Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

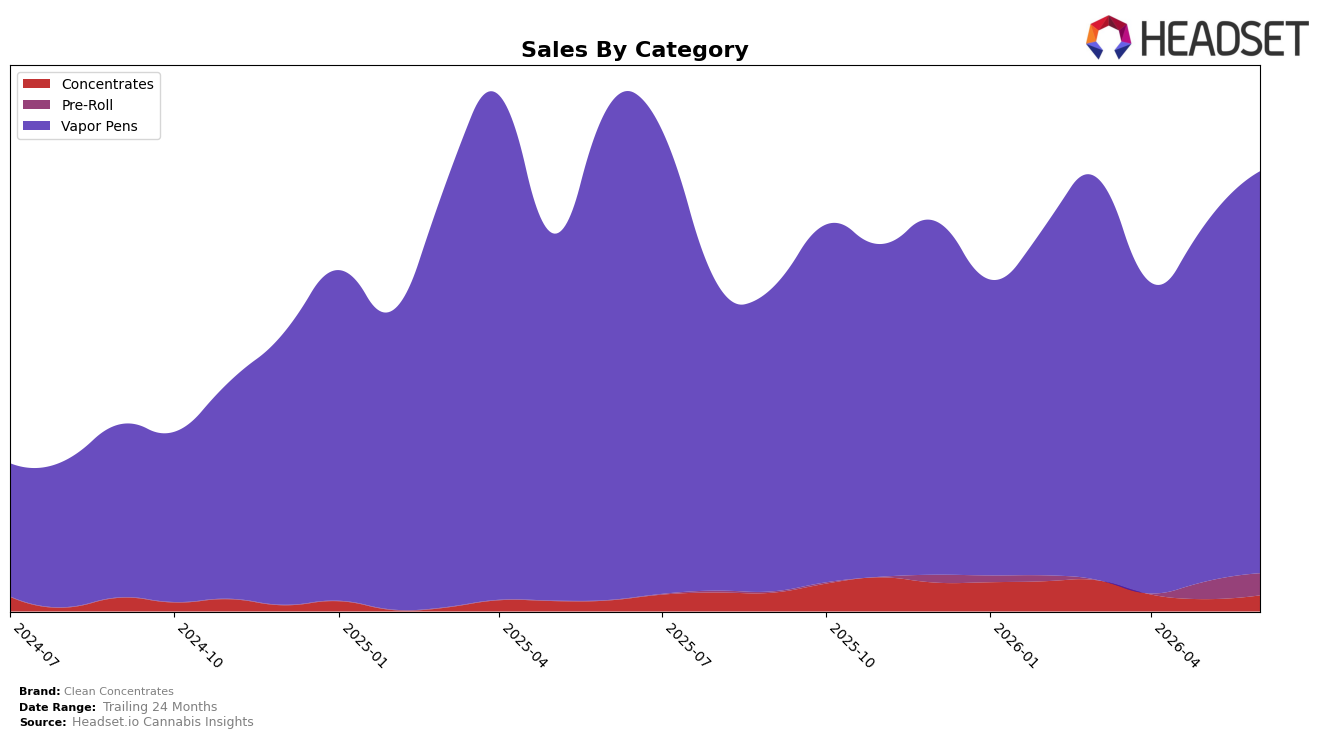

In June 2026, Vapor Pens held 91.50% of Clean Concentrates’ mix and sat at rank 15 in Arizona Vapor Pens, with category sales down 18.50% year over year but up 12.67% month over month; by contrast, Concentrates represented 3.57% share with a 48.68% year-over-year increase and a 31.92% month-over-month lift. Pre-Roll accounted for 4.93% share, posting a 27.96% month-over-month rise while lacking a reported year-over-year comp, and average price rose 3.43% year over year to $16.37. This mix—dominated by a declining year-over-year Vapor Pens core while smaller lines accelerate month over month—implies the category anchor is stabilizing sequentially as growth optionality concentrates in niche formats.

The divergence between a double-digit year-over-year decline in Vapor Pens and double-digit month-over-month gains in both Pre-Roll and Concentrates indicates portfolio risk if rank 15 in Arizona Vapor Pens slips while emerging categories outpace their small bases. With Concentrates’ 48.68% year-over-year and 31.92% month-over-month growth alongside Pre-Roll’s 27.96% month-over-month increase, the brand’s path to insulating against a 12.80% year-over-year sales decline rests on reallocating toward the 8.18–12.83 average-price tiers where velocity is expanding, implying a positioning shift from Vapor Pen-heavy to a more balanced, value-accessible mix that preserves volume while defending Vapor Pens share.

Competitive Landscape

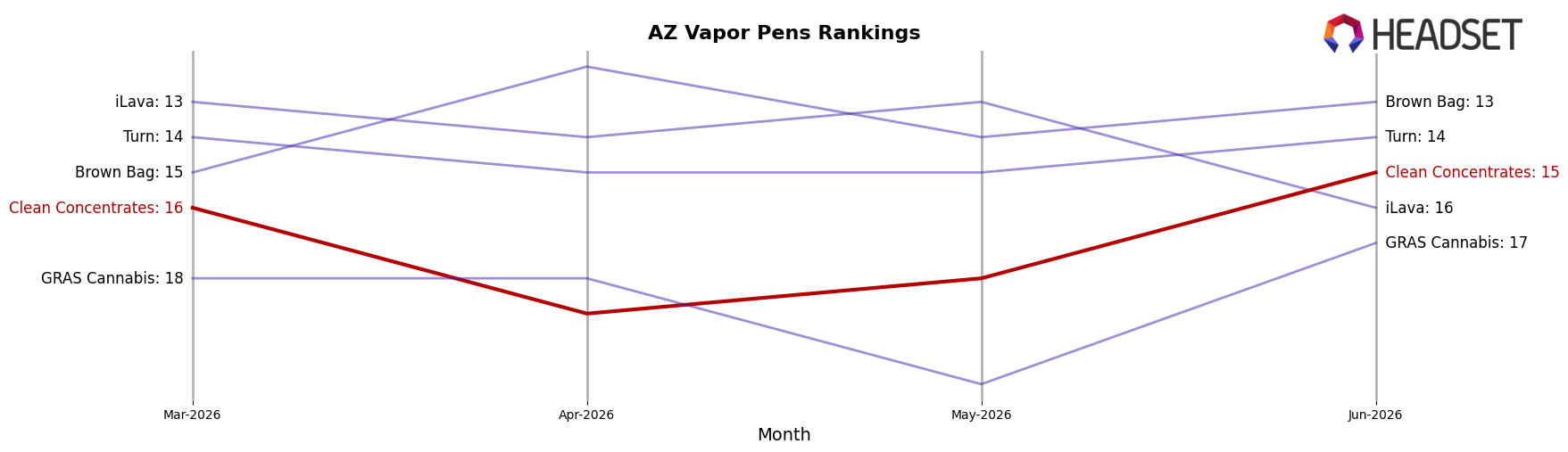

Clean Concentrates sits at rank #15 in June 2026 in AZ Vapor Pens, down 3 positions year over year from #12, and up 1 spot versus March 2026 when it was #16; the brand’s peak was #12 in July 2025, placing today’s #15 three ranks off that high. Against this backdrop, Abstrakt climbed from #5 to #2 with a 162.2% year-over-year sales change while Mfused held #1 despite a -19.4% sales change, indicating that Clean Concentrates’ relative slippage of 3 ranks year over year and only a 1-rank quarter-over-quarter gain leave it ceding ground to faster risers and even to incumbents absorbing declines; the pattern implies a mid-tier brand at risk of being boxed out of the top 12 unless it converts share from declining leaders or matches the triple-digit growth seen by surging peers.

Notable Products

Strawberry Cough Distillate Compact Disposable (2g) posted the largest month-over-month gain at +45.9% while holding rank 3, and Melt Mode Infused Pre-Roll (1g) followed with +44.2% at rank 1, indicating momentum concentrated at the top rather than breadth across the lineup. Cherry Bomb Distillate Compact Disposable (1g) advanced +42.0% to rank 2, whereas Peach Distillate Cartridge (1g) slipped -4.6% at rank 9, and four of the top ten are Vapor Pens SKUs clustered between ranks 2 and 7, signaling category-led lift more than price-driven expansion despite one SKU exceeding $29,000 in June 2026 sales. The absence of any declines worse than -10% alongside multiple 40%+ movers implies Clean Concentrates is leaning into higher-velocity disposables and preserving share through concentrated bets in Vapor Pens rather than broad-based SKU proliferation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.