Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Lobo is stocked at 67 licensed dispensaries across New York, New Jersey, and Illinois, 41 of them in New York, with the deepest coverage in New York, Queens, Rochester, Albany, and Astoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

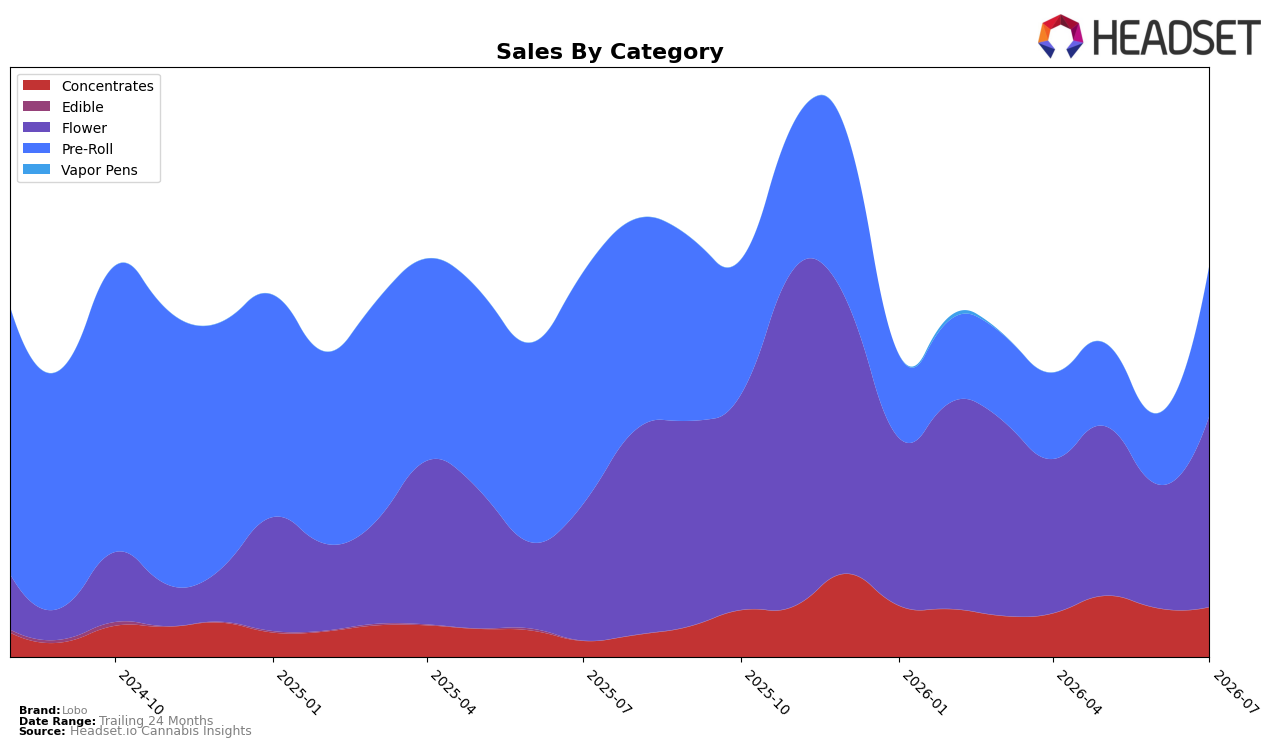

In July 2026, Lobo’s mix tilted back toward Flower at 48.8% share as Flower sales rose 40.2% year over year and 54.9% month over month, while Pre-Roll held 38.5% share despite a 35.0% year-over-year decline paired with a 112.4% month-over-month surge. Concentrates expanded to 12.7% share with a 210.2% year-over-year increase and a 2.4% month-over-month uptick, which, together with a 17.1% year-over-year drop in average price to $29.10, implies volume-led recovery concentrated in Flower and volatile short-cycle swings in Pre-Roll. With Flower ranked 70th in New Jersey and Lobo’s brand sales up 1.9% year over year but down 22.7% versus 24 months, the pattern points to near-term category reacceleration that hasn’t yet translated into sustained multi-period rank gains.

The mix shift—Flower’s 54.9% month-over-month lift alongside Concentrates’ 210.2% year-over-year rise but only 2.4% month-over-month movement—suggests Lobo is leaning into core Flower demand while testing depth in Concentrates, with Pre-Roll’s 112.4% month-over-month rebound offsetting its 35.0% year-over-year drag. Coupled with the 17.1% year-over-year price decline and a 1.9% year-over-year brand sales increase, the positioning signal is toward share defense via accessible pricing in high-velocity Flower and opportunistic re-entry in Pre-Roll, implying that sustained improvement in a 70th-category rank context will require stabilizing Pre-Roll’s year-over-year trajectory while converting Concentrates’ growth into repeatable monthly gains.

Competitive Landscape

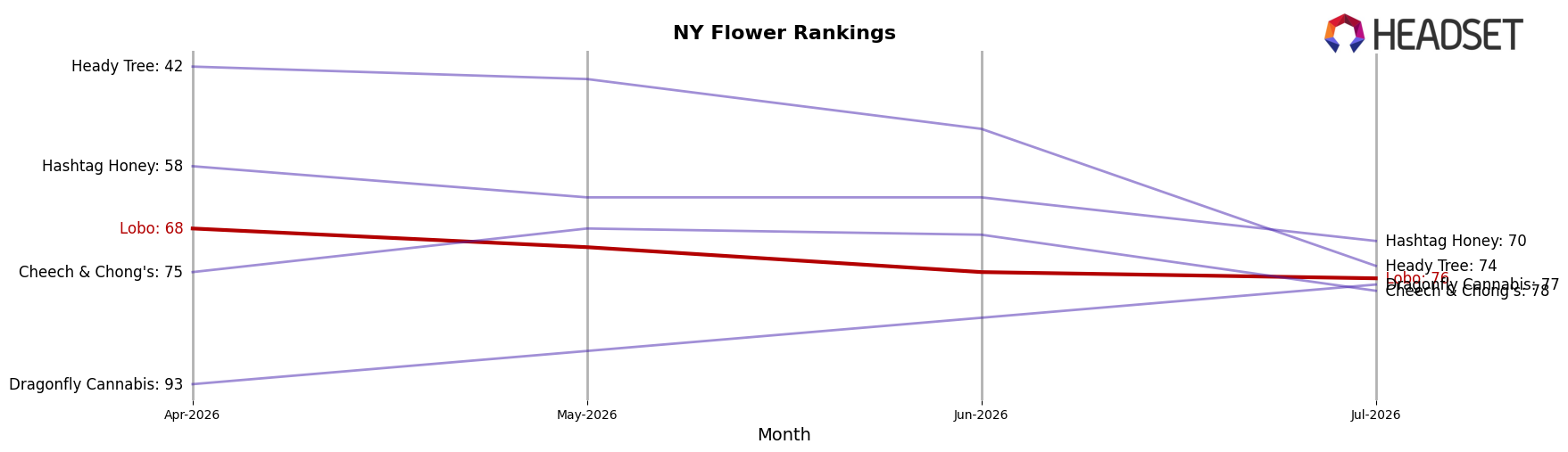

Lobo is ranked #76 in July 2026 in NY Flower, down 7 positions year over year from #69, and down 8 positions from its three-month rank of #68, while its peak of #47 in November 2025 is 29 spots higher than today; in contrast, Find. rose from #8 to #1 with a 46.7% year-over-year sales increase, and Grassroots climbed from #15 to #5 alongside a 79.8% sales gain. The split where Dank. By Definition slid from #1 to #3 despite a 51.5% sales decline, while Leal advanced from #7 to #2 with 34.4% growth, indicates competitive churn concentrated at the top ranks as Lobo’s position migrates downward; the pattern implies Lobo’s rank trajectory is being shaped more by faster-rising rivals displacing the middle tier than by uniform category growth, signaling a need to reclaim higher-share SKUs or channels to reverse rank loss.

Notable Products

Bold - Blue Dream Infused Pre-Roll (1g) posted the largest month-over-month surge at +255.9% to reach a top-2 rank, while Blue Dream Diamond Infused Pre-Roll 5-Pack (2.5g) climbed +162.2% to rank 1. Blueberry Diesel Infused Flower (3.5g) advanced +115.3% while holding rank 5, and Pre-Rolls occupied four of the top ten positions, indicating a tilt toward infused convenience formats over traditional Flower. The product mix points to Lobo leaning into Blue Dream-led, infused Pre-Roll momentum as the primary commercial engine for July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.