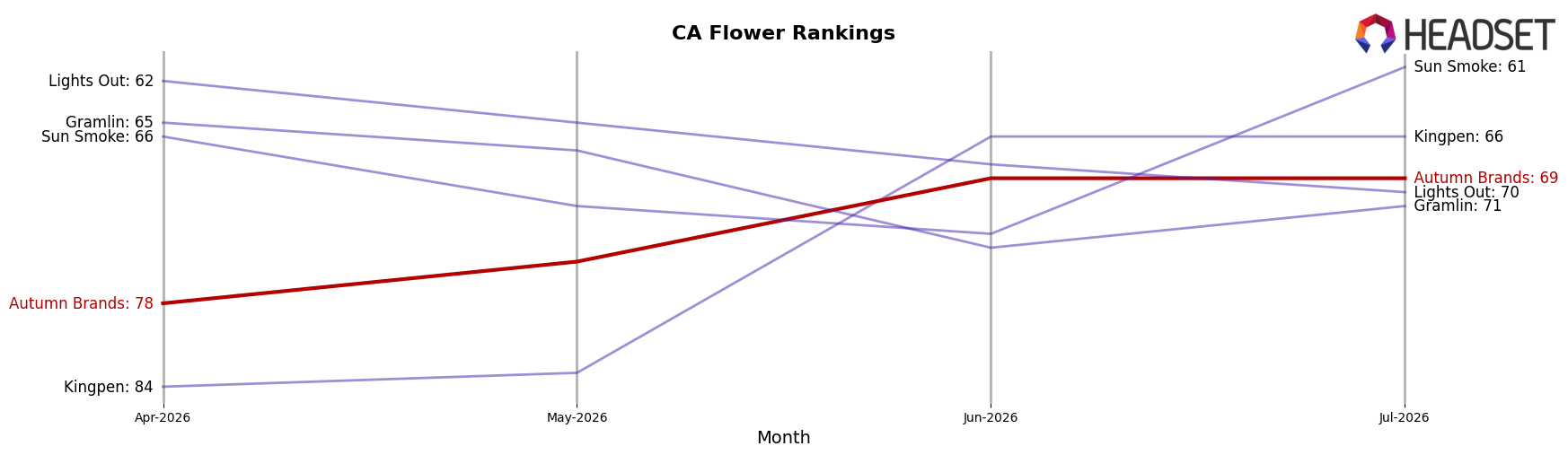

Autumn Brands sits at rank 69 in California Flower in July 2026, down 2 positions from rank 67 year over year, but up 9 positions versus its April 2026 mark at rank 78; against its peak at rank 59 in February 2026, the current standing is 10 places lower. While STIIIZY advanced from rank 2 to rank 1 with 59.7% year-over-year sales growth and CAM climbed from rank 4 to rank 3 with 52.2% growth, Autumn Brands’ 2-position YoY slippage alongside a 9-position recovery since April 2026 indicates mid-pack churn where short-term gains are possible but sustained share reclamation back toward the February 2026 peak requires outpacing faster-rising leaders.

Notable Products

Purple Carbonite Pre-Roll (1g) posted the steepest decline at -44.2% and slid to rank 4, while Cooked Pre-Roll (1g) fell -11.8% to rank 2, signaling a shakeout within top-tier pre-rolls. In contrast, Purple Carbonite (7g) jumped +34.8% to rank 5 and Blue Dream (3.5g) rose +18.3% to rank 6, and four of the top ten are Pre-Roll SKUs even as the category splits between gains of +27.8% and losses near -12.6%. Motion Party Pre-Roll (1g) climbed +24.7% to rank 1 and Mango Haze Pre-Roll (1g) advanced +27.8% to rank 3, yet Main Squeeze Pre-Roll (1g) dropped -12.6% to rank 8, indicating volatility concentrated within format rather than brand-level demand. The pattern implies Autumn Brands is tilting toward larger-pack Flower strength anchored by Purple Carbonite (7g) while rationalizing a crowded pre-roll lineup.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.