Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

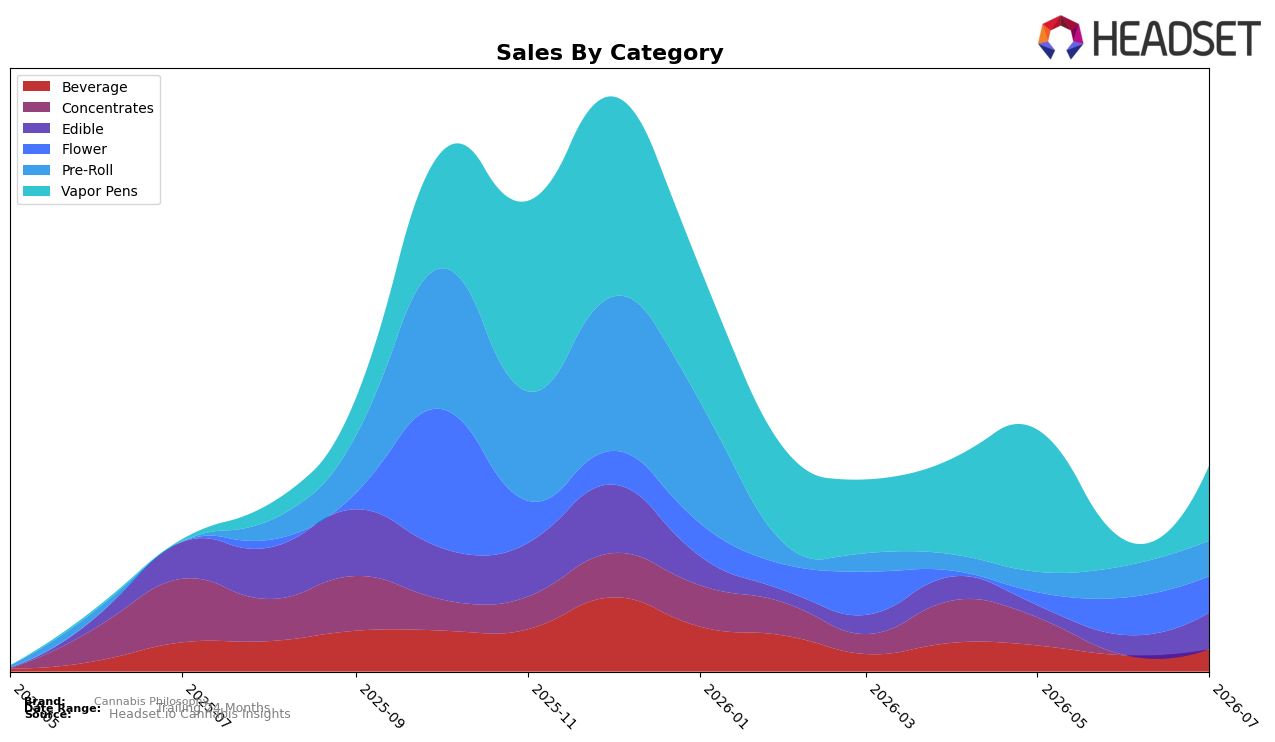

Cannabis Philosophy shifted toward Vapor Pens in July 2026, with the category rising to 36.58% share and a 3,482.73% year-over-year surge alongside a 191.46% month-over-month jump, while Edible held 17.72% share with a -0.82% year-over-year change but an 82.25% month-over-month gain. Flower maintained 17.71% share with a -2.56% month-over-month move and no year-over-year read, as Pre-Roll sat at 17.21% share with an 11.95% month-over-month uptick; Beverage represented 10.77% share with a -24.04% year-over-year decline but a 36.34% month-over-month lift. With brand-wide sales up 56.21% year over year and average price down 28.72%, the emerging Vapor Pens weight plus price compression implies a volume-led expansion that is rebalancing the category mix toward inhalables at the expense of lagging Beverage and flat Edible trajectories on a yearly basis.

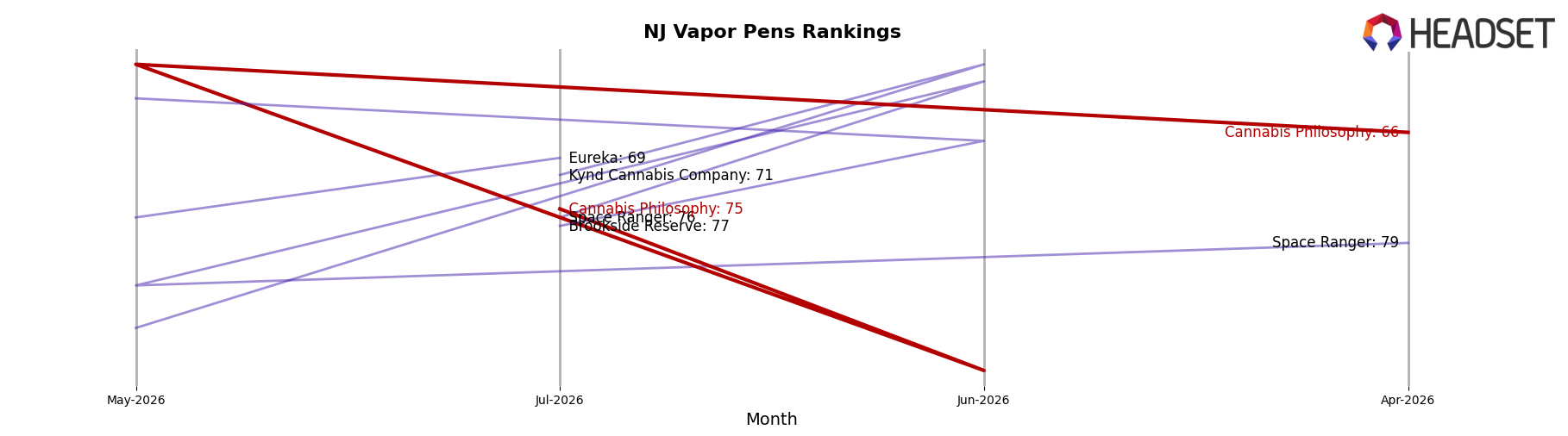

Positioning is now anchored by Vapor Pens as the lead category, but the 75 rank in Vapor Pens in New Jersey suggests that, despite the 191.46% month-over-month acceleration, the brand competes from a lower-tier placement that may cap immediate visibility. The simultaneous 82.25% month-over-month rise in Edible and 11.95% month-over-month growth in Pre-Roll, combined with a -2.56% month-over-month dip in Flower, points to a consumer shift toward ready-to-use formats; together with a 36.34% month-over-month Beverage rebound against a -24.04% year-over-year base, this indicates trial and promotion dynamics rather than durable equity in ingestibles. Net effect: the mix is tilting toward higher-velocity inhalables while ingestibles act as opportunistic contributors, implying that sustained growth will depend on defending the July 2026 gains in Vapor Pens while selectively pruning low-yield Beverage exposure.

Competitive Landscape

Cannabis Philosophy sits at rank 75 in July 2026, improving 12 positions from rank 87 year over year, but slipping 9 spots from rank 66 in April 2026; the brand is also down 34 places from its peak rank 41 in November 2025, indicating momentum has cooled after a prior climb. In directional contrast, Select holds rank 1 with a -8.9% year-over-year sales change while RYTHM advanced from rank 8 to rank 5 alongside a 43.9% sales increase, suggesting competitive pressure at the top is reshuffling faster than Cannabis Philosophy’s mid-tier recovery. The pattern implies Cannabis Philosophy’s rank trajectory is stabilizing above last year’s baseline but losing short-term ground, which points to a need for near-term activation to prevent further drift while the market rewards faster-moving leaders.

Notable Products

Lemon Lime Ice Pops (10mg) posted the standout move in July 2026 with a month-over-month jump of 409%, vaulting to rank 2 while the Lemonade Drink Mix 10-Pack (100mg) climbed 78% to rank 4. In contrast, Lime OG Infused Whole Flower (3.5g) fell 16% to rank 3, marking the steepest decline among the top ten despite Flower typically anchoring basket size with its $12,883 in sales. Four of the top ten are Edibles, and within that group Oatmeal Raisin Cookies 10-Pack (100mg) rose 69% to rank 9 while Banana Cake Bites 10-Pack (100mg) increased 69% to rank 10, concentrating momentum in ingestibles rather than inhalables. The pattern implies Cannabis Philosophy is shifting demand toward entry-priced, flavor-led Edibles that can scale quickly, reducing reliance on Flower volatility and rebalancing the mix toward repeatable, impulse-driven formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.