Market Insights Snapshot

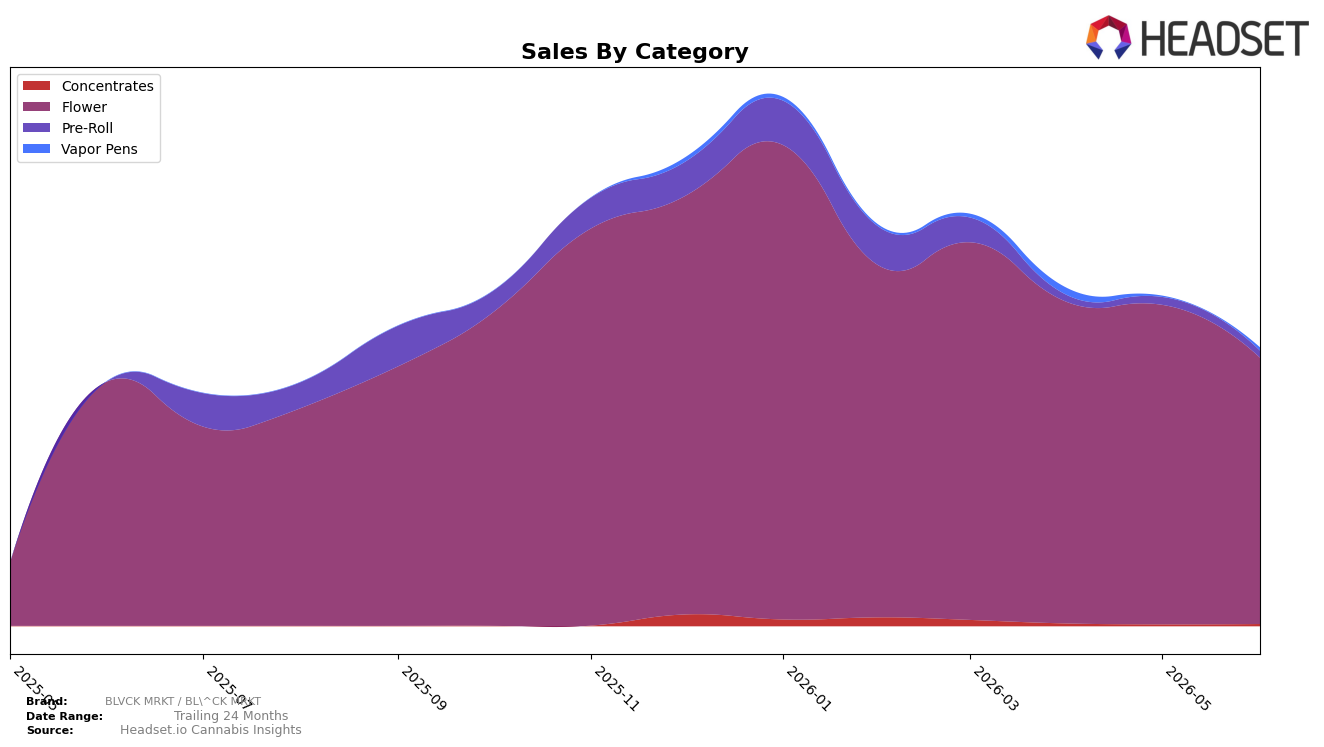

Flower carried 95.94% share in June 2026 with average price at $29.64, rising 8.87% year over year but falling 16.66% month over month; meanwhile, Vapor Pens jumped 213.63% MoM to 1.01% share while Pre-Roll slipped 11.02% MoM to 2.39% share. Despite a 29.31% YoY drop in overall average price to $29.22 and total brand sales up 13.48% YoY, Concentrates lifted 23.15% MoM to 0.67% share, pointing to a basket tilting slightly toward non-Flower formats even as Flower dominance persists. The pattern implies June 2026 was a price-led volume month where softening Flower momentum (-16.66% MoM) was partially offset by trial and expansion in Vapor Pens (+213.63% MoM) and Concentrates (+23.15% MoM), keeping category breadth from narrowing further.

With Flower anchoring rank position 27 in Maryland and accounting for 95.94% of mix, the sharp MoM decline in Flower (-16.66%) alongside triple‑digit MoM gains in Vapor Pens (+213.63%) signals a shift toward mitigating single-category risk rather than chasing immediate share in Flower. The 13.48% YoY sales increase alongside a 29.31% YoY price reduction suggests elasticity headroom that can support cross-category entry, and the incremental 1.01% share in Vapor Pens plus 0.67% in Concentrates indicates footholds where price architecture can be tested without eroding the Flower base; the implication is that near-term positioning favors a value-led gateway in Flower while seeding higher-ASP formats to rebalance mix and reduce sensitivity to Flower rank volatility.

Competitive Landscape

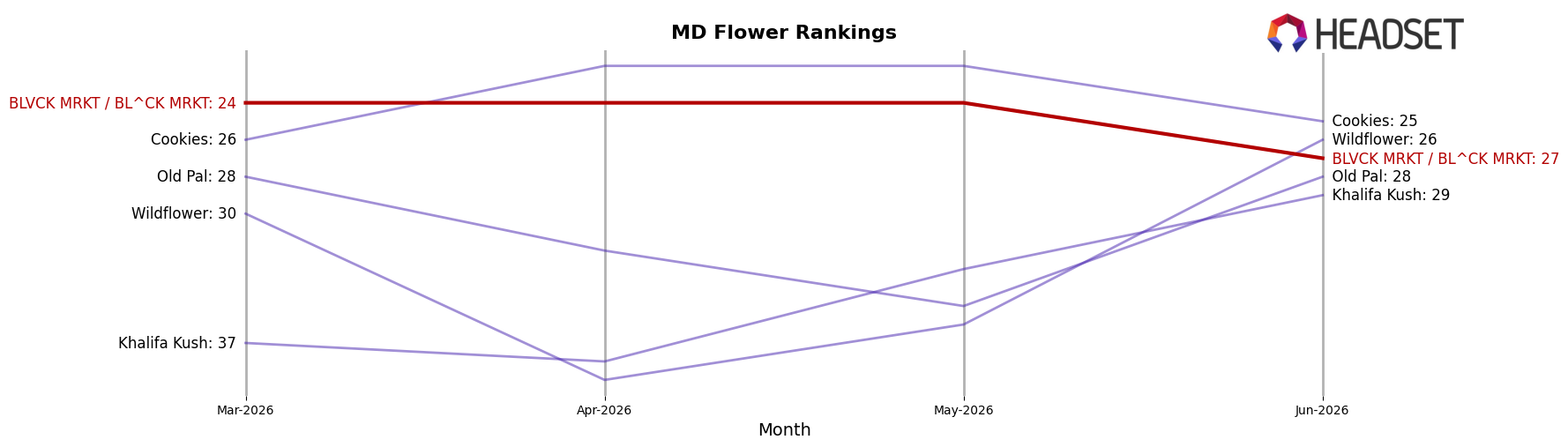

BLVCK MRKT / BL^CK MRKT sits at rank #27 in June 2026, improving 4 positions from #31 year over year but slipping 3 spots from #24 in March 2026; against the category’s leaders, RYTHM advanced from #3 to #2 while Fade Co. moved the other direction from #2 to #3, indicating share is actively reallocating at the top even as BLVCK MRKT / BL^CK MRKT lingers outside the top 20 after a peak at #21 in November 2025. The non-linear path—year-over-year gain of 4 ranks paired with a recent 3-rank quarter-over-quarter slide—implies the brand is caught between gradual rebuilding and short-term loss of momentum, and the thesis is that without a step-change in velocity BLVCK MRKT / BL^CK MRKT’s trajectory points to oscillation in the mid-20s rather than a return to its #21 peak.

Notable Products

Lemon Barz (3.5g) posted the steepest decline at -73.29% month over month while holding rank 8, a sharper drop than Oreo Blizzard (3.5g) at -35.22% and Charm Biscuitz (3.5g) at -32.64%, and this downswing concentrates risk in the lower half of the ranking. At the top, Super Lemon Haze (3.5g) grew 9.97% to rank 1 while Murphyz Law (3.5g) surged 32.24% at rank 2, and with Flower occupying 10 of the top 10 SKUs the mix indicates reliance on a single category that is tilting toward a narrower set of leaders. The pattern implies BLVCK MRKT / BL^CK MRKT is consolidating around a couple of Flower flagships while pruning or de-emphasizing weaker mid-tier Flower SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.