May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

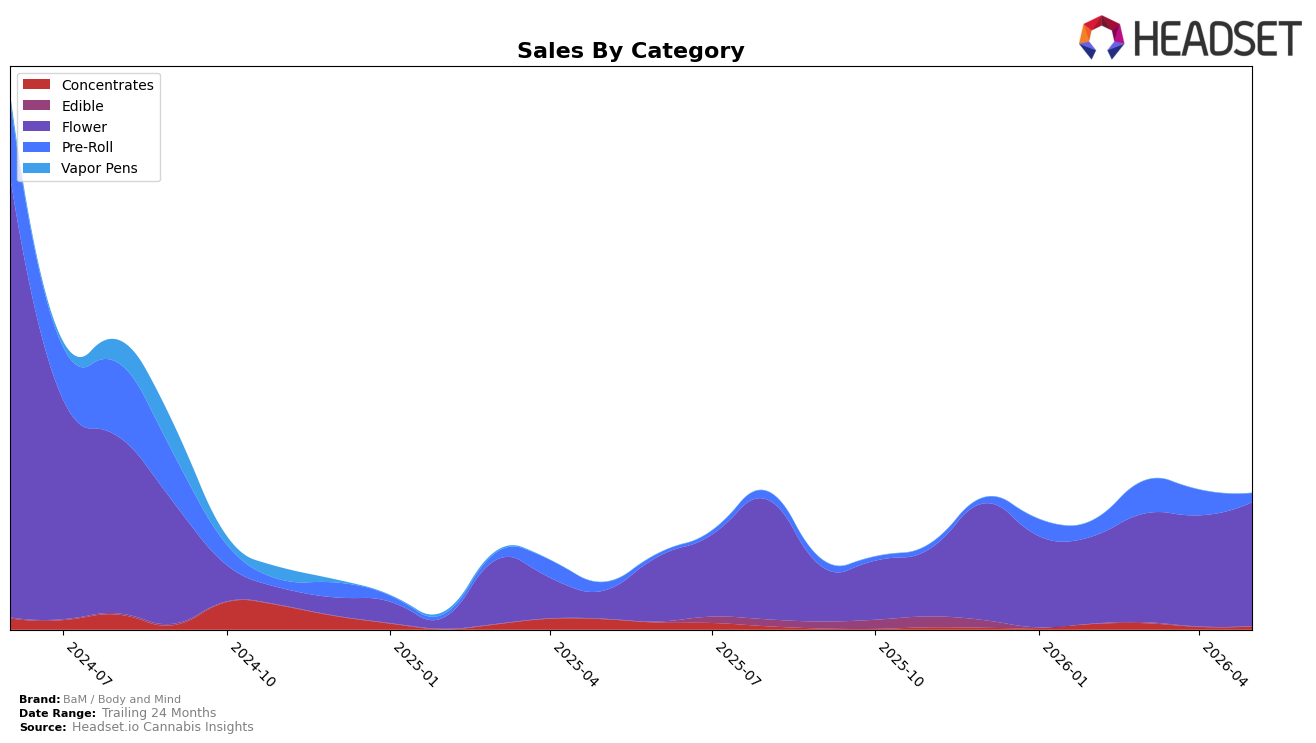

In May 2026, BaM / Body and Mind concentrated 91.29% of sales in Flower with a 347.69% year-over-year lift and an 11.39% month-over-month gain, while Pre-Roll held 6.53% share with 7.81% year-over-year growth but a 65.29% month-over-month decline. Concentrates accounted for 2.18% share with a 70.96% year-over-year contraction yet an 18.21% month-over-month rebound, and the brand’s average price rose 38.97% year over year to one reported dollar figure of 24.87. This mix implies a deliberate tilt toward higher-priced Flower driving the 193.69% brand sales year-over-year increase despite a 72.57% decline over 24 months, concentrating momentum in a single category that amplifies near-term gains while narrowing diversification.

Positioning-wise, anchoring 91.29% share in Flower alongside a rank of 28 in Flower within Nevada indicates scale concentrated in one competitive lane, where the 11.39% month-over-month Flower increase offsets the 65.29% month-over-month Pre-Roll pullback. The 18.21% month-over-month rise in Concentrates against a 70.96% year-over-year decline and the 7.81% year-over-year growth in Pre-Roll together signal limited secondary pillars, implying the brand’s near-term positioning relies on maintaining price‑led Flower velocity while selectively rebuilding smaller formats to reduce reliance on a single category.

Competitive Landscape

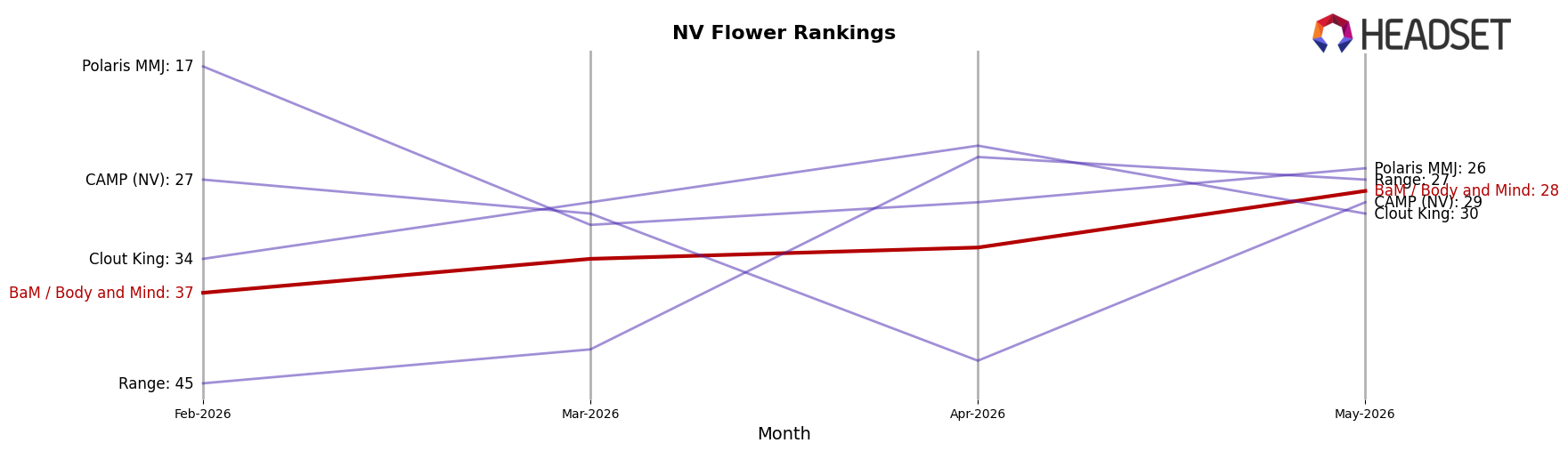

BaM / Body and Mind sits at rank #28 in Nevada Flower for May 2026, improving 40 places year over year from #68 and rising 9 spots since February 2026 from #37; against its history, this sits far below the peak of #8 reached in June 2024 but marks a sustained rebound within the last quarter. While STIIIZY held at #1 year over year (flat at #1 with a -2.3% sales YoY change) and RYTHM moved from #3 to #2 despite a -14.3% sales YoY change, Redwood surged from #54 to #5 on a 917.6% sales YoY increase, indicating that BaM / Body and Mind’s climb is occurring amid divergent competitor momentum; the trajectory from #68 to #28 suggests recaptured distribution or tighter assortment is working, but reclaiming the former #8 position will require pacing closer to the rapid ascent tiers seen by top five movers.

Notable Products

G-Kandy Pre-Roll (1g) posted the steepest movement in May 2026 with a -47.0% month-over-month decline at rank 3, while Pineapple Breeze Pre-Roll (1g) also fell -49.5% at rank 6, indicating sharp pressure on the pre-roll format relative to Flower placements at ranks 1, 2, 4, 5, and 7–9. Pineapple Breeze (3.5g) rose 24.4% month over month to rank 1, whereas LV Glue (14g) dropped -19.7% to rank 4, and Sunset Cookies (3.5g) slid -31.7% to rank 8, creating a split within Flower where only select strains are expanding. With eight of the top ten landing in Flower and only two in Pre-Roll, the mix points to a pivot toward core Flower strains where price-pack architecture can be managed more deliberately, with a single dollar anchor at $42,799 signaling headroom for larger pack sizes while underperforming pre-rolls warrant pruning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.