Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

TRENDI is stocked at 30 licensed dispensaries across Nevada and California, 28 of them in Nevada, with the deepest coverage in Las Vegas, North Las Vegas, Carson City, Elko, and Ely. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

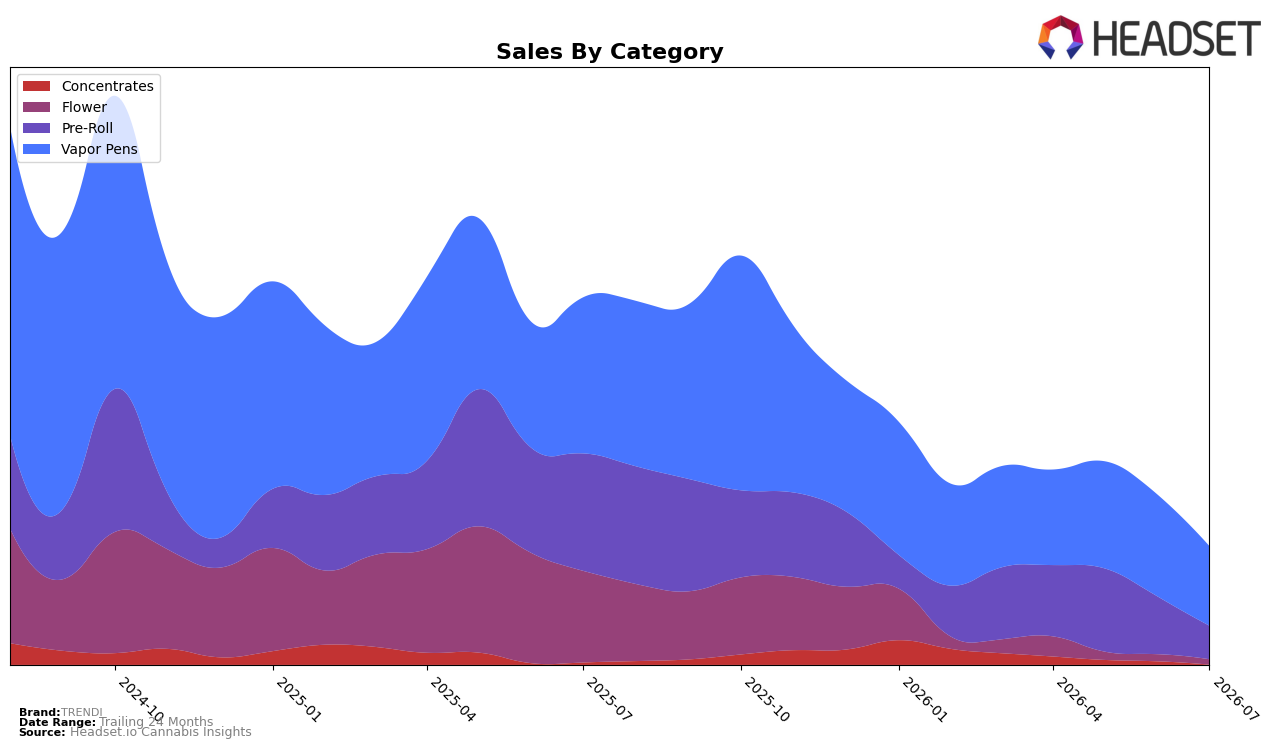

In July 2026, TRENDI’s mix tilted further toward Vapor Pens at 54.28% share with year-over-year sales down 45.20% and month-over-month down 19.22%, while Pre-Roll held 27.22% share with a steeper 64.37% YoY decline and 34.08% MoM drop. Flower contributed 10.73% of sales but contracted 82.50% YoY and 8.77% MoM, as Concentrates at 7.77% share softened 13.70% YoY and 19.87% MoM; combined with a 32.82% YoY fall in average price to $17.31, the mix indicates price compression hitting higher-volume formats and accelerating category-specific pullbacks. The pattern implies TRENDI is consolidating around Vapor Pens while shedding breadth in Pre-Roll and Flower, with relative resilience in Concentrates helping cushion, but not offset, the double-digit MoM declines across three of four categories.

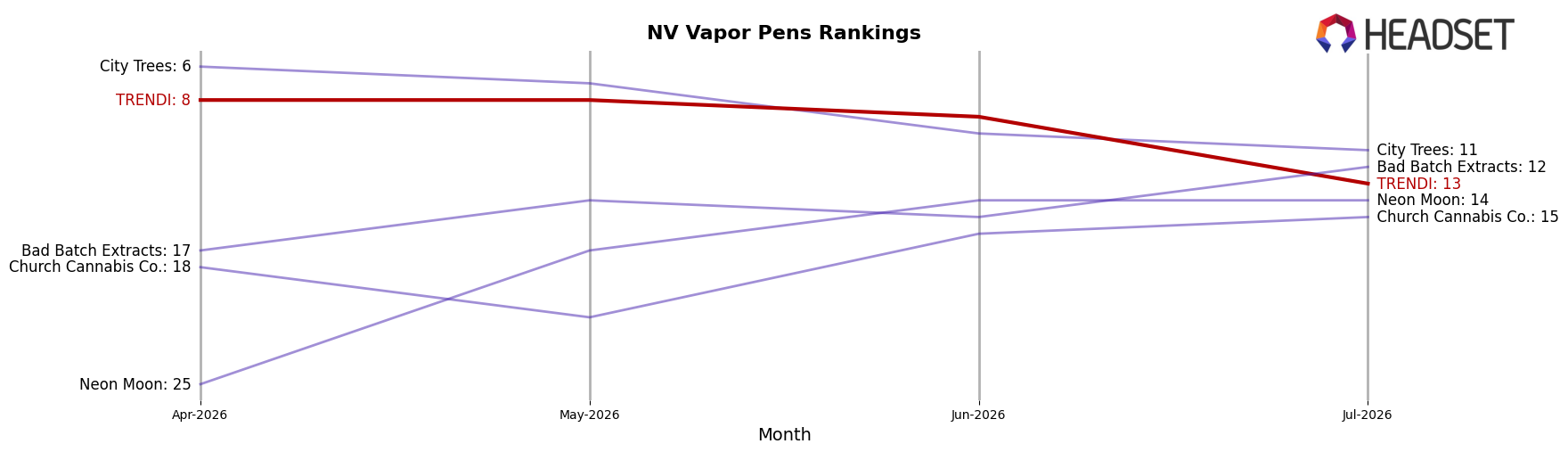

TRENDI’s Vapor Pens rank of 13 in Nevada within the segment, paired with a 19.22% MoM slide and a 45.20% YoY contraction, signals mid-pack positioning vulnerable to further share erosion unless mix and price strategy shift toward stickier subsegments. With Pre-Roll down 34.08% MoM and Flower down 8.77% MoM, the brand’s heavier reliance on a single lead category magnifies volatility, while Concentrates’ smaller base and 13.70% YoY decline suggest limited buffer; the implication is that TRENDI needs to re-weight toward faster-recovering formats or ladder Vapor Pens into value tiers to stabilize rank and protect share.

Competitive Landscape

In July 2026, TRENDI sits at rank #13 in NV Vapor Pens, down 7 positions from rank #6 year over year and 5 positions from rank #8 in April 2026, while its peak at #4 in October 2024 underscores a two-year slide; meanwhile, Rove holds #1 despite a 31.8% YoY sales decline and STIIIZY remains #2 with a steeper 38.6% YoY drop, whereas AiroPro climbed from #8 to #5 on 104.2% YoY growth—this spread implies TRENDI’s ranking pressure is less about category contraction and more about losing relative momentum to select growers even as top incumbents retrench.

Notable Products

Gorilla Glue #4 Infused Pre-Roll 3-Pack (1.5g) led July 2026 with a 94.2% month-over-month surge to rank 4, while Heavy D Pre-Roll (1g) rose 36.7% to rank 7, indicating momentum concentrated in higher-value pre-roll formats. Four of the top ten are Pre-Roll SKUs, clustering at ranks 1, 2, 3, 4, 5, 7, and 10, whereas the leading Vapor Pens SKU sits at rank 6 with no comparable gain cited; this pattern points to pre-rolls outpacing other formats in short-term velocity. Flower presence at ranks 8 and 9 without reported month-over-month lifts, compared with a near-doubling in an infused pre-roll and a mid-tier gain in a standard pre-roll, implies TRENDI’s near-term growth is leaning into infused and multi-pack pre-rolls rather than traditional flower or disposables.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.