Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Greenline (CA) is stocked at 269 licensed dispensaries across California, New York, and Massachusetts, 266 of them in California, with the deepest coverage in Los Angeles, Santa Rosa, San Jose, San Diego, and Sacramento. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

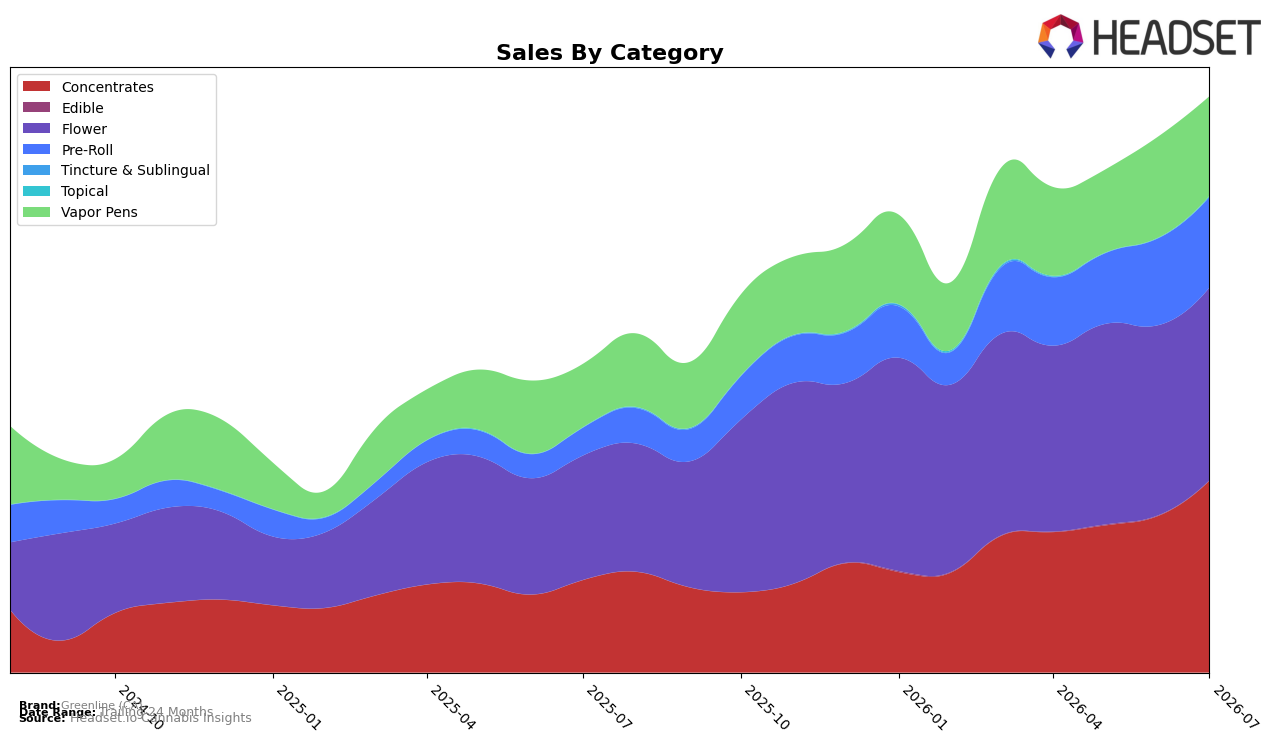

Greenline (CA) concentrated its July 2026 mix in Flower at 33.49% share and Concentrates at 33.33% share, with Pre-Roll at 15.72% and Vapor Pens at 17.28%, while Topical and Edible together contributed 0.18%. Year over year, Pre-Roll expanded 226.88% and Concentrates rose 107.53%, whereas Vapor Pens grew 57.50% and Flower advanced 55.03%; month over month, Concentrates climbed 22.55% and Pre-Roll increased 4.28% while Vapor Pens slipped 1.46% and Flower edged up 1.39%. The average price fell 5.62% year over year to $13.89, alongside brand sales growth of 86.997%, implying that volume gains are outpacing price declines as the mix tilts toward faster-growing segments. With a Flower rank of 55 in California, the balance of high-growth Concentrates and Pre-Roll against steadier Flower and Vapor Pens suggests the brand is leaning into momentum categories without abandoning the core.

The mix shift toward Concentrates and Pre-Roll—together 49.05% share—paired with 22.55% month-over-month growth in Concentrates and a 226.88% year-over-year surge in Pre-Roll indicates positioning around value-accessible inhalables, supported by a 5.62% price decrease that likely widened the addressable base. Vapor Pens’ 1.46% month-over-month decline against Flower’s 1.39% month-over-month uptick signals substitution within inhalables toward formats where the brand has stronger velocity, while Topical’s 213.35% month-over-month jump at just 0.13% share acts as a low-risk test rather than a strategic pillar. The pattern implies Greenline (CA) is using price to accelerate penetration in fast-turn categories while maintaining Flower scale to anchor visibility, a combination that can lift rank from 55 in Flower only if conversion in Concentrates and Pre-Roll sustains above the 107.53% and 226.88% year-over-year pace, respectively.

Competitive Landscape

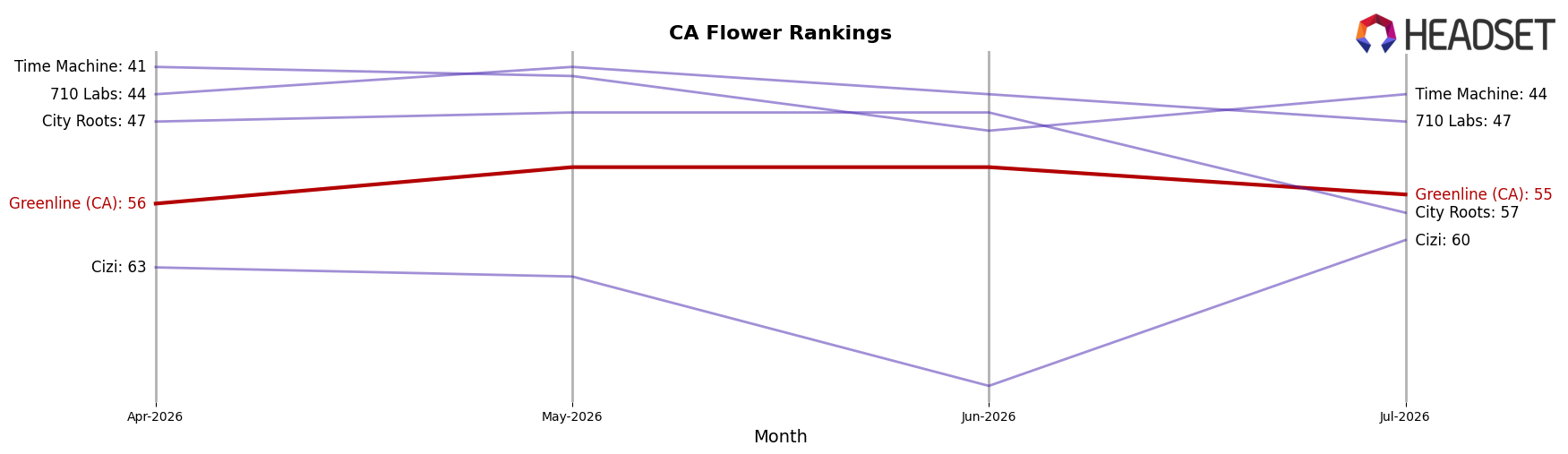

Greenline (CA) sits at rank #55 in California Flower for July 2026, improving 23 positions from #78 year over year and edging up 1 spot from #56 in April 2026; despite peaking at #51 in January 2026, the brand remains 4 ranks below that high. In contrast, STIIIZY climbed from #2 to #1 while growing sales 59.7% year over year, and CAM moved from #4 to #3 with 52.2% YoY growth, indicating top-tier velocity, whereas Claybourne Co. slipped from #3 to #5 with a –1.4% YoY decline; this dispersion suggests Greenline (CA)’s gradual rank gains are tied more to consistent but moderate momentum than to breakout share capture, implying the trajectory points to steady mid-pack positioning unless conversion accelerates.

Notable Products

Orange Tree (3.5g) posted the steepest decline in July 2026, down 11.3% month over month and sliding to rank 3, while Orange Tree Pre-Roll (1g) rose 11.3% MoM to rank 1, signaling a shift in demand from flower to ready-to-use formats. Three of the top ten are Pre-Roll SKUs, with Orange Tree Pre-Roll (1g) at rank 1 and Blueberry Sugar Pre-Roll (1g) at rank 6, compared with two Flower SKUs including Hash Burger (3.5g) at rank 9, indicating mix tilting toward value-per-draw over bulk flower. Vapor Pens hold two top-10 spots with Grand Daddy Purple Distillate Sauce Cartridge (1g) at rank 4 and Maui Pineapple Distillate Cartridge (1g) at rank 7, while Concentrates occupy ranks 2, 8, and 10, concentrating spend in inhalables rather than edibles or topicals. The pattern implies Greenline (CA) is converging on inhalable convenience-led segments, with flagship flower losing share to Pre-Rolls and Cartridges that likely drive higher turn and promotion-friendly price points.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.