May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

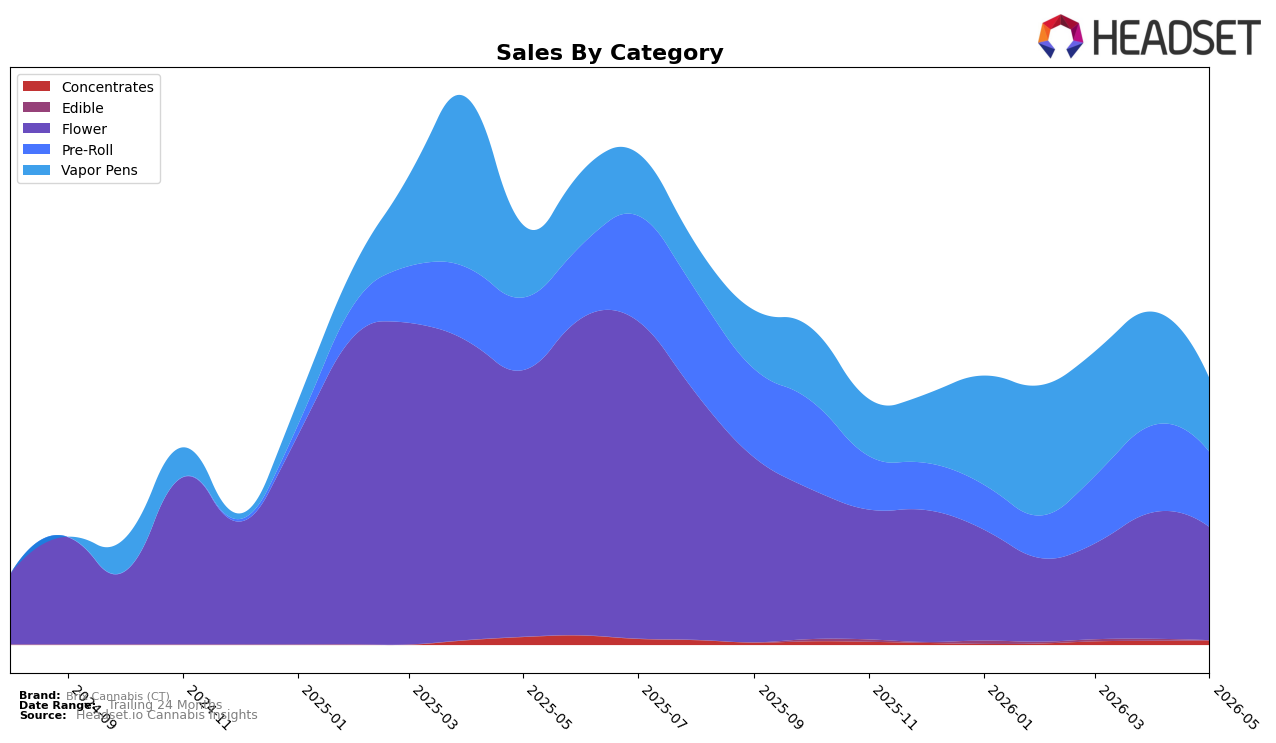

In May 2026, Brix Cannabis (CT) concentrated 42.54% of sales in Flower with year-over-year decline of 57.64% and month-over-month decline of 10.55%, while Pre-Roll held 28.18% share with a 3.40% YoY increase but a 13.94% MoM pullback. Vapor Pens accounted for 27.67% share with 1.74% YoY growth but a steep 35.11% MoM contraction, and Concentrates remained small at 1.61% share with a 44.50% YoY decline but a 7.07% MoM uptick. With an average price down 34.30% YoY to $20.14 and Flower’s average price at $30.10, the mix shows reliance on a shrinking Flower base while Pre-Roll and Vapor Pens provide limited YoY relief; the pattern implies the brand is shifting toward lower-price, higher-velocity formats but suffered a May 2026 volume shock in inhalables.

Brix Cannabis (CT)’s category skews suggest a repositioning opportunity: Flower’s 42.54% share and 57.64% YoY drop constrain rank mobility even as the brand sits at rank 11 in Flower in Connecticut, while Pre-Roll’s 28.18% share and 3.40% YoY gain indicate a defendable entry point if the 13.94% MoM slide is addressed. Vapor Pens’ 27.67% share with 1.74% YoY growth but 35.11% MoM decline signals sensitivity to price and inventory cycles given the brand-wide 34.30% YoY average price decrease, and Concentrates’ 7.07% MoM rise off a 1.61% share base suggests tactical upside without material mix impact; together, these shifts imply Brix Cannabis (CT) can stabilize share by reallocating from declining Flower into Pre-Roll and select Vapor Pen SKUs while using targeted price architecture rather than broad discounting.

Competitive Landscape

Brix Cannabis (CT) sits at rank #11 in CT Flower for May 2026, down 8 positions from rank #3 in May 2025, while its 3-month position was #12, a 1-place improvement into May 2026; the brand’s peak was #2 in July 2025, marking a 9-rank slide from that high to today. In contrast, Theraplant climbed from #8 to #1 year over year with 137.3% sales growth, and RYTHM rose from #11 to #4 with 65.5% sales growth, whereas Affinity Grow moved from #10 to #5 despite a -6.4% sales change; this competitive reshuffling, alongside Brix Cannabis (CT)’s 8-rank YoY decline and 1-place quarter-to-date gain, implies the brand is stabilizing off its July 2025 peak but is ceding share to faster-rising rivals.

Notable Products

Purple Milk (3.5g) posted the steepest move in May 2026 with a -58.1% month-over-month decline, sliding to rank 8, which rebalances attention toward higher-velocity items. Jungle Cake (3.5g) rose 10.4% MoM to rank 3 while Jungle Cake Pre-Roll (1g) fell 15.6% to rank 5, indicating divergence between the same strain’s Flower and Pre-Roll formats. Pre-Rolls occupy six of the top ten positions, yet two of the category’s leaders fell by double digits with Cap Junk Pre-Roll (1g) down 35.6% at rank 4 and Jungle Cake Pre-Roll (1g) down 15.6% at rank 5, suggesting format breadth without consistent pull-through. The pattern implies Brix Cannabis (CT) is tilting toward Flower-led revenue concentration, with Pre-Rolls requiring tighter SKU curation to stabilize rank and margin.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.