Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

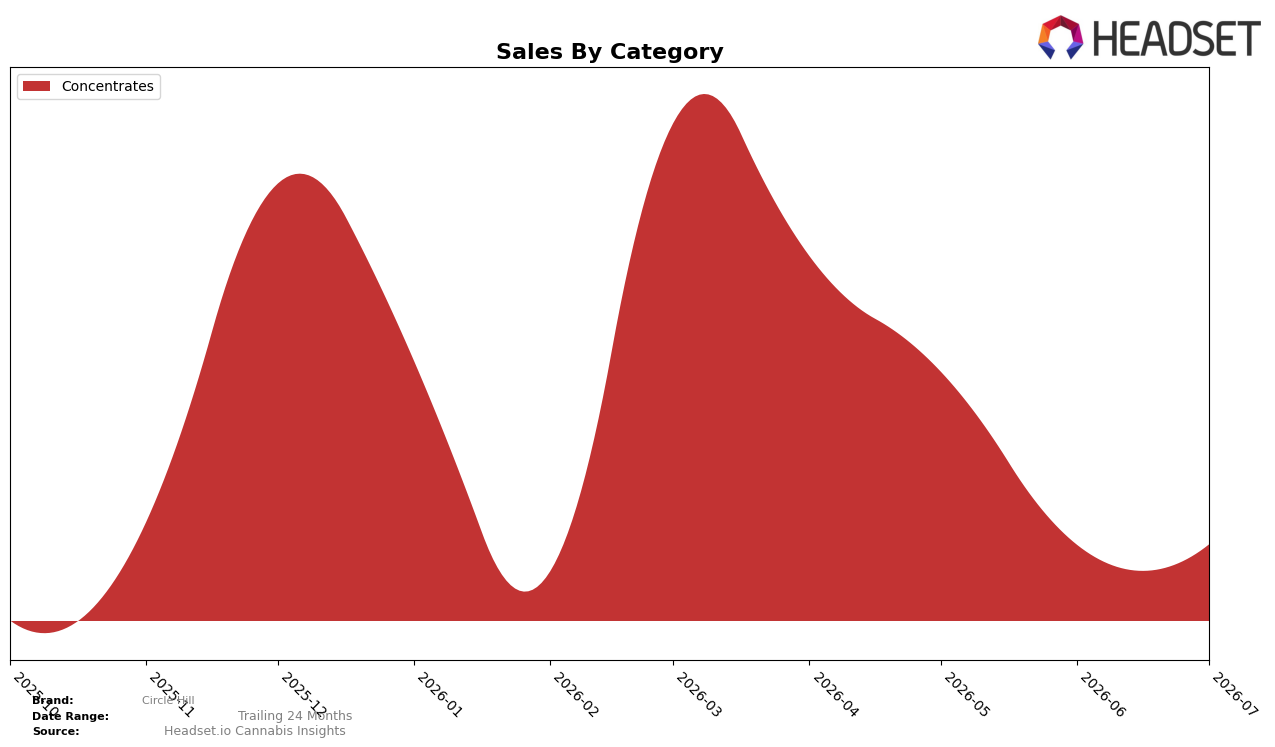

Circle Hill operated as a single-category brand in July 2026, with Concentrates accounting for 100.0% of sales and an average price of $71.11. Month over month, Concentrates grew 53.2%, while category share remained static at 100.0%, and the brand held rank 35 in New York. The absence of a year-over-year rate alongside a 53.2% MoM swing indicates a reliance on recent momentum rather than multi-period depth; this pattern implies a concentrated bet that magnifies volatility and compresses diversification options.

With rank 35 in New York Concentrates and a 100.0% category mix, Circle Hill’s positioning hinges on extracting more velocity per SKU rather than expanding breadth, because any shift in Concentrates demand directly translates to brand-level movement. The 53.2% MoM lift coupled with a static 100.0% mix suggests pricing and promotion levers inside Concentrates, not portfolio expansion, are driving outcomes; the implication is that future gains will depend on moving rank upward from 35 through deeper penetration within the existing segment rather than cross-category spillover.

Competitive Landscape

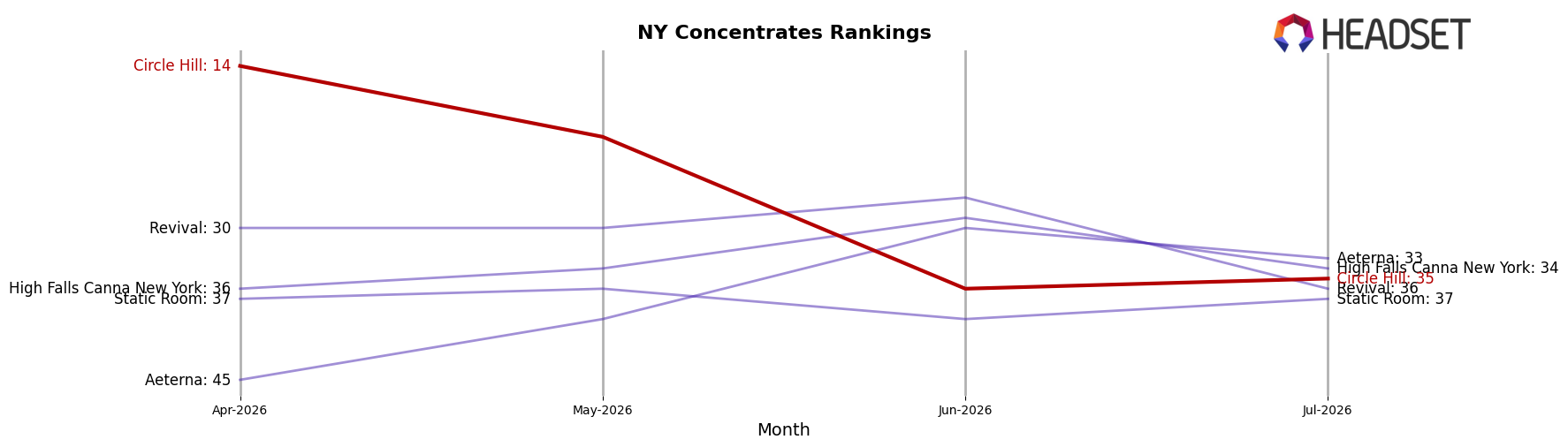

Circle Hill sits at rank 36 in July 2026, down 22 places from rank 14 in April 2026, and 26 spots below its peak rank of 10 in March 2026; that trajectory contrasts with Mfny (Marijuana Farms New York) holding rank 1 year over year at 1, and UMAMII jumping from rank 27 to rank 3 alongside a 1,758.2% year-over-year sales gain. With Jetpacks edging up from rank 3 to rank 2 while posting 56.4% YoY growth and Nyce improving from rank 9 to rank 5 with 68.5% YoY growth, Circle Hill’s slide from mid-teens to mid-30s implies a loss of velocity against faster-rising rivals and points to share erosion unless distribution or product mix is realigned.

Notable Products

Rainbow Push Pop #4 Solventless Live Rosin (2g) posted the standout move in July 2026 with a 387% month-over-month surge and climbed to rank 8, while Dulce De Uva Live Rosin Badder (2g) fell 70.8% and slipped to rank 9; among the winners, Rainbow Push Pop #4 Cold Cured Live Rosin (2g) also jumped 91.5% to rank 7. Dulce De Uva Live Rosin (1g) advanced 240.6% to rank 1 as Dulce de Uva Live Rosin (2g) rose 221.5% to rank 6, and four of the top ten are 2g concentrates, indicating a tilt toward larger pack sizes. The concentration of eight Concentrates SKUs in the top ten with both triple-digit gains and double-digit declines suggests volatile trade-ups where format and weight drive share more than flavor alone.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.