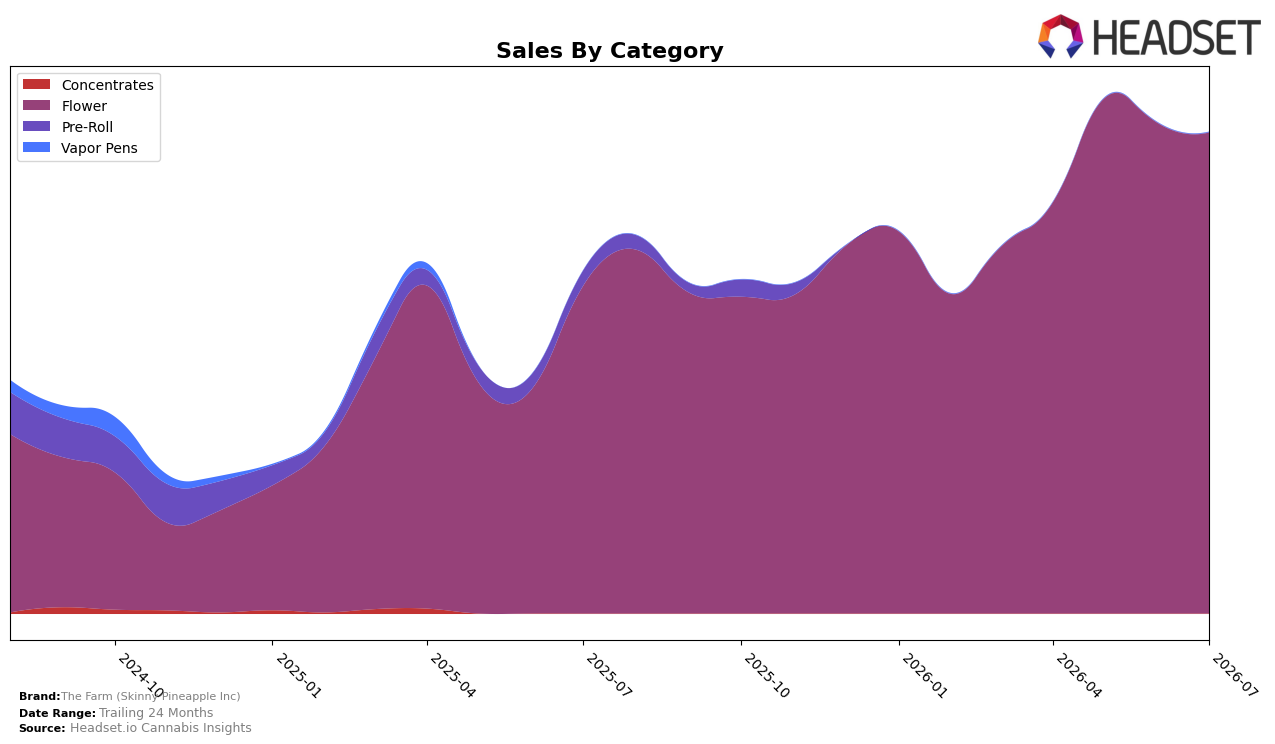

Market Insights Snapshot

In July 2026, The Farm (Skinny Pineapple Inc) concentrated entirely in Flower, with category share at 100.0% and average price at $30.83, while Flower sales were up 47.0% year over year and down 1.9% month over month. Brand-level sales were up 40.6% YoY alongside a 34.3% YoY increase in average price, placing the brand’s mix as fully single-category and exposed to short-term MoM volatility despite YoY gains; the pattern implies reliance on Flower-led pricing and velocity rather than diversification.

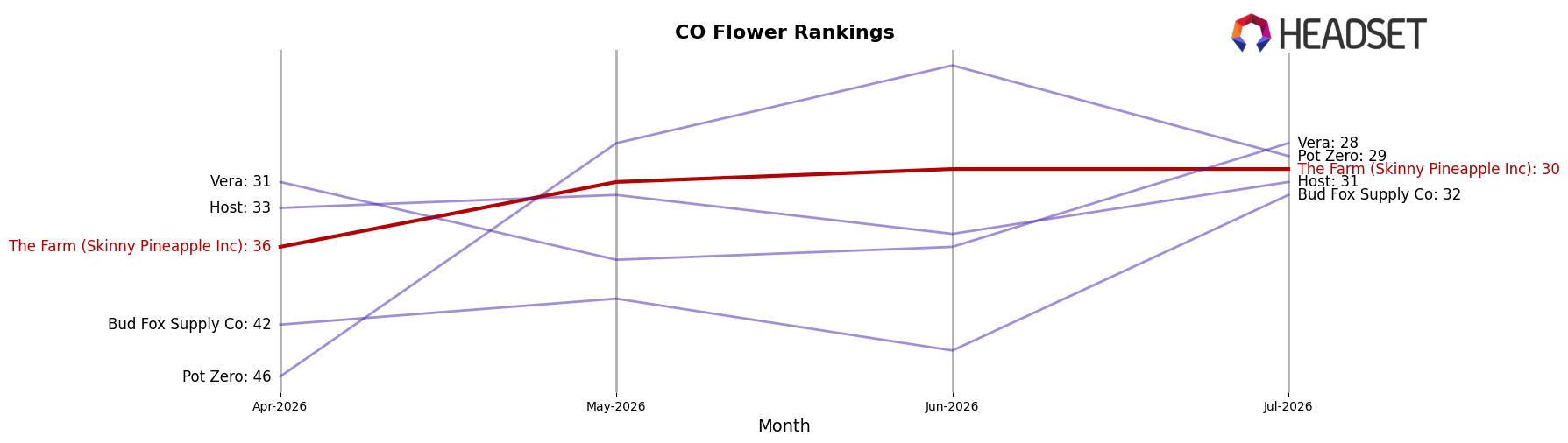

Within Colorado Flower, the brand’s rank at 30 against a 47.0% YoY Flower lift and a 1.9% MoM dip indicates mid-pack positioning that skews toward price-led contribution rather than breadth. With 100.0% of sales in Flower and a 34.3% YoY price increase, the brand’s competitive stance hinges on sustaining price realization while countering MoM softness, implying the need to shore up rank through deeper SKU depth or regional penetration rather than category expansion alone.

Competitive Landscape

The Farm (Skinny Pineapple Inc) sits at rank #30 in Colorado Flower in July 2026, improving 21 positions from #51 year over year, and climbing 6 spots from #36 over the last three months; this marks a peak rank of #30 in July 2026 while the category’s leaders tightened their hold, with Seed & Strain Cannabis Co. edging up from #2 to #1 and Good Chemistry Nurseries sliding from #1 to #3 as its sales fell 8.7% year over year. Against this backdrop, Natty Rems surged from #23 to #5 alongside a 168.5% YoY sales lift while Triple Seven (777) advanced from #3 to #2 with a 56.8% YoY increase, indicating that The Farm’s rise into the top 30 is occurring amid rapid upward mobility at the top and suggests its trajectory is consolidation into mid-tier relevance rather than immediate contention for top-10 share.

Notable Products

Cast Away (14g) delivered the headline move in July 2026 with a 151.9% month-over-month surge to rank 1, while Fried Strawberries (14g) also jumped 56.0% to rank 3, indicating momentum concentrated at the top of the list. Tally Mon (14g) fell 25.7% to rank 10 and Mob Boss (14g) slipped 4.6% to rank 7, suggesting weaker pull-through for lower-tier placements even as Original Glue (14g) nudged up 3.1% at rank 6. Eight of the top ten are Flower SKUs, and the gap between a triple‑digit gainer at rank 1 and a double‑digit decliner at rank 10 points to a portfolio skew that rewards large-size Flower winners over smaller or aging cuts. The pattern implies The Farm (Skinny Pineapple Inc) is consolidating volume behind a few high-velocity Flower anchors, prioritizing depth in leading strains over breadth across formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.