May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

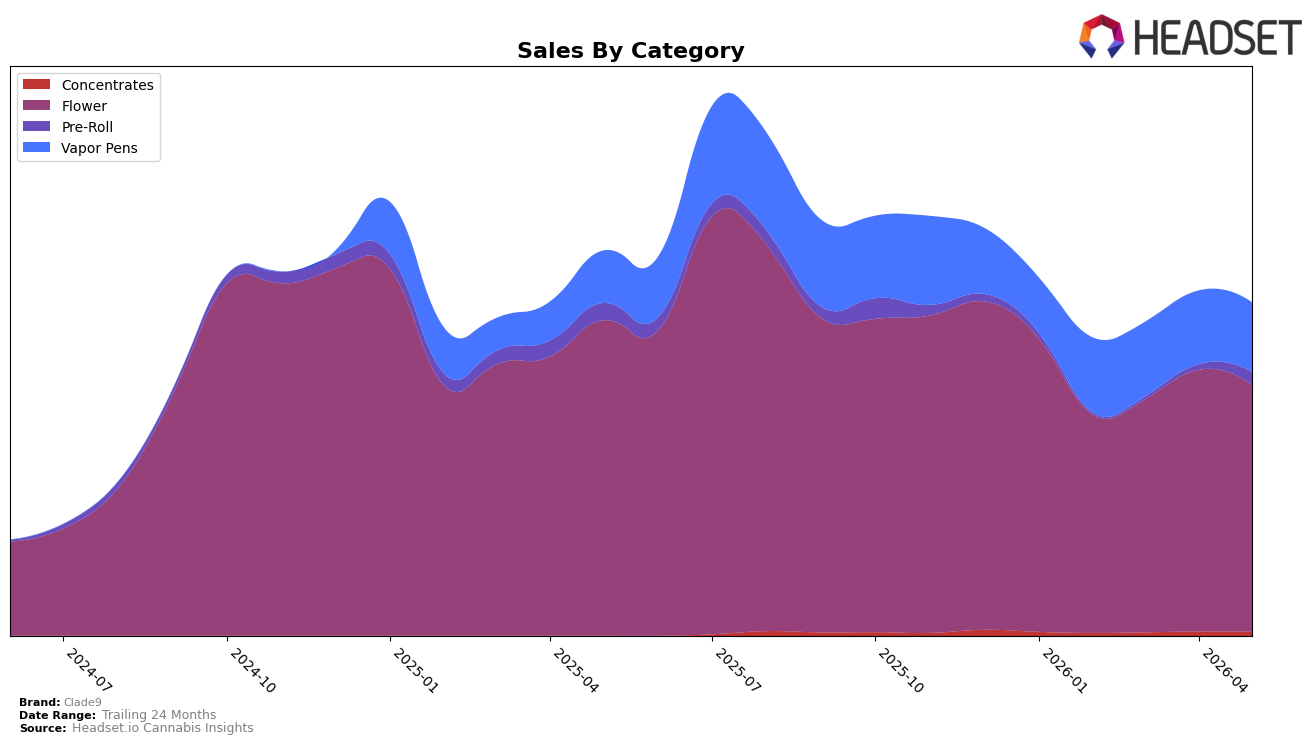

Clade9’s category mix in May 2026 skewed heavily to Flower at 74.09% share, but Flower fell 21.88% year over year and 5.75% month over month, pulling overall sales down 13.49% YoY while the brand’s average price contracted 11.04%. Vapor Pens climbed 32.98% YoY to 20.88% share despite a 5.41% MoM dip, indicating consumer pull even as near-term velocity softened; meanwhile, Pre-Roll held just 3.87% share but spiked 140.59% MoM after a 23.57% YoY decline, suggesting a tactical rebound from a low base. Concentrates remained small at 1.17% share with a 9.36% MoM decline and no YoY read, and the average ticket in May 2026 was $42.81 as Flower’s $44.75 and Vapor Pens’ $42.50 mixed down with Pre-Roll’s $24.26. In New Jersey Flower, Clade9 ranked 7, so the dependence on a shrinking primary category and a modest month-over-month drag in two of the top three segments implies near-term rank risk unless the mix shifts toward categories with positive year-over-year momentum.

The pattern implies Clade9 is overexposed to a contracting core and underweight in the one category showing durable YoY expansion: Vapor Pens at +32.98% YoY versus Flower at -21.88% YoY, while Pre-Roll’s 140.59% MoM surge offers a lever to diversify away from the 74.09% Flower concentration. With overall prices down 11.04% YoY and both Flower and Vapor Pens slipping 5.75% and 5.41% MoM respectively, the brand’s May 2026 price architecture likely chases volume in lower-priced formats, positioning Clade9 to stabilize share by leaning into Pre-Roll as an acquisition entry and scaling Vapor Pens where the YoY trajectory is favorable, which could reduce reliance on a rank-7 Flower foothold in New Jersey.

Competitive Landscape

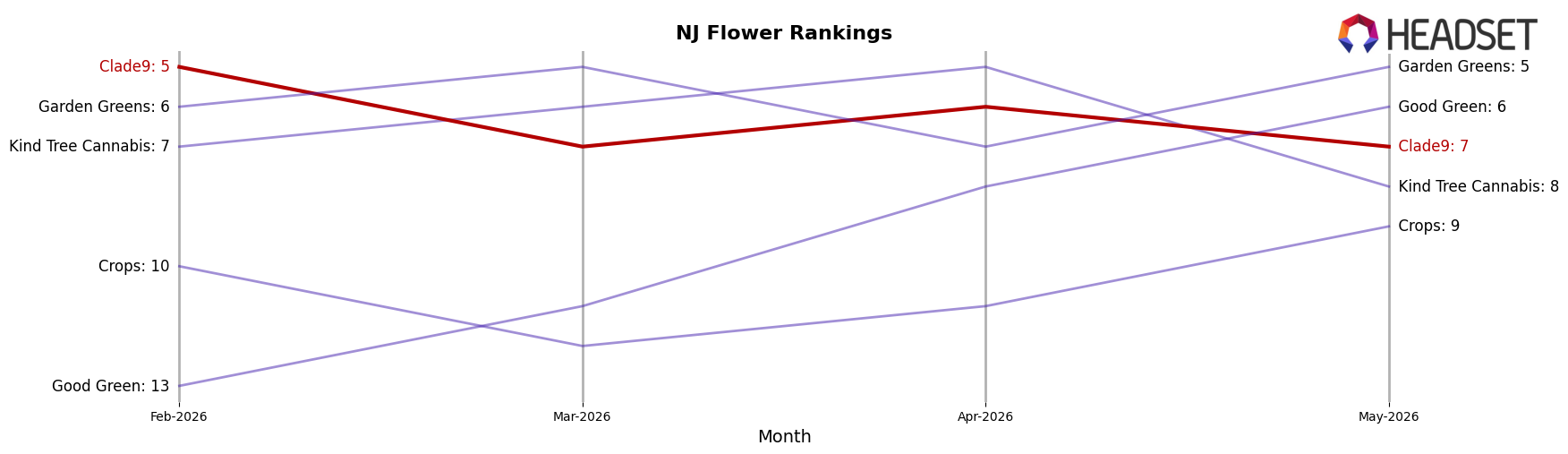

Clade9 is currently ranked #7 in New Jersey Flower in May 2026, down 3 positions from #4 year over year, and 2 positions lower than its #5 spot in February 2026; this follows a prior peak at #3 in November 2025, indicating a multi-quarter slide. By contrast, Find. climbed from #15 to #1 with 189.3% year-over-year sales growth, while Ozone slipped from #1 to #2 alongside a 25.9% sales decline, and Garden Greens sits at #5 after a 2-position rise despite a 44.9% sales drop; these mixed competitor trajectories suggest rank is being reshuffled by distribution and assortment changes more than uniform demand trends. The pattern implies Clade9’s downward rank trajectory from #3 in November 2025 to #7 in May 2026 points to relative share loss amid a volatile leaderboard where aggressive movers can overtake even as some incumbents contract.

Notable Products

Clade9’s steepest movement in May 2026 was the Orange Push Pop Distillate Disposable (1g) falling 23.3% month over month to rank 7, while the leading Orange Push Pop (3.5g) rose 13.3% and held rank 1. Orange Push Pop (1g) advanced 24.5% to rank 2, and Fig Bar (3.5g) added 13.5% while Diamond Bar (3.5g) in rank 3 inched up 2.2%, indicating gains are concentrated at the top even as a key Vapor Pens SKU retreated. With eight of the top ten in Flower and only two in Vapor Pens, the mix signals a tilt toward Flower-led traffic and basket builders, with disposables serving a secondary role rather than a growth engine.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.