Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

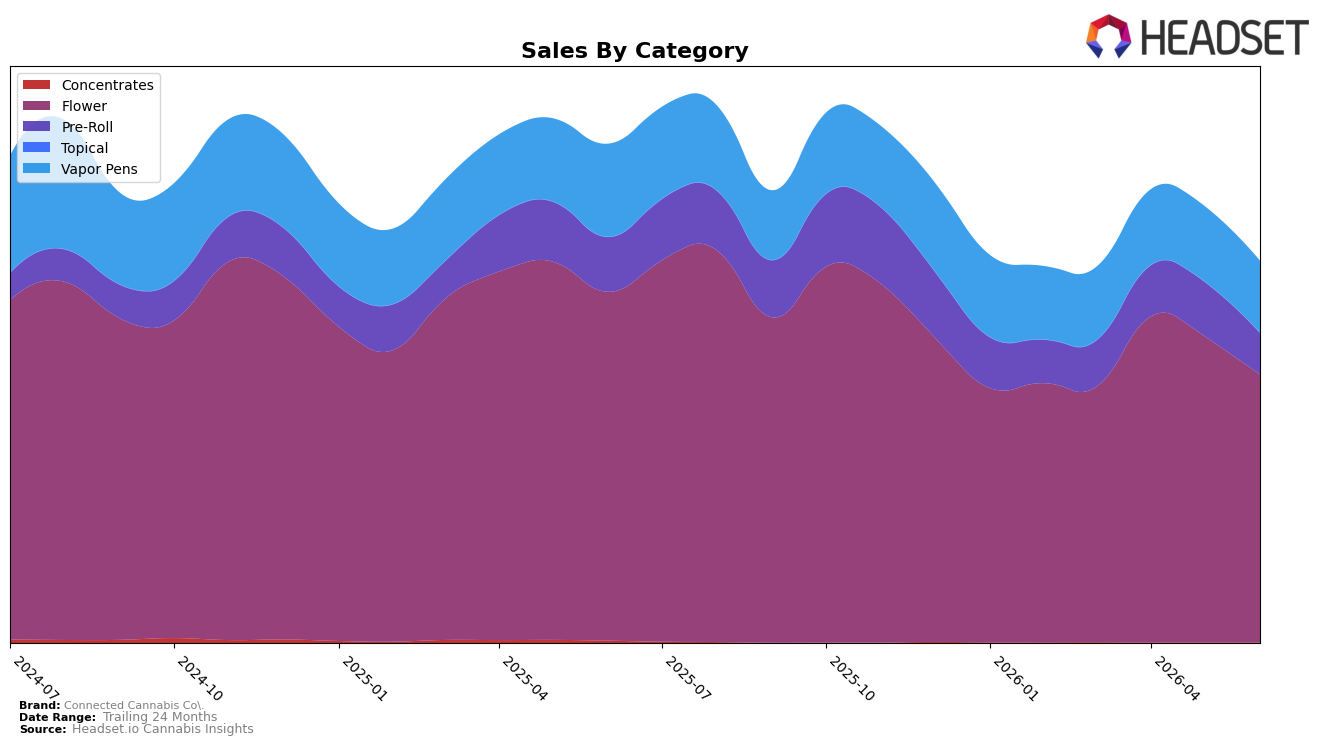

Connected Cannabis Co.’s category mix in June 2026 is anchored in Flower at 70.33% share with year-over-year sales down 23.19% and month-over-month down 12.47%, while Vapor Pens hold 18.82% share with year-over-year down 22.71% and month-over-month down 4.70%. Pre-Roll accounts for 10.76% share but contracted faster with year-over-year down 24.65% and month-over-month down 23.97%, and Concentrates sit at 0.09% share with year-over-year down 83.76% and month-over-month down 19.69%. With average price essentially flat year-over-year at +0.28% while the brand’s total year-over-year sales fell 23.52%, the pattern implies volume attrition concentrated in core Flower and accelerated pullback in Pre-Roll, tightening the portfolio around higher-priced Flower even as overall unit throughput declines.

The consolidation toward Flower at 70.33% share alongside a 12.47% month-over-month drop, combined with a 23.97% month-over-month slide in Pre-Roll and a 4.70% month-over-month decline in Vapor Pens, implies overexposure to demand softening in inhalable formats and less diversification to buffer shocks. Given the brand’s top market is CA and its rank position of 13 in Flower in Arizona, the mix suggests Connected Cannabis Co. is positioned as a Flower-centric player prioritizing price integrity over promotional volume, which, coupled with a 23.52% brand-level year-over-year decline and a 21.16% two-year decline, implies the need to rebalance toward formats with steadier month-over-month trajectories to protect share without further compressing average price.

Competitive Landscape

Connected Cannabis Co. sits at rank #23 in CA Flower in June 2026 after sliding 7 positions from #16 year over year, and falling 6 spots from #17 in March 2026, while remaining 12 places below its peak at #11 from August 2025; meanwhile, STIIIZY rose from #2 to #1 with a 62.5% YoY sales increase and CAM climbed from #3 to #2 with a 56.2% YoY lift, outpacing the brand’s trajectory as CannaBiotix (CBX) edged down from #1 to #3 despite 2.4% YoY growth; this combination of a 7-rank YoY decline and a 6-rank drop over the last three months points to sustained share erosion versus ascending leaders, implying that without a near-term rank inflection the brand is trending toward the second quartile rather than reapproaching its August 2025 peak.

Notable Products

Silver Spoon (3.5g) posted the steepest decline in June 2026 at -13.8% month over month, slipping to rank 4 while Jack of Diamonds (3.5g) fell -12.3% to rank 3. Gascotti (3.5g) held rank 1 despite a -1.0% dip, and Permanent Marker (3.5g) stayed at rank 2 with a -4.8% slide, signaling that leadership is intact even as velocity cools at the tier just below. Five of the top ten are Flower SKUs clustered at ranks 1–5, whereas Pre-Rolls at ranks 6, 9, and 10 saw sharper drops, including Ghost OG Pre-Roll (1g) at -18.5%, pointing to category mix pressure. The pattern implies Connected Cannabis Co. is leaning on flagship Flower to anchor share while reevaluating Pre-Roll assortment and pricing to stabilize secondary tiers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.