Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Clear is stocked at 391 licensed dispensaries across Colorado, Montana, and 6 other states, 135 of them in Colorado, with the deepest coverage in Colorado Springs, Denver, Aurora, Boulder, and Pueblo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

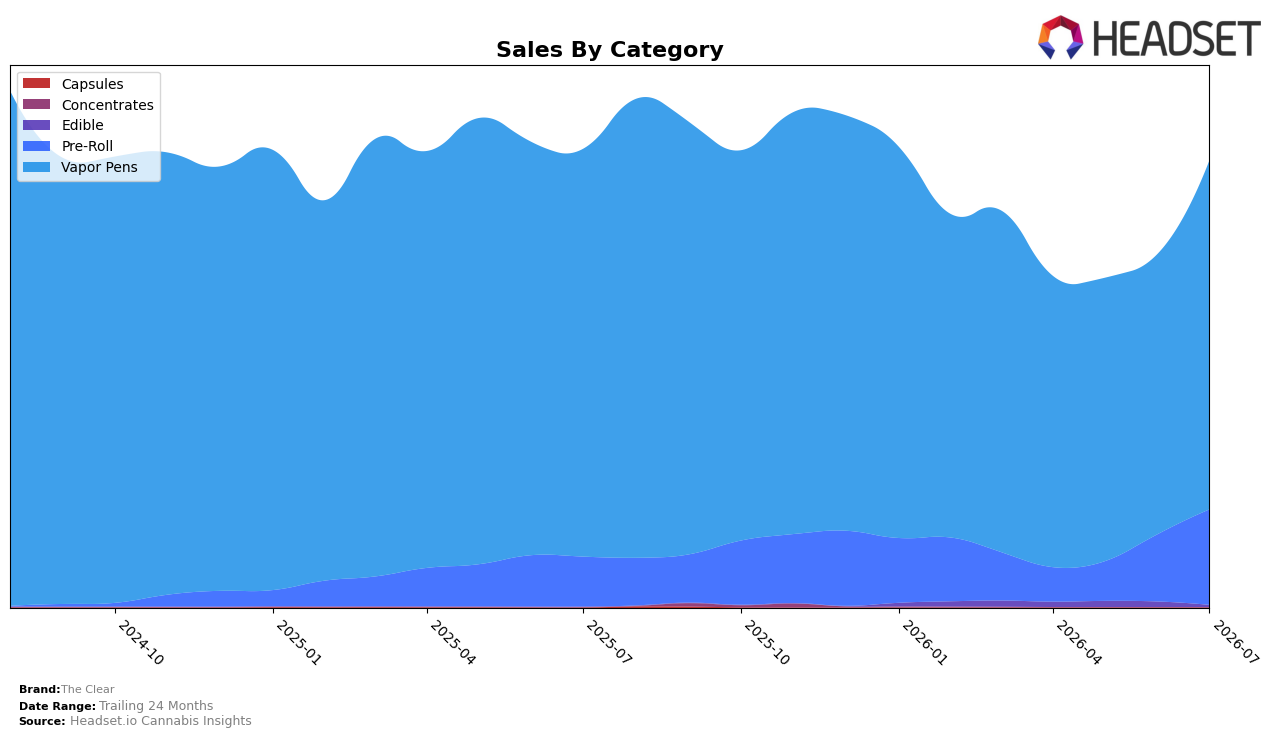

In July 2026, The Clear remained concentrated in Vapor Pens at 78.29% share, with category sales up 24.44% month over month but down 14.43% year over year, while Pre-Roll expanded to 21.34% share on 41.77% MoM and 92.27% YoY growth. Edible contracted to 0.37% share with a 67.32% MoM decline and no year-over-year baseline, and the brand’s average price fell 21.63% YoY to $29.39. Despite brand sales declining 2.53% YoY, the mix shift toward Pre-Roll alongside a MoM rebound in Vapor Pens indicates a rebalancing that offsets category softness in Vapor Pens and cushions overall volatility.

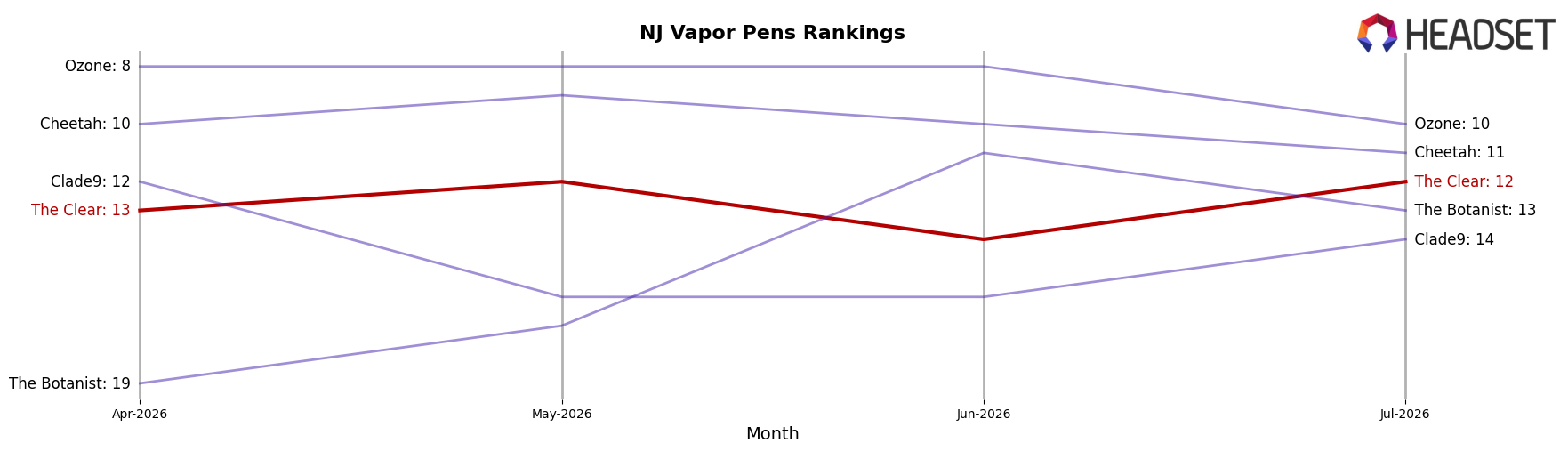

The Clear’s position in New Jersey Vapor Pens at rank 12, combined with a 24.44% MoM lift in that category and a 92.27% YoY surge in Pre-Roll, implies the brand is trading some depth in its core for breadth across formats. The 21.63% YoY price decline alongside Vapor Pens’ 14.43% YoY sales dip suggests a value-led pivot that can sustain rank in Vapor Pens while the 21.34% Pre-Roll share serves as a growth wedge; this pattern points to a two-pronged positioning where Vapor Pens provides scale and Pre-Roll supplies incremental share capture.

Competitive Landscape

The Clear sits at rank 12 in July 2026, down 2 positions year over year from rank 10, and has eased 1 spot since April 2026 when it was rank 13, despite having peaked at rank 9 in January 2026; meanwhile, Select held rank 1 with a -8.9% year-over-year sales change while RYTHM advanced to rank 5 from rank 8 on 43.9% year-over-year growth, indicating that The Clear’s downward rank drift amid competitors’ stability at ranks 1–4 and upward mobility into rank 5 points to share being redistributed toward faster-growing incumbents rather than broad market contraction.

Notable Products

Strawberry Banana Twax Infused Pre-Roll (1g) delivered the standout move in July 2026 with a +60.4% month-over-month surge while holding rank 3, outpacing Elite - Grapevine Distillate Cartridge (2g) at rank 7 with +36.9% and Twax - Lime Sorbet Distillate Infused Pre-Roll (1g) at rank 1 with +22.2%. Three Twax-infused Pre-Rolls sit inside the top 4 with gains of +60.4%, +25.6%, and +22.2%, whereas top Vapor Pens at ranks 5–7 posted a mixed range from +8.6% to +36.9%. This skew toward high-growth Pre-Rolls at premium ranks implies the product mix is tilting toward infused format velocity rather than relying solely on 2g Vapor Pens for topline momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.