Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

MADE is stocked at 328 licensed dispensaries across California, Arizona, and New Jersey, 199 of them in California, with the deepest coverage in Los Angeles, Costa Mesa, San Diego, San Jose, and Long Beach. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

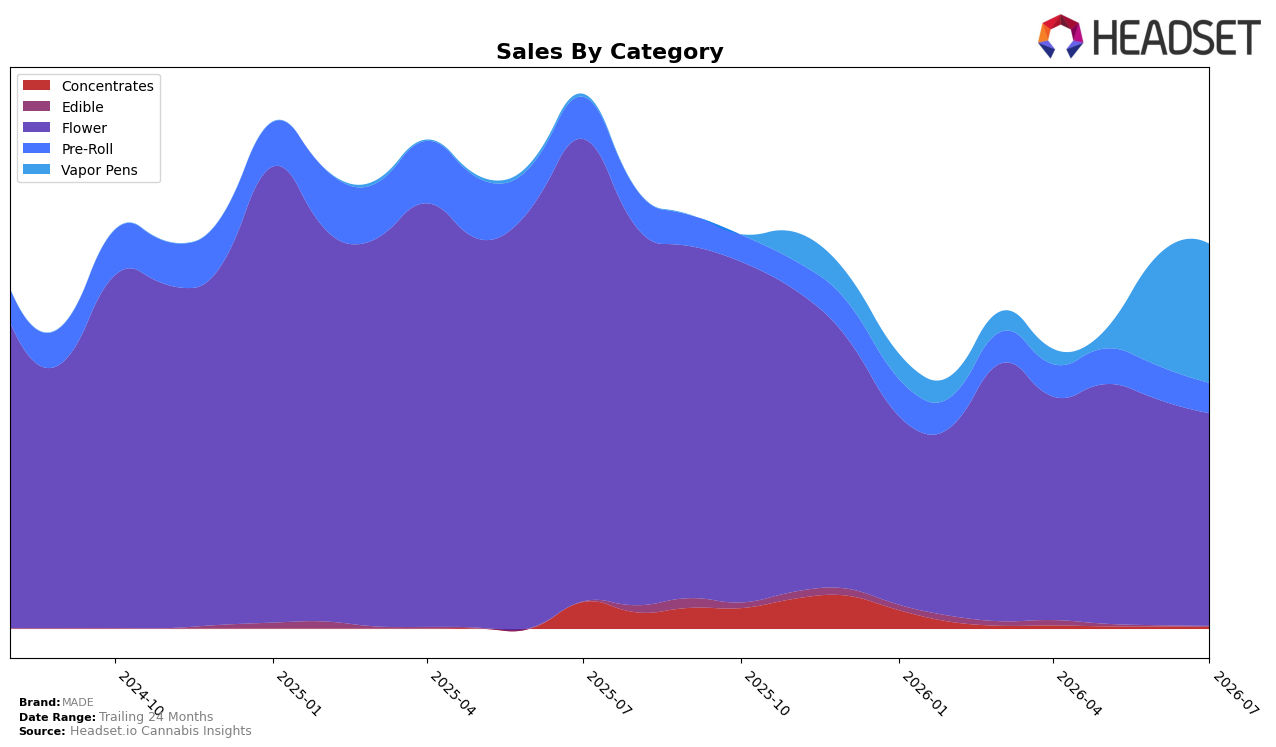

In July 2026, MADE’s mix pivoted toward Vapor Pens at 36.20% share with a 25.99% month-over-month increase and a 5,383.03% year-over-year surge, while Flower still led at 55.41% share but fell 5.83% month-over-month and 54.06% year-over-year. Pre-Roll slipped to 7.80% share with a 10.33% month-over-month decline and a 28.51% year-over-year drop, and Concentrates contracted to 0.48% share with a 12.63% month-over-month decline and 93.09% year-over-year erosion; Edible held 0.11% share with a 47.75% month-over-month pullback but 132.08% year-over-year growth. With an average price down 11.60% year over year to $25.92 and brand sales down 28.14% year over year despite 21.42% growth over 24 months, the pattern implies MADE is trading lower price for volume in faster-growing Vapor Pens while ceding legacy Flower volume.

The category shifts imply MADE is repositioning from a Flower-centric profile toward a dual-track anchored by Vapor Pens, where rapid year-over-year expansion of 5,383.03% contrasts with Flower’s 54.06% decline and Pre-Roll’s 28.51% decline. Given Flower’s 55.41% share but a rank of 27 in Flower within Arizona, the month-over-month -5.83% in Flower alongside +25.99% in Vapor Pens suggests short-term resource reallocation toward formats where price elasticity at an average price of $27.63 for Vapor Pens is more favorable than $30.08 in Flower. The implication is a deliberate migration toward higher-velocity, device-led formats to stabilize total share, even if near-term brand sales are down 28.14% year over year as the portfolio resets toward categories with better forward momentum.

Competitive Landscape

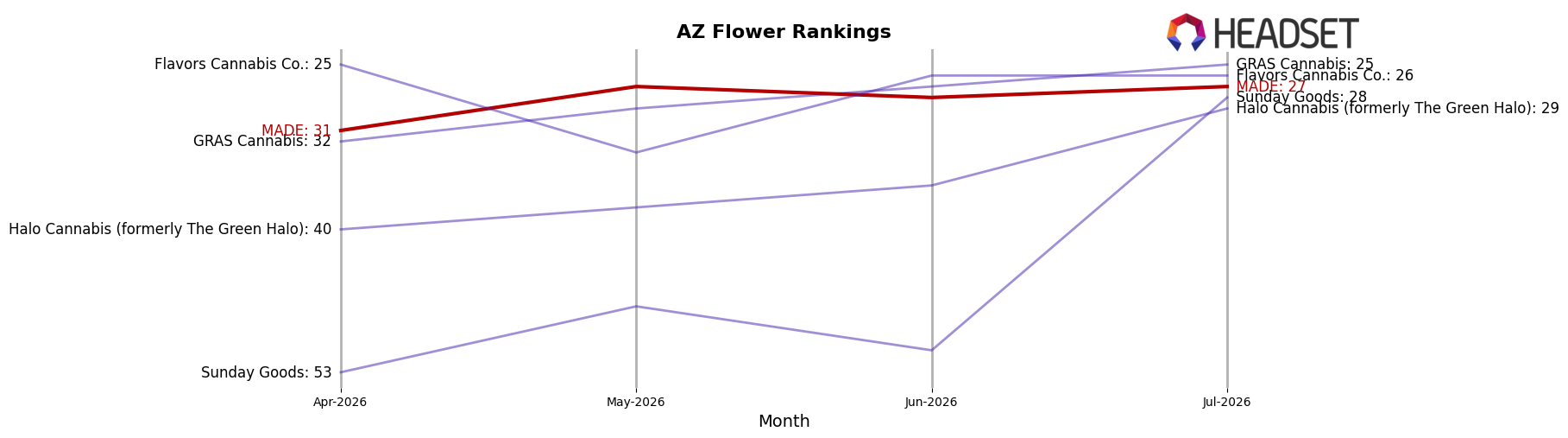

MADE sits at rank #27 in Arizona Flower for July 2026, down 2 positions year over year from #25, while improving 4 ranks versus April 2026’s #31; that trajectory contrasts with Just Flower holding #1 with a 21.8% year-over-year sales lift and Fenix sliding from #4 to #5 alongside a 6.9% sales decline. Against peers reshuffling at the top, Brown Bag advanced from #5 to #4 with 79.0% growth as MADE remains 9 ranks below its peak #18 from November 2025, indicating share is consolidating among faster movers and MADE’s recent 4-rank quarter-over-quarter rebound is not yet offsetting a 2-rank year-over-year erosion—implying stabilization rather than recovery unless momentum accelerates.

Notable Products

Lou Lou Lemon (3.5g) set the tone in July 2026 with a -14.23% month-over-month drop while holding rank 4, and Made x GS - Rainbow Melts Live Resin Disposable (1g) slid -11.11% at rank 2, indicating vapor-led softness at the very top. Offsetting that drag, Biscotti X Kush Mints (3.5g) jumped 37.57% to rank 1 and Blue Dream (3.5g) rose 32.07% at rank 5, while Made X GS - Durban Poison Live Resin Disposable (1g) inched up 2.82% at rank 3, which collectively points to Flower reclaiming momentum as Vapor Pens lose some pace. With six of the top ten being Flower SKUs, the product mix is tilting toward inhalable bud strength over single-use hardware despite a $27,900 anchor in the number-two Vapor Pens slot, implying near-term merchandising should weight shelf space and promos toward fast-moving Flower strains while stabilizing flagship disposables.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.