Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

City Trees is stocked at 73 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Reno, Henderson, North Las Vegas, and Sparks. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

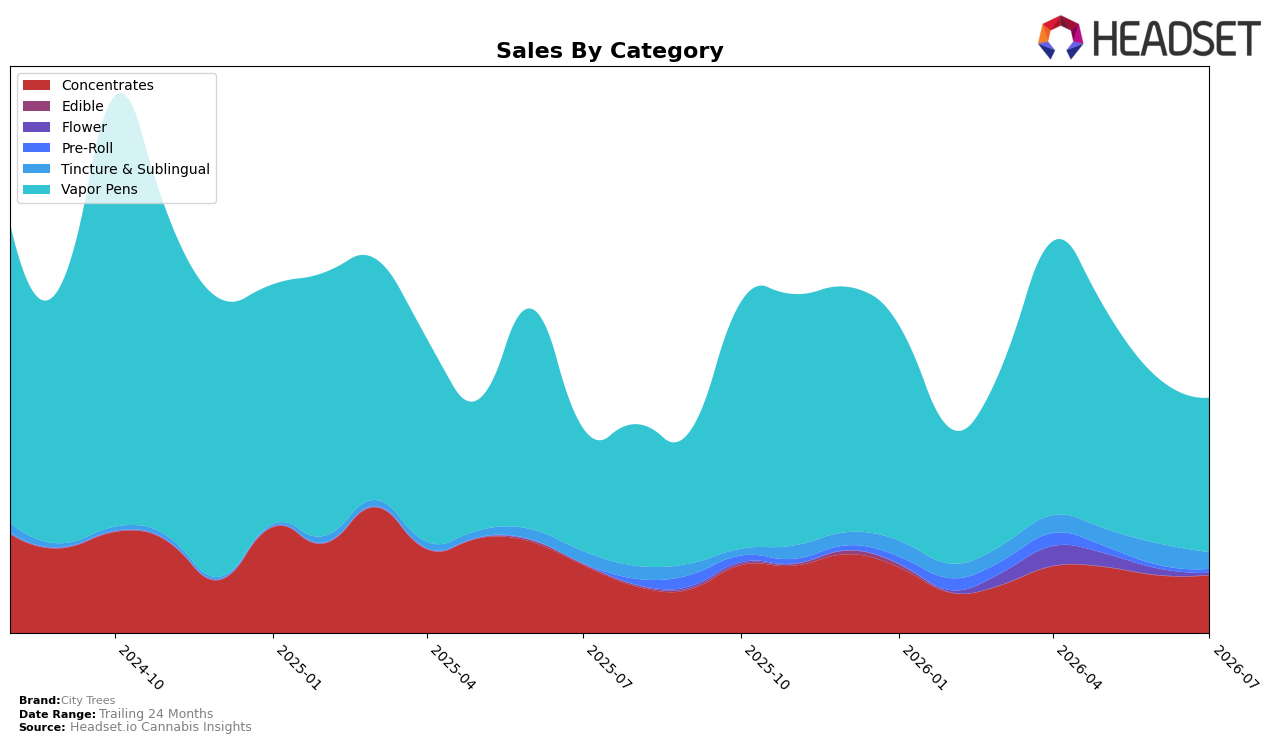

City Trees concentrated 66.09% of July 2026 sales in Vapor Pens with 25.86% year-over-year growth but a 6.65% month-over-month decline, while Concentrates held 24.71% share with a 14.95% year-over-year contraction and a 0.39% month-over-month uptick. Tincture & Sublingual rose 40.27% year-over-year but fell 22.50% month-over-month to 7.02% share, and Pre-Roll expanded 13.87% month-over-month to 1.53% share as Flower collapsed 75.52% month-over-month to 0.65% share. With average price down 6.60% year-over-year to $20.40 and Vapor Pens anchored at 66.09% share, the mix signals a price-led, cartridge-centric portfolio that is gaining annual traction while giving back near-term momentum in July 2026.

In Nevada Vapor Pens, City Trees is ranked 11, and the 25.86% year-over-year lift in the core category alongside a 22.50% month-over-month pullback in Tincture & Sublingual indicates reliance on a single growth engine that is vulnerable to monthly volatility. The simultaneous 0.39% month-over-month stabilization in Concentrates and a 13.87% month-over-month rise in Pre-Roll suggest a hedging pivot at the margins, while the 6.65% month-over-month decline in Vapor Pens and a 75.52% month-over-month drop in Flower imply that assortment pruning is concentrating demand into fewer, price-sensitive SKUs. This pattern implies City Trees is positioned as a value-leaning Vapor Pens specialist in Nevada, with rank 11 leaving headroom if the brand converts Tincture & Sublingual’s 40.27% year-over-year growth into steadier monthly sell-through and sustains Concentrates’ slight month-over-month improvement.

Competitive Landscape

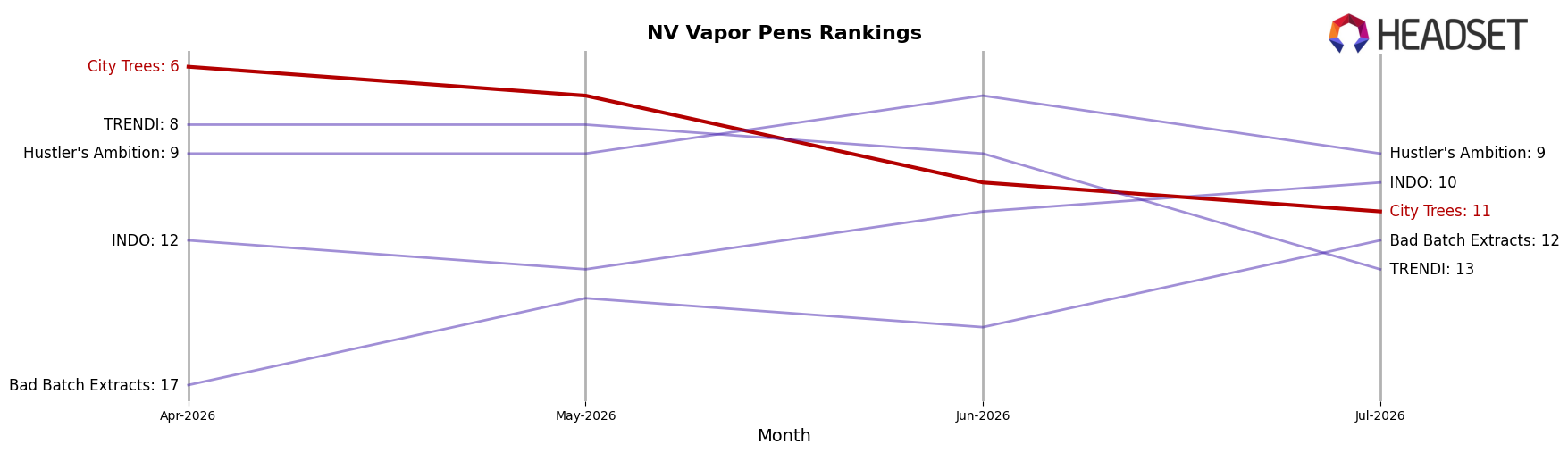

City Trees sits at rank #11 in NV Vapor Pens in July 2026, improving 5 positions year over year from #16 while sliding 5 spots since April 2026 from #6, indicating a rebound in annual standing but a recent quarter softening. Competitors moved differently: Rove held #1 while its sales fell 31.8% YoY and AiroPro rose to #5 from #8 YoY with 104.2% sales growth, a directional climb that outpaced City Trees’ drop from its #5 peak in October 2024 to #11 now. The pattern implies City Trees’ YoY rank gain masks a mid-2026 loss of momentum versus faster-advancing rivals, signaling the need to stabilize quarterly rank to prevent further share leakage.

Notable Products

Pink Lemonade Distillate Cartridge (1g) set the tone with a -20.8% month-over-month drop to rank 2 in July 2026, while Biscotti Pre-Roll (1g) also slipped -12.8% at rank 1, signaling pressure at both the top position and the primary trailing SKU. At the same time, Pink Lemonade Distillate Disposable (1g) climbed +18.8% to share rank 7 and Gasolina Distillate Cartridge (1g) rose +15.9% at rank 3, contrasting with a -27.2% decline for Fruity Pebbles OG Distillate Cartridge (1g) at rank 6. With eight of the top ten rooted in Vapor Pens and one disposable posting $21,123, the mix points to a pivot toward disposables and select flavors within pens as cartridges fragment and the lone Pre-Roll leader softens.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.