Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Mfny (Marijuana Farms New York) is stocked at 342 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Queens, Rochester, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

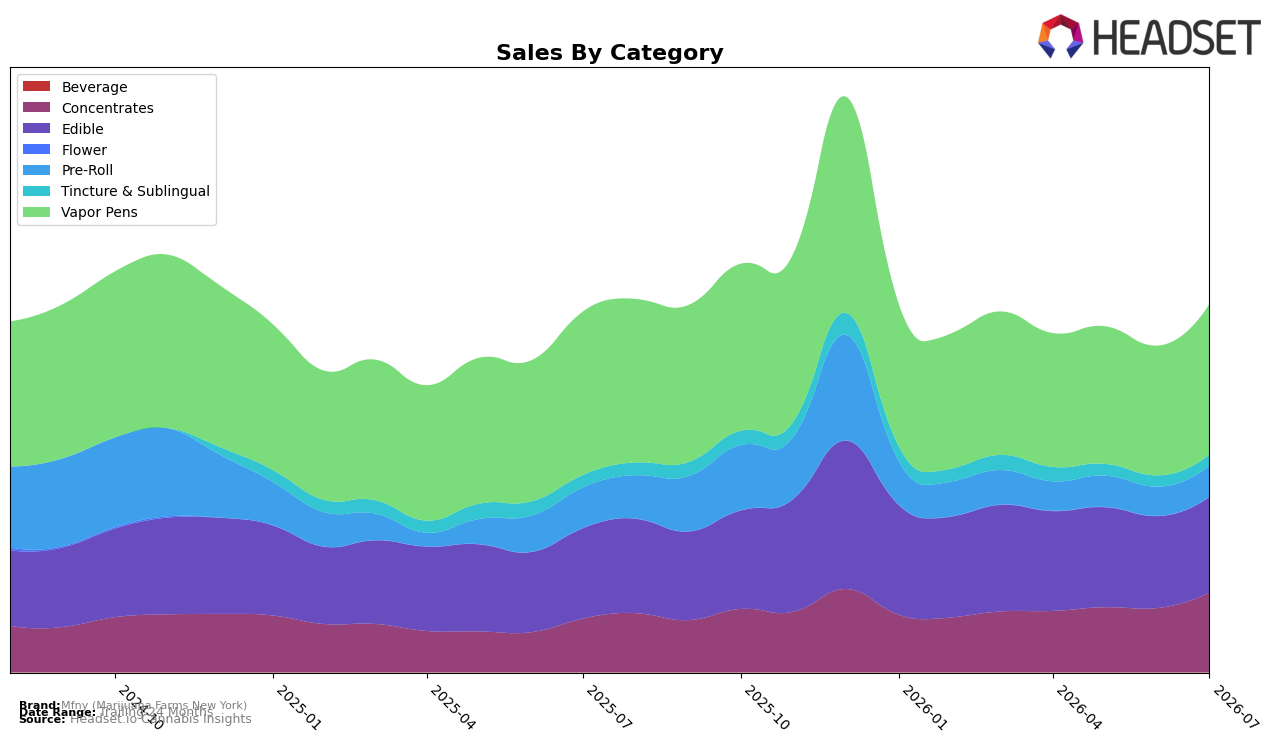

In July 2026, Mfny (Marijuana Farms New York) concentrated 40.94% of sales in Vapor Pens with a month-over-month rise of 15.98% but a year-over-year decline of 7.94%, while Concentrates climbed to a 21.69% share on 24.04% MoM and 48.54% YoY growth. Edible held 25.99% share with 4.09% MoM and 5.76% YoY gains, as Pre-Roll slipped to 8.39% share despite a 6.52% MoM uptick and a 23.60% YoY drop. Tincture & Sublingual represented 2.96% of mix with -2.10% MoM and -11.55% YoY, and Flower remained negligible at 0.02% share with 9.01% MoM and no YoY basis. The pattern indicates a migration toward inhalable formats led by Vapor Pens and high-growth Concentrates, with Edible acting as a stabilizer while Pre-Roll and Tincture & Sublingual contract in relative importance.

With Vapor Pens anchoring mix at 40.94% and a category rank of 5 in New York, the 15.98% MoM rebound alongside a 7.94% YoY decline suggests share defense via recent velocity rather than sustained annual expansion, while Concentrates’ 48.54% YoY surge and 24.04% MoM lift signal headroom to diversify reliance away from a single lead category. Edible’s 5.76% YoY and 4.09% MoM increments, paired with a 14.24% YoY decline in average price at the brand level, point to a value-sensitive consumer mix that can absorb targeted premiumization in Concentrates without eroding overall basket. Net, the mix shifts imply positioning that leans into inhalable potency (Concentrates) to complement a large but volatile Vapor Pens base, using Edible as a demand buffer while deprioritizing Pre-Roll and Tincture & Sublingual where double-digit YoY declines (-23.60% and -11.55%) constrain return on attention.

Competitive Landscape

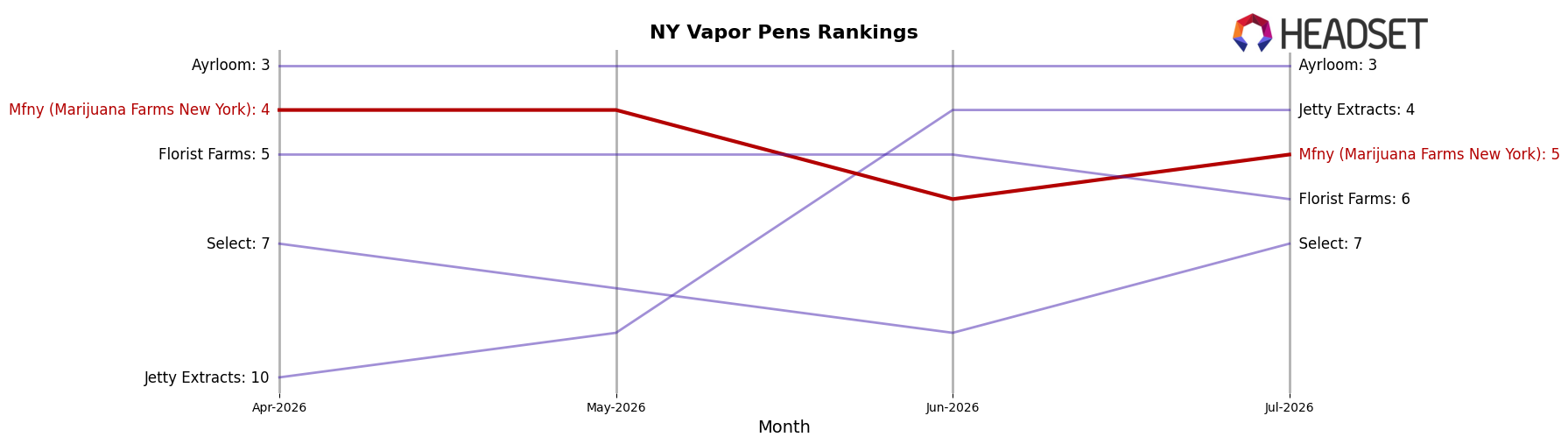

Mfny (Marijuana Farms New York) sits at rank #5 in NY Vapor Pens in July 2026, unchanged from #5 year over year, after slipping from #4 in April 2026 to #5 in July 2026 and peaking at #4 in May 2026; meanwhile, Jetty Extracts surged from #22 to #4 with 199.3% YoY sales growth while Jaunty fell from #1 to #2 with a 24.8% YoY sales decline, and Fernway climbed from #3 to #1 alongside 46.8% YoY sales growth; this stability at #5 alongside upward pressure from a faster-rising #4 and a reshuffling top three implies Mfny’s flat YoY rank masks share compression risk unless it converts its brief May 2026 peak back into sustained gains.

Notable Products

Pina Colada x Strawpaya Live Resin Gummies 10-Pack (100mg) posted the sharpest move in July 2026 with a -10.9% month-over-month decline, sliding to rank 3 while Sour Green Apple x Sour Diesel Live Resin Gummies 10-Pack (100mg) inched up +2.1% at rank 2. Five of the top ten are Edibles, and within that set Sour Fruit Punch x Lemon Sour Dawg Live Resin Gummies 10-Pack (100mg) rose +10.1% to rank 6 as Sour Diesel x Sour Diesel Live Resin Infused Pre-Roll (0.75g) held rank 1 with a modest +2.8% gain. Vapor Pens clustered just behind with Honey Banana Live Resin Cartridge (1g) at rank 7 and Hash Burger Live Resin Cartridge (1g) at rank 8, while Honey Banana Live Rosin Cartridge (0.5g) dipped -2.5% at rank 10, suggesting carts are stable but ceding share of the very top spots to gummies. The pattern implies Mfny (Marijuana Farms New York) is leaning into flavor-driven edibles to anchor traffic while maintaining cartridges as high-value volume drivers, with product rotation in gummies deciding near-term rank volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.