Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

INDO is stocked at 12 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Ely, Henderson, and Reno. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

INDO’s category mix in July 2026 concentrated 98.95% of sales in Vapor Pens, with Pre-Roll at 1.05%, while overall brand sales fell 84.79% year over year and average price rose 9.67%. Within Vapor Pens, sales grew 1.11% YoY and 39.05% month over month, contrasted by Pre-Roll contracting 62.06% YoY and 48.53% MoM, and the average price in Vapor Pens at $33.33 closely tracked the brand’s $33.34. With Vapor Pens ranked 10 in Nevada, the mix shift paired with price inflation implies the brand is leaning into a single-category recovery where month-over-month gains are offsetting cross-category decline, positioning July’s rebound as category-specific rather than portfolio-wide.

The 39.05% MoM lift in Vapor Pens paired with a 48.53% MoM drop in Pre-Roll signals resource and demand consolidation toward a top-10 category position, while the 1.11% YoY Vapor Pens increase amid an 84.79% YoY brand decline indicates category insulation against broader contraction. The 9.67% YoY price increase alongside a 62.06% YoY fall in Pre-Roll suggests price tolerance in the core while peripheral segments face elasticity limits, implying INDO’s positioning is to defend share via Vapor Pens scale and pricing while de-prioritizing Pre-Roll until mix efficiency improves in Nevada.

Competitive Landscape

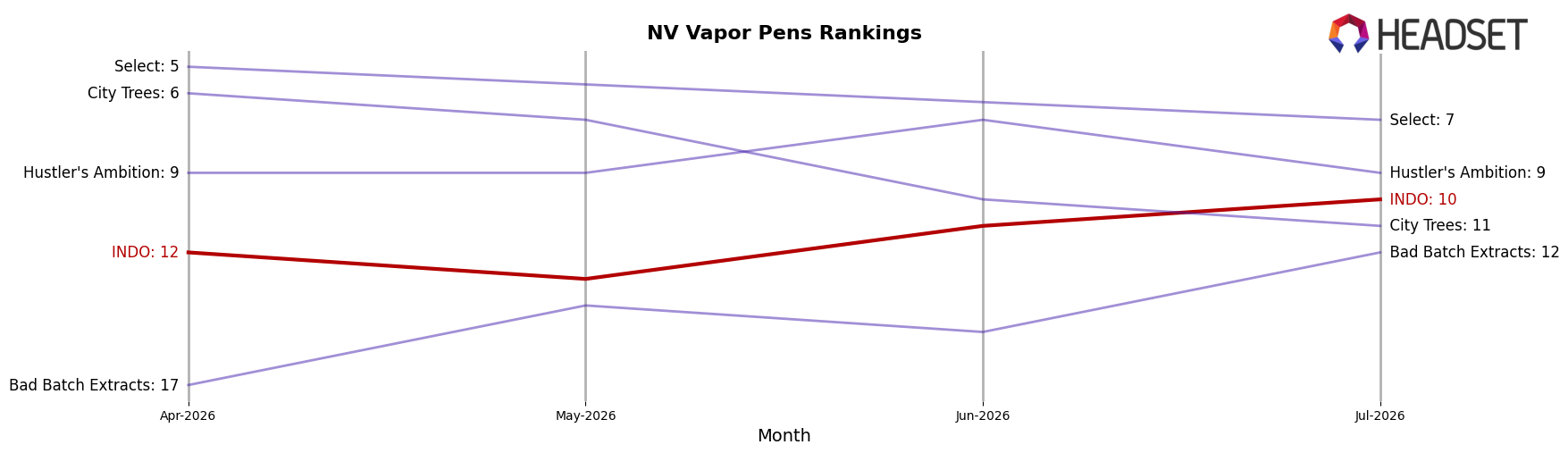

INDO sits at rank #10 in Nevada Vapor Pens in July 2026, unchanged from #10 year over year, while improving 2 positions versus April 2026’s #12 and still 3 spots below its February 2026 peak at #7; meanwhile, category leader Rove held #1 with a -31.8% YoY sales change and STIIIZY stayed #2 with a -38.6% YoY sales change, whereas AiroPro advanced from #8 to #5 on 104.2% YoY growth. The flat YoY rank at #10 combined with a 2-position quarter-on-quarter climb implies INDO is stabilizing its placement but must convert incremental momentum into share gains to avoid being outpaced by faster-rising mid-pack movers.

Notable Products

Blue Zkittles Distillate Disposable (2g) led July 2026 with a 110% month-over-month surge to rank 1, outpacing Pineapple Jack Botanical Terpene Distillate Disposable (2g) at rank 2 with a 59% gain, while Indopuff - Pineapple Jack Distillate Disposable (0.9g) slid 10% to rank 9. Three SKUs in the top four posted positive gains of 33% or more, and four of the top ten are 2g Vapor Pens, indicating the higher-capacity format is concentrating share at the top. Despite small pullbacks of 5% at rank 7 and 5% at rank 10, the mix skews toward up-tiered 2g lines anchored by Blue Zkittles and Pineapple Jack, pointing to a deliberate trade-up strategy. This pattern implies INDO is consolidating leadership around 2g disposables, reallocating demand from smaller 0.9–1g variants toward higher-ticket units, with July 2026 revenue near $31.9k on the leading SKU supporting premiumization.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.