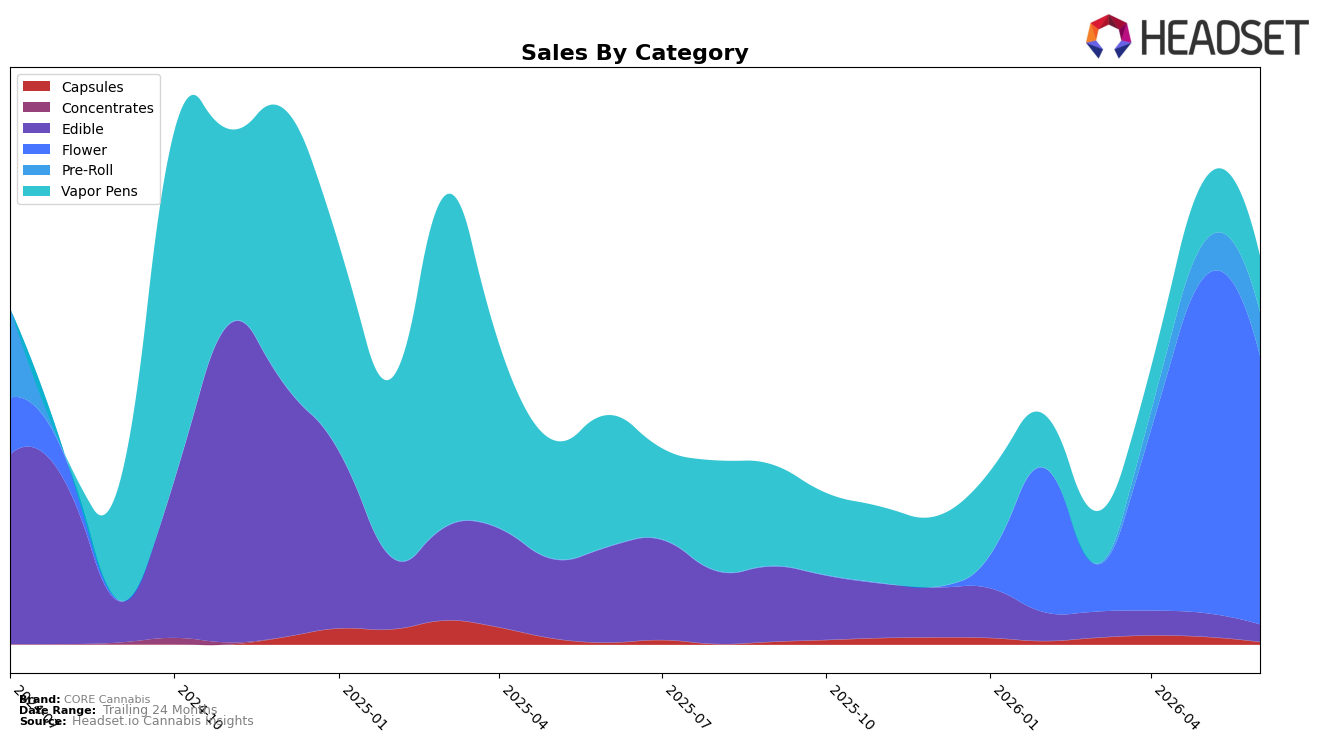

Market Insights Snapshot

In June 2026, CORE Cannabis concentrated 69.30% of sales in Flower, where month-over-month sales fell 20.16% and the brand sat at rank 39 in Nevada Flower, while the brand’s overall sales were up 69.94% year over year. Vapor Pens dropped 57.35% year over year and 9.72% month over month to 14.43% share, whereas Pre-Roll expanded 24.64% month over month to 11.25% share despite lacking a year-over-year benchmark. Edible contracted 82.04% year over year and 26.60% month over month to 4.41% share, and Capsules, though up 39.82% year over year, fell 68.91% month over month to 0.60% share. With the average price up 5.10% year over year to $22.12 alongside Flower’s month pullback and Pre-Roll’s month surge, the mix implies a pivot toward lower-priced, faster-turn formats to stabilize volume while Flower remains the anchor at a mid-pack rank.

The shift toward Pre-Roll month-over-month growth of 24.64% alongside a 20.16% Flower decline suggests CORE Cannabis is using Pre-Roll to buffer volatility in its 69.30% Flower-heavy mix, a positioning that can trade down consumers without abandoning inhalables. The 57.35% year-over-year contraction in Vapor Pens and the 82.04% year-over-year decline in Edible indicate a retreat from non-Flower inhalation-adjacent and ingestible segments, while Capsules’ 39.82% year-over-year rise but 68.91% month drop points to episodic, not strategic, participation. Given the rank of 39 in Nevada Flower and a 5.10% year-over-year price increase, the pattern implies a price-disciplined, Flower-led stance that relies on Pre-Roll as the growth lever and de-emphasizes Vapor Pens and Edible for margin and inventory control.

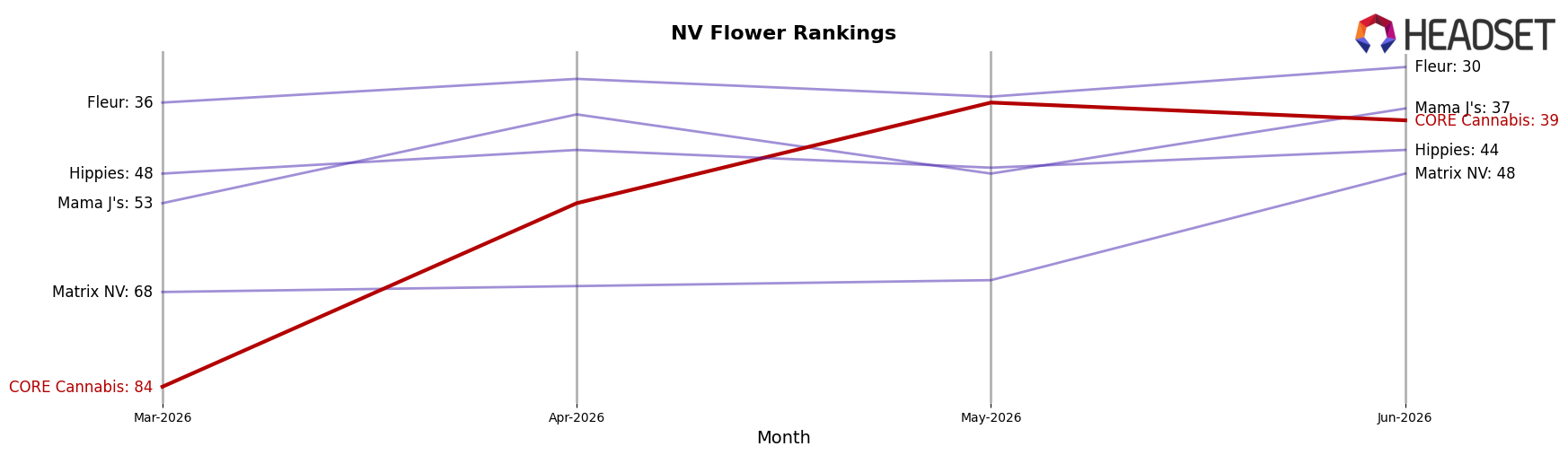

Competitive Landscape

CORE Cannabis is ranked #39 in NV Flower in June 2026, improving 45 positions from #84 in March 2026 and sitting 3 spots below its peak of #36 in May 2026; without a year-over-year rank, the quarter-to-date climb of 54% in rank position (from #84 to #39) contrasts with RYTHM holding #2 while posting a -6.9% sales YoY change and FloraVega / Welleaf at #3 after a 22-place YoY rank rise with 260.4% sales growth. Against the leader STIIIZY at #1 with a 5.2% YoY sales increase, CORE Cannabis’s 3-month rank surge and slight pullback from May 2026 imply a momentum-driven rebound that is sensitive to execution but now within striking distance of consistent top-30 presence.

Notable Products

Lemon Bars Pre-Roll (1g) posted the standout movement with a 101% month-over-month surge to rank 1, while Blue Diesel (3.5g) climbed with a 69% MoM gain to rank 3. Banana Punch (3.5g) also accelerated 76% MoM at rank 5, and four of the top ten are Flower SKUs concentrated between ranks 2 and 8. The absence of any steep declines under -10% alongside these triple- and high-double-digit gains implies the portfolio is pivoting toward velocity-led SKUs where Pre-Roll lift is complementing a Flower-heavy core.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.