Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Superflux is stocked at 332 licensed dispensaries across Illinois, New Jersey, and 2 other states, 123 of them in Illinois, with the deepest coverage in Chicago, Normal, Schaumburg, Springfield, and Champaign. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

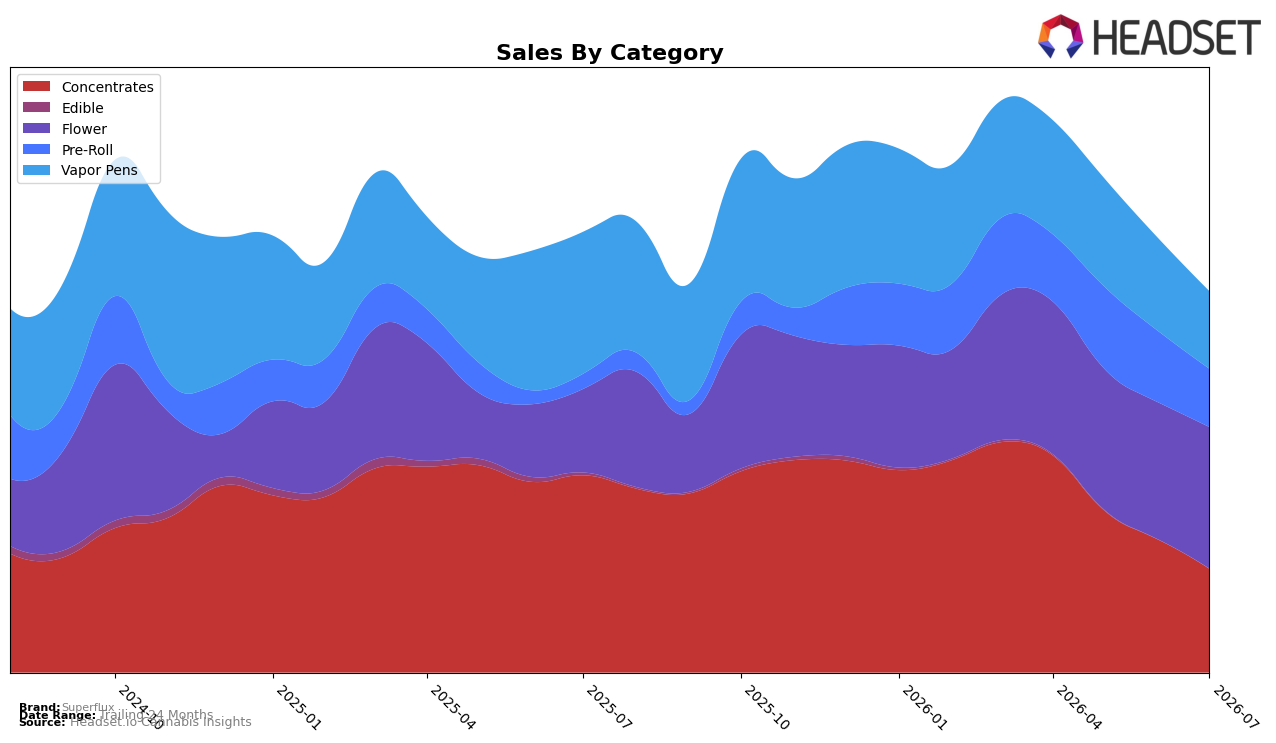

In July 2026, Superflux’s mix tilted toward Flower at 36.99% share with 68.95% YoY growth and a 3.27% MoM increase, while Concentrates fell to 27.15% share with -47.29% YoY and -21.96% MoM. Vapor Pens accounted for 20.35% share with -45.16% YoY and -16.44% MoM, whereas Pre-Roll rose to 15.30% share on 273.94% YoY but slipped -18.23% MoM. Edible remained marginal at 0.20% share with -76.63% YoY and a 6.65% MoM uptick. With the brand’s average price down 24.19% YoY to $29.30 and Flower ranking 39th in New Jersey, the pattern implies a reweighting toward Flower and Pre-Roll to offset steep declines in Concentrates and Vapor Pens, using price to compete for volume.

The shift concentrates risk into inhalables led by Flower (rank 39) and a volatile Pre-Roll that is expanding YoY but contracting MoM, while core extract formats are retreating at double‑digit MoM rates. Given brand sales down 13.41% YoY alongside 8.29% growth over 24 months, the divergence implies a portfolio pivot: defending Flower’s 36.99% share and stabilizing Pre-Roll momentum could recapture lost basket spend from Concentrates (-47.29% YoY) and Vapor Pens (-45.16% YoY), while the lowered average price suggests a value-led positioning that trades margin for retention in New Jersey.

Competitive Landscape

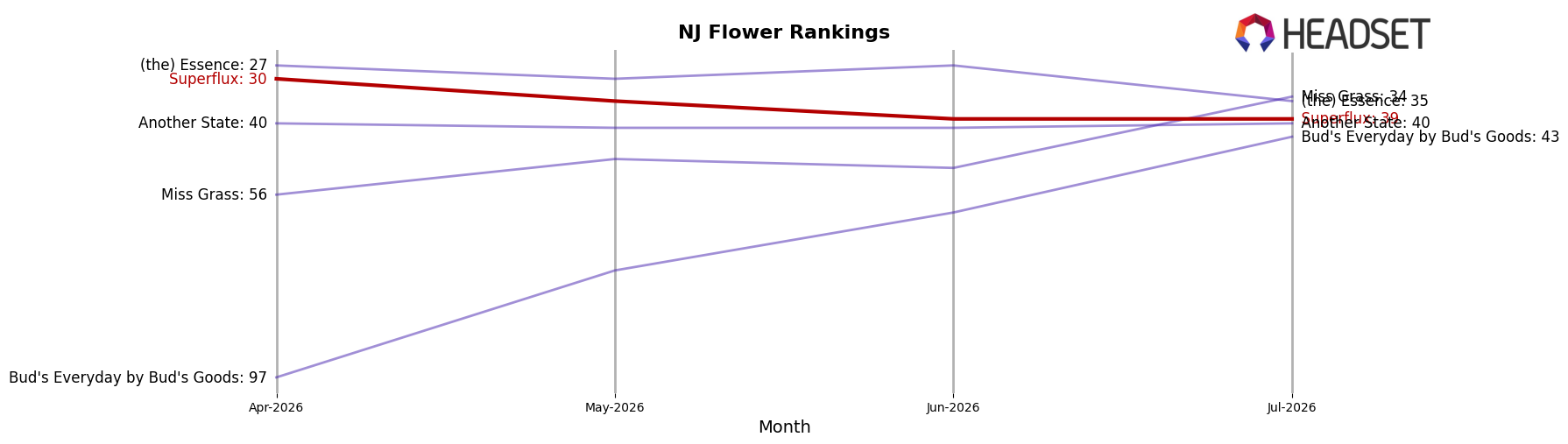

Superflux ranks #39 in NJ Flower in July 2026, down 5 positions year over year from #34 and down 9 positions from its April 2026 peak at #30; in contrast, Ozone slid from #2 to #1 (-13.1% YoY sales) while Find. climbed from #10 to #2 (+129% YoY sales), signaling that Superflux’s shift from #30 three months ago to #39 now is a relative share loss amid competitors moving up the leaderboard faster.

Notable Products

Billionaire (3.5g) posted the steepest movement in July 2026 with a -16.9% month-over-month decline, slipping to rank 5 while Mint Sherbert THCa Diamond Infused Pre-Roll 2-Pack (1g) rose 25.0% to hold rank 1. Four of the top ten are Pre-Roll SKUs concentrated in diamond-infused formats, with Mint Sherbert at rank 1 and Kem Chillz Diamond Infused Pre-Roll 2-Pack (1g) at rank 7, whereas Flower holds ranks 4, 5, 6, 8, 9, and 10 but shows mixed momentum with Grapple Pie Infused Live Resin Ground (3.5g) up 15.5% at rank 4. Grapple Pie Infused Live Resin Ground (3.5g) nearly matches Mint Sherbert’s revenue scale at $46,539 while delivering a 15.5% lift, in contrast to the -16.9% slide for Billionaire (3.5g) that pressures the mid-pack. The pattern implies Superflux is tilting toward infused formats—especially diamond-infused Pre-Rolls—while pruning or repositioning legacy Flower strains that are losing rank and velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.