May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

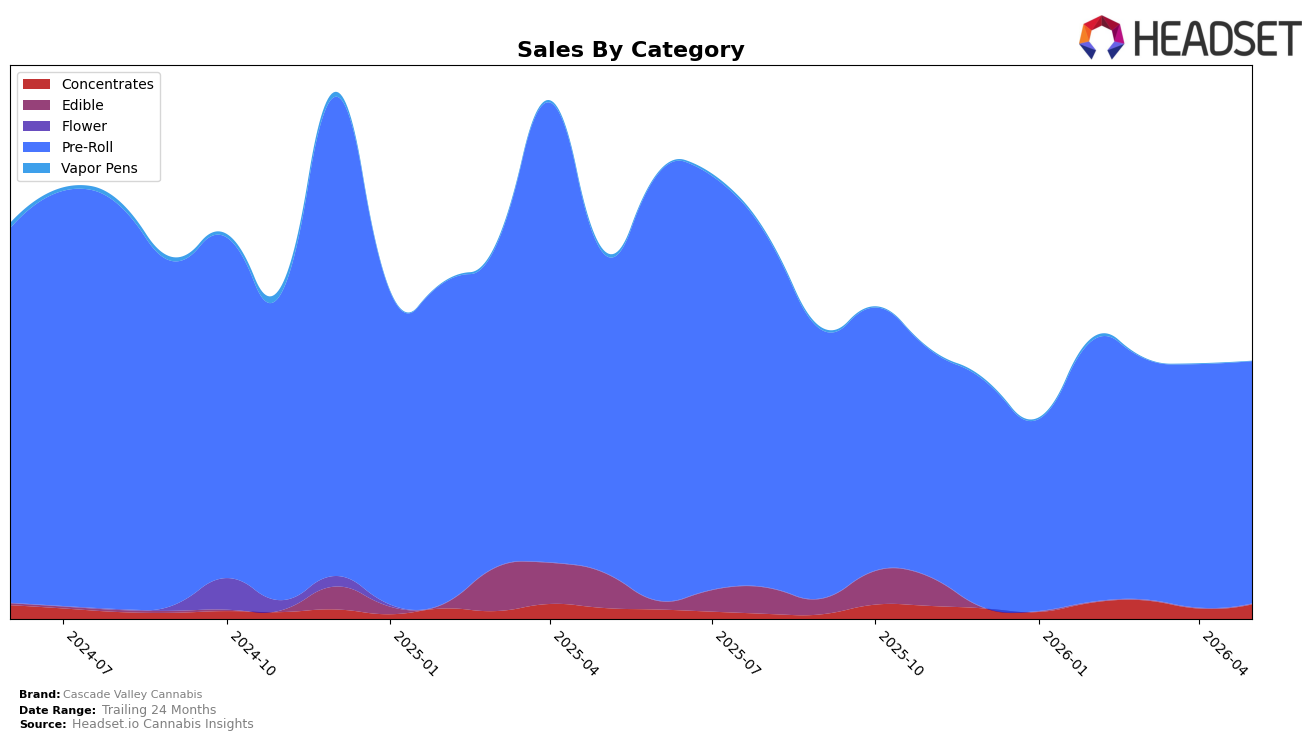

In May 2026, Cascade Valley Cannabis concentrated 94.40% of sales in Pre-Roll with a year-over-year decline of 24.02% and a month-over-month dip of 0.51%, while Concentrates rose to 5.60% share with a 32.89% YoY increase and a 41.01% MoM surge; the average price fell 59.36% YoY to $4.92, aligning with Pre-Roll’s low average ticket of $4.71. Within Oregon Pre-Roll, the brand sat at rank 26, indicating mid-pack placement amid a shrinking core category and a rapidly expanding secondary category; the pattern implies overexposure to a declining Pre-Roll base and an emerging pivot toward Concentrates that is beginning to offset volume pressure.

The mix shift—Concentrates’ 41.01% MoM and 32.89% YoY growth against Pre-Roll’s 0.51% MoM and 24.02% YoY declines—suggests the brand’s positioning is tilting from a value-heavy Pre-Roll focus to a two-tier strategy where Concentrates act as the growth and margin stabilizer. With the brand down 30.19% YoY in total sales and anchored at rank 26 in Oregon Pre-Roll, maintaining low Pre-Roll pricing while expanding Concentrates share toward double digits would reduce reliance on a weakening lead category and reposition the portfolio toward steadier rank resilience.

Competitive Landscape

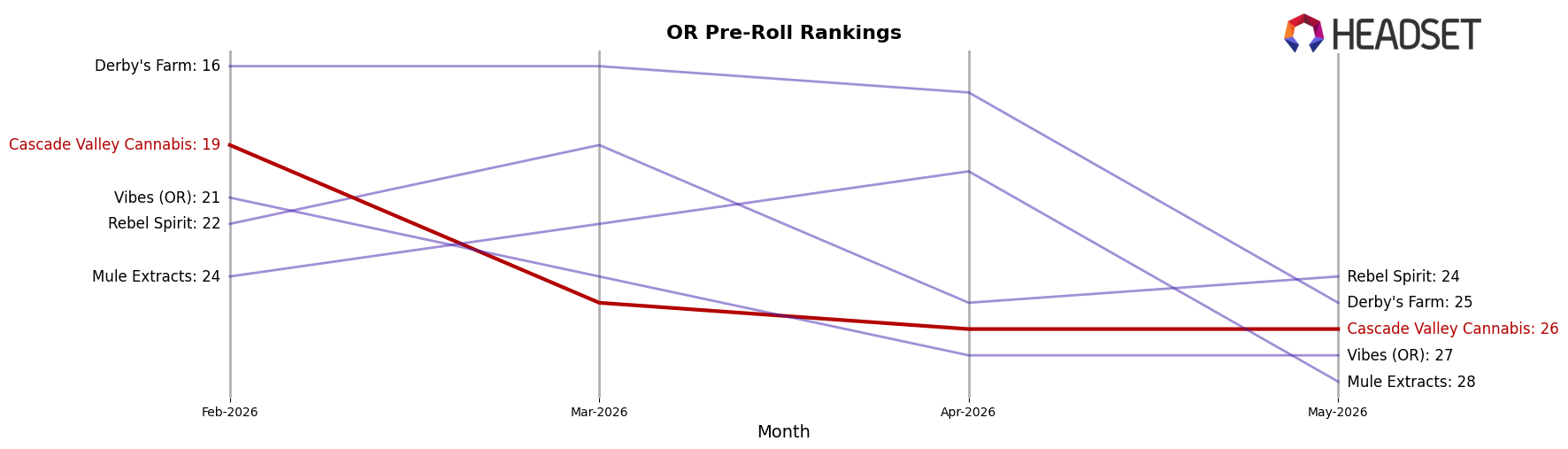

Cascade Valley Cannabis is ranked #26 in OR Pre-Roll in May 2026, down 6 positions year over year from #20, and 7 positions below its February–May 2026 three-month reference of #19; the slide from a peak of #9 in December 2024 to #26 spans a 17-rank decline. Meanwhile, STiCKS sits at #1 after improving from #2 year over year with 144.25% sales growth, and Kaprikorn advanced from #5 to #2 alongside 85.55% sales growth, indicating leaders are moving up as Cascade Valley Cannabis moved down; this divergence implies Cascade Valley Cannabis is ceding rank to faster-advancing rivals and will need a material reversal to reenter the top 20.

Notable Products

GMO Pre-Roll (1g) delivered the standout move in May 2026 with a +501% month-over-month surge to rank 1, while Scorpion Tears Pre-Roll (1g) fell 33% to rank 5, marking a sharp divergence at the top of the lineup. Dragon Candy Pre-Roll (1g) also accelerated with a +62% month-over-month gain to rank 8, as Ice Cream Cake Pre-Roll (1g) advanced a steadier +14% to rank 2, concentrating momentum among the upper tier. With all ten top products in the Pre-Roll category and four of the top five holding ranks 1–5, the portfolio is consolidating around a pre-roll-led strategy that favors breakout winners over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.