Oct-2025

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

CRU Cannabis has shown varied performance across different categories in New York. In the Pre-Roll category, the brand has consistently remained outside the top 30 rankings, slipping from 36th position in July 2025 to 49th by October 2025. This downward trend in rankings is accompanied by a notable decline in sales from July to September, although there was a slight recovery in October. The absence of CRU Cannabis from the top 30 brands in this category over the months could be a point of concern, indicating potential challenges in market competitiveness or consumer preference shifts.

In contrast, the Vapor Pens category presents a more positive trajectory for CRU Cannabis in New York. The brand maintained a presence within the top 30, albeit with some fluctuations. After a dip in rankings from July to September, CRU Cannabis improved its position to 29th in October 2025, suggesting a potential recovery or strategic adjustments that resonated with consumers. Sales figures reflect this trend, with a rebound in October following a decrease in previous months. This indicates that while the brand faces challenges in some areas, there are opportunities and growth potential in others, particularly in the Vapor Pens category.

Competitive Landscape

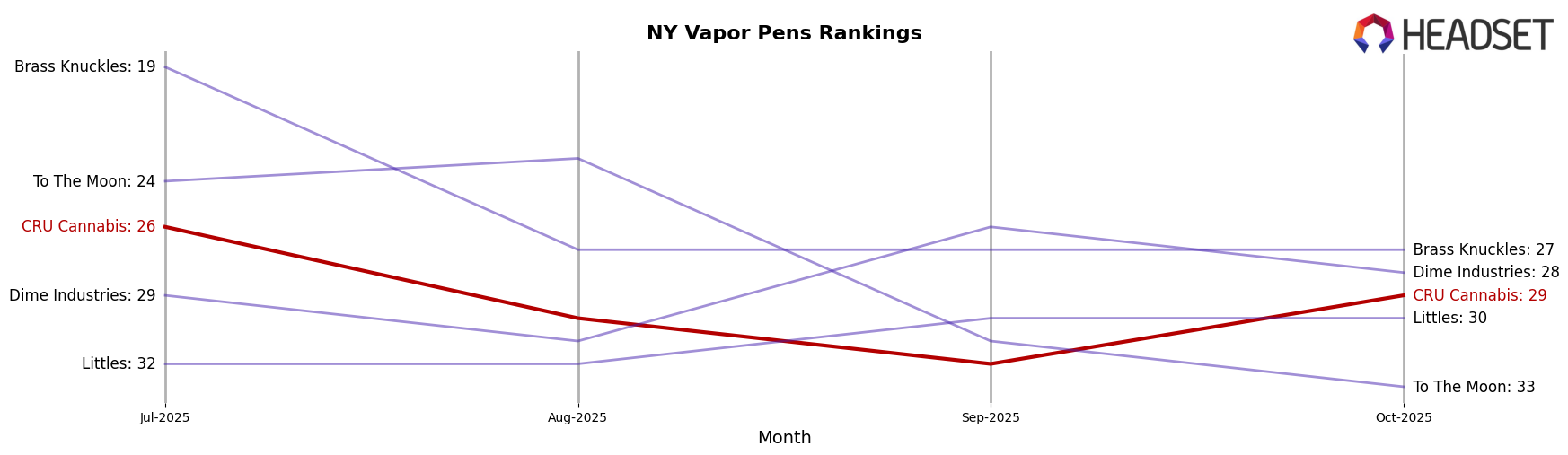

In the competitive landscape of vapor pens in New York, CRU Cannabis has experienced fluctuating rankings over the past few months, indicating a dynamic market presence. As of October 2025, CRU Cannabis ranked 29th, showing a slight improvement from September's 32nd position, yet remaining outside the top 20. This is contrasted by brands like Brass Knuckles, which maintained a consistent lead despite dropping out of the top 20 after July. Meanwhile, Dime Industries showed a positive trajectory, improving their rank from 31st in August to 28th in October, suggesting a growing market share. Littles and To The Moon also present interesting cases; Littles remained stable in the lower ranks, while To The Moon experienced a notable drop from 23rd in August to 33rd in October. These shifts highlight the competitive pressures CRU Cannabis faces, emphasizing the need for strategic marketing and product differentiation to enhance its market position and drive sales growth.

Notable Products

In October 2025, CRU Cannabis's top-performing product was the Granddaddy Purple Live Resin Liquid Diamonds Sauce Disposable (1g) in the Vapor Pens category, maintaining its number 1 rank from September with sales of 1277 units. The Cheetah Piss Pre-Roll (0.5g) rose to the 2nd position in the Pre-Roll category, showing a significant climb from 4th place in September. Tropicanna Cookies Infused Pre-Roll (0.5g) also improved its standing, moving up to 3rd place from 5th in the same category. Maui Wowie Live Sauce Disposable (1g) in Vapor Pens saw a drop, falling to 4th position from 2nd in September. Lastly, the Durban Poison Sauce Disposable (1g) in Vapor Pens slipped to 5th place, down from 3rd in the previous month.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.